Inman News

Soaring home prices have fueled talk of a bubble. Economists, however, think a gradual slowdown is more likely than a sudden pop.

BY JIM DALRYMPLE II

Bill Wilmering’s buyer has disappeared.

An agent with Wood Brothers Realty in the St. Louis area, Wilmering recently told Inman that he had been working with a man who found the perfect home. Together, they put together an offer that they thought could work. And then as has happened to so many agents this spring, they lost a bidding war.

“I haven’t heard from him in days, which is very unusual for him,” Wilmering said. “The last comments I had from him were that he was very discouraged.”

The anecdote is just one of many that highlights the brutal market buyers face in much of the U.S. right now. It’s a market that has been shaped by supply shortages, rising material costs and the coronavirus pandemic — all of which have sent prices soaring.

Now, with no end in sight to the price increases, many are beginning to wonder: Is this a bubble? And if so, when does it pop?

To get a sense of what lies ahead for the housing marketing, Inman spoke to economists and agents around the country. In every case, they said that what’s going on now is unprecedented.

But the takeaway from these conversations was also that while there are some warning signs, and nothing goes up forever, the housing market does not appear to be heading for a sudden collapse any time soon. Instead, a more likely scenario is that it gradually slows down in the coming months and years.

Signs of trouble

Anyone with even a glancing familiarity with the housing market right now knows that prices have been soaring. Asked about those conditions, the economists who spoke to Inman said there are indeed some points of concern.

For example, Taylor Marr, a lead economist and data scientist for Redfin, said today’s price growth is “unprecedented” and suggests there is a “risk of overheating” in the market.

Rick Palacios Jr., director of research for John Burns Real Estate Consulting, made a similar point, describing today’s market as “the early innings” of what could “be a housing bubble.”

“Our view is we are entering the higher risk, higher reward phase of the housing cycle,” he said.

The point that Palacios and Marr were making is not that a bubble is here now, but rather that today’s rapid price appreciation could theoretically lay the groundwork for some bubble-like conditions in the future. For example, if speculators entered the market en masse and banked on the theory that home prices would keep rising the way they are today, there could be a problem.

The good news

Still, no one who spoke with Inman said the market has reached a bubble stage yet.

Palacios, for example, noted that during the last bubble, lenders loosened who they’d give money to. There were also a variety of “exotic” mortgage products on the market, such as loans with payments that would jump up after the first few years. Those loans banked on their users either refinancing or experiencing wage growth, but when the economic collapsed many homeowners found they couldn’t afford their ballooning payments.

Today, however, lending is far more conservative than it used to be, and homeowners tend to have much more equity in their houses.

“Right now the majority of lenders are not doing wacky lending,” Palacios said.

He also pointed out that current price appreciation is driven by a supply shortage, combined with a demographic wave of potential new homebuyers.

Obviously a supply shortage isn’t good news for consumers on the ground who are facing relentless bidding wars and endless discouragement. But it is good in the sense that it differs from the last housing bubble in 2008, when supply ultimately outstripped demand and put many homeowners underwater. In other words, today’s supply issues, while frustrating, suggest that what’s going on right now is not a bubble.

Marr agreed that supply shortages are a major cause of what’s going on right now, and distinguish this moment from the past. He also said low mortgage rates and rising demand from workers who don’t have to go to the office are factors. And while all of these things create challenges for consumers, they don’t necessarily mean broader economic catastrophe waits on the horizon.

“A bubble really implies overvaluation driven by speculation,” Marr said. “Eventually that’s a house of cards that’s going to pop. You bet and over bet in the hope that prices will keep rising. But are people overpaying on housing? I would say so far the answer at least on a national level is no.”

George Ratiu, a senior economists at realtor.com, on the other hand told Inman he has seen instances of overpricing.

Still, he doesn’t see the massive speculation today that characterized the last housing crash, and agreed with Palacios that lending is more conservative. The result is that Ratiu’s ultimate take is similar to the other experts who spoke with Inman, and he believes the market is “more stable” right now than it was in, say, 2008.

“I don’t yet see a bubble,” he ultimately concluded.

When is relief coming?

So where does all of this leave consumers and their agents? While it’s certainly good news that economists don’t see an economic collapse coming, rising prices are a serious strain for many would-be homeowners. And many are wondering when they’ll get some relief.

There are basically two timelines here: The short term and the longer term.

In the short term, conditions could start to cool somewhat within months.

“My outlook has been that price growth will start to slow down in the second half of this year,” Marr said.

Marr thinks price growth will slow for a number of reasons. For example, during the pandemic many Americans had nothing to spend discretionary income on. Restaurants and movie theaters were closed, travel was mostly impossible, and recreational spending evaporated. The result was that, at least for those who kept their jobs, there was more time and money to devote to home searches.

Saturday Night Live‘s parody of a Zillow ad in February captured what was going on, with the show portraying home searches themselves as a source of recreation.

>>> SNL / Zillow

As the economy reopens in the coming months, however, consumers may have less bandwidth — not to mention cash — to pour into real estate.

Marr specifically envisions people diverting some of their resources back into lifestyle oriented activities, and that should reduce demand for homes in the near future. (Some agents are already seeing this phenomenon play out in their local markets.)

At the same time, supply should increase as early as this year as well.

Ratiu, for example, pointed to a recent survey his company conducted which found that 10 percent of homeowners plan to put their houses up for sale sometime during 2021. In large part current appreciation has been driven by not enough homeowners responding to market conditions by listing their properties, so an influx of supply would temper prices the short term.

“That to me is tremendous good news,” Ratiu added.

Also in the shorter term, builders should finally succeed in adding more supply as well.

“They’ve been buying land hand over fist of the last three quarters,” Palacios said of builders. “So that’s going to start happen at the end of this year, where you’re finally going to have some new supply.”

The takeaway is that over the next six months, the intensity of competition in the market should begin to subside somewhat.

Still, that doesn’t mean buyers will suddenly get deals.

Looking at the longer term — so, the next few years — Palacios compared current conditions to a train, saying that it isn’t going to “fall off the tracks but the train is going to slow down a little bit.” And he ultimately predicted that price appreciation, even if it slows, will continue for “several years.”

Everyone who spoke with Inman agreed, saying prices aren’t going to keep climbing at their current rates, but they also aren’t going down any time soon.

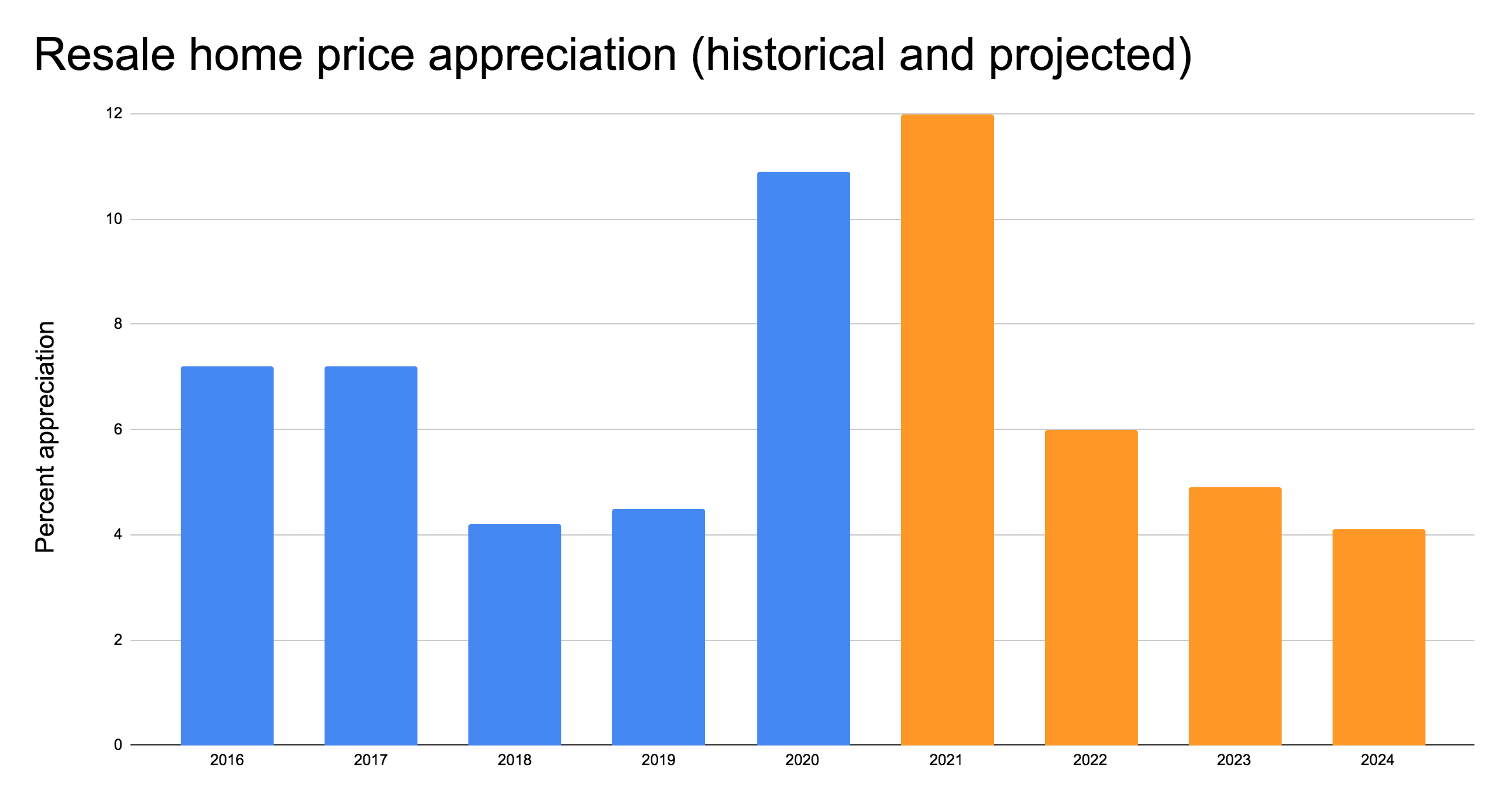

In a report provided to Inman, Palacios’ company John Burns Real Estate Consulting specifically states that current price appreciation is 13.8 percent for existing single family homes. But the report forecasts appreciation falling to 6 percent in 2022, 4.9 percent in 2023 and 4.1 percent in 2024.

Historic appreciation values are represented here in blue, while projections for the future are in orange. This data, from John Burns Real Estate Consulting, suggests that home price appreciation should peak this year, though it shouldn’t dip into negative values any time soon. Credit: Jim Dalrymple II via data from John Burns Real Estate Consulting

That’s a considerable slowdown compared to what’s happening today, but it’s also not a bubble bursting.

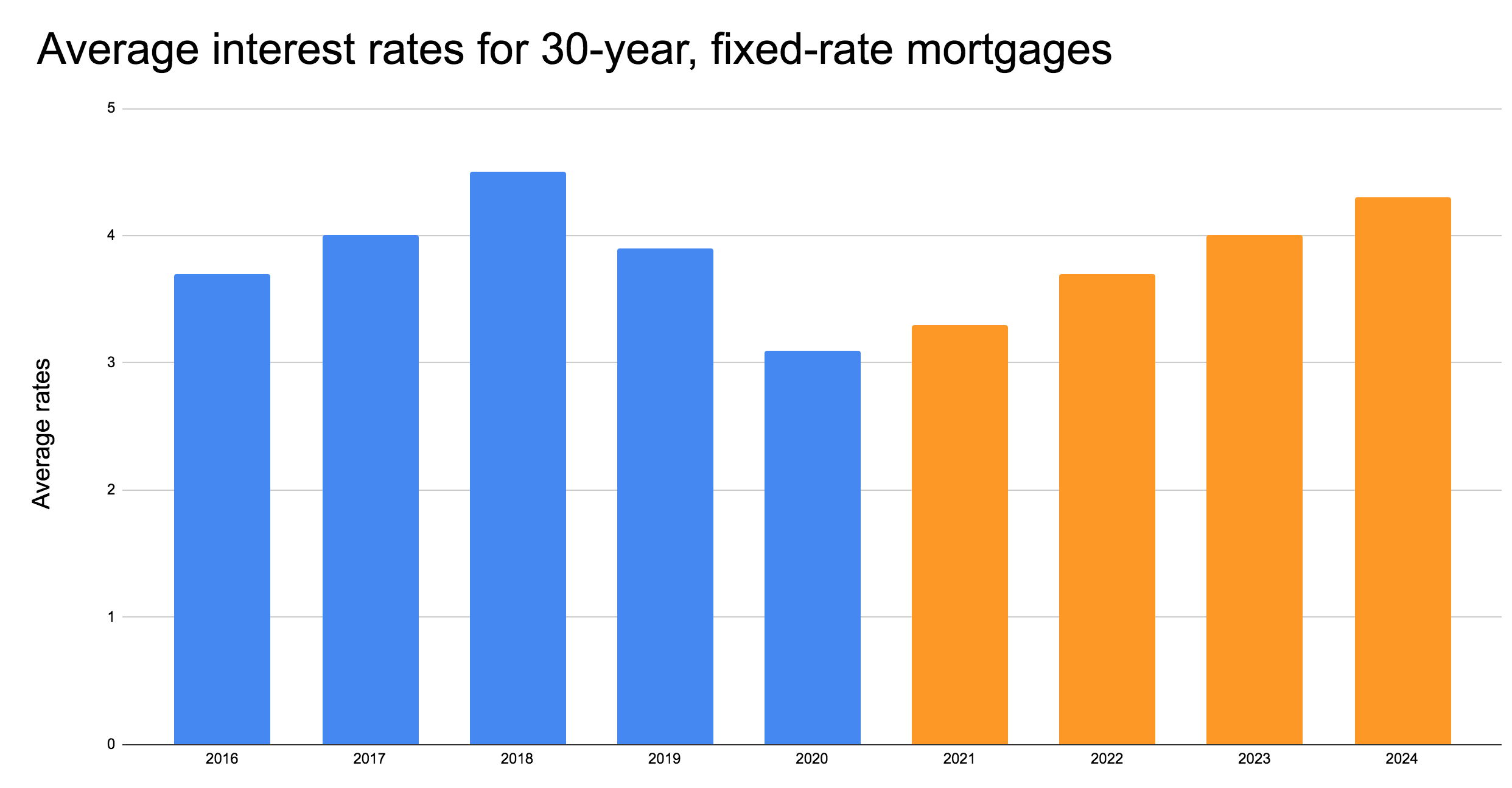

One of the key factors that will shape what happens next is mortgage rates. Most projections right now indicate mortgage rates will rise John Burns Real Estate Consulting, has forecasted an average rate of 3.7 percent for a 30-year fixed rate loan in 2022. That would an increase compared to an average of 3.2 percent right now.

Significantly, the forecast indicates rates could jump to 4 percent in 2023 and 4.3 percent in 2024.

Historic average rates are represented here in blue, while projections for the future are in orange. The data suggests rates should rise in the coming years. Credit: Jim Dalrymple II via data from John Burns Real Estate Consulting

Different analyses have pinpointed different specific numbers, and John Burns Real Estate Consulting comes up with its average projected rates by studying bond markets — a method it sees as more accurate than other approaches.

But the important thing to keep in mind is that there is a consensus that rates should go up in the coming years. That, in turn, should cool conditions off compared to what we’re seeing today.

In the end, then, the likeliest explanation for what’s going on now is that this is an extreme moment, but one that is situated within a generally stable economy. That still means plenty of pain for homebuyers, but it also means the path forward probably won’t be as tumultuous as prior periods of extreme stress in the market.

“The music isn’t going to just stop any time soon,” Palacios concluded, “but the tempo that anybody is dancing to is probably going to slow down.”

Jim Dalrymple II covers real estate technology. Prior to joining Inman he covered politics, the environment, and general chaos for BuzzFeed News.