Inman News

February’s 19.6% annual home price appreciation, together with sharp rise in mortgage rates, produced the tightest affordability in 15 years, according to new data from Black Knight.

Home prices posted the strongest annual gains on record in February, which together with a sharp rise in mortgage rates produced the tightest affordability in 15 years, according to data aggregator Black Knight.

Black Knight’s monthly Mortgage Monitor report shows that after cooling briefly last fall, home price growth reaccelerated in February, with home prices up 19.6 percent from a year ago even as interest rates continued to climb.

Four of the 10 fastest appreciating markets were located in Florida — Tampa, Jacksonville, Orlando and Miami.

Top 10 markets for annual home price appreciation

- Tampa, Florida (33.2 percent)

- Austin, Texas (33.0 percent)

- Raleigh, North Carolina (32.8 percent)

- Phoenix, Arizona, (32.0 percent)

- Nashville, Tennessee (31.5 percent)

- Jacksonville, Florida (29.5 percent)

- Orlando, Florida (28.6 percent)

- Las Vegas, Nevada (28.6 percent)

- Miami, Florida (27.9 percent)

- San Diego, California (27.3 percent)

But the affordability crisis “is particularly acute in western coastal markets,” Black Knight reported.

It now takes more than half the median income to make monthly payments on the average-priced home in Los Angeles (61 percent), San Jose (57.5 percent) San Diego (55.5 percent) and San Francisco (50.9 percent).

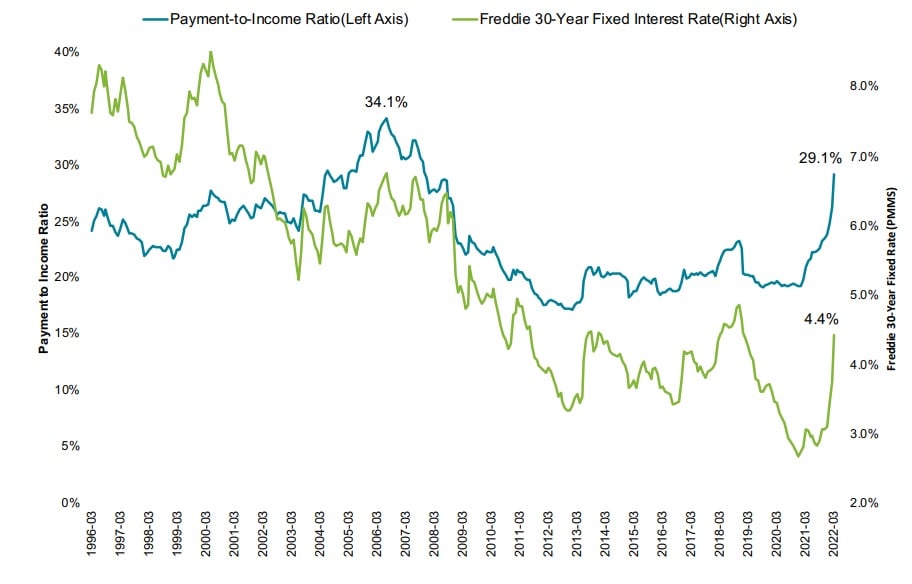

National payment-to-income ratio

Share of median income needed to make the monthly principal and interest payment on the purchase of the average-priced home using a 20 percent down 30-year fixed rate mortgage at the prevailing interest rate. Source: Black Knight Mortgage Monitor.

From 1995 to 2003, U.S. homebuyers needed to devote only 25.1 percent of the median income to make the monthly mortgage payments on the average-priced home. That’s now risen to 29.1 percent for the nation as a whole in March.

Black Knight said 82 of the 100 largest U.S. markets are now less affordable than their long-term benchmarks, up from six at the start of the pandemic.

When payment-to-income ratios rise above 21 percent, that usually helps cool housing market. But record-low inventory “continues to fuel growth even in the face of the tightest affordability in 15 years,” Black Knight reported.

Rising home prices may have fueled “a fear-of-missing-out wave of exuberance” among investors that may point to the need for an eventual price correction, researchers at the Federal Reserve Bank of Dallas warned last week.

Distressed properties haven’t filled inventory gap

Some experts had anticipated that many homeowners who put their mortgage payments on hold during the pandemic might list their homes for sale once forbearance programs expired.

Black Knight estimates that so far, about 925,000 of the 8.1 million homeowners who were in forbearance have put their homes up for sale. Although that generated 40,000 sales a month during the pandemic, those distressed property sales have not filled the inventory gap, and have been trending downward in recent months, Black Knight said.

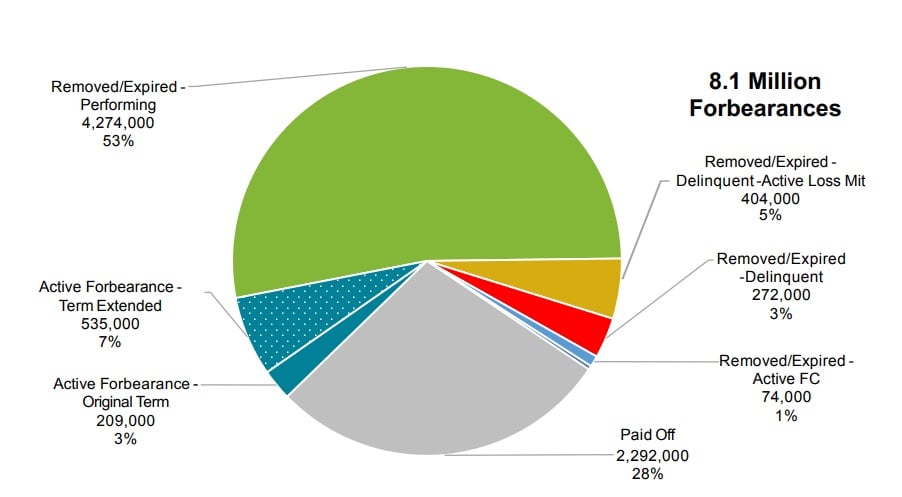

Current status of COVID-related forbearances

Status of loans in forbearance as of March 22, 2022. Source: Black Knight Mortgage Monitor.

About 744,000 loans remained in active forbearance as of March 22, while another 404,000 homeowners whose forbearance programs expired were delinquent on their loans and exploring “loss mitigation” options with lenders such as mortgage modifications to avoid foreclosure.

Some 272,000, most of whom were already delinquent prior to the pandemic, remain past due after exhausting both forbearance and loss mitigation options. Another 74,000 homeowners are in foreclosure, up 6 percent from a month ago, but foreclosure starts fell to 25,000, below pre-pandemic levels.

And while mortgage delinquencies edged up by 1.8 percent in February, the national delinquency rate remained near pre-pandemic levels.