Inman News

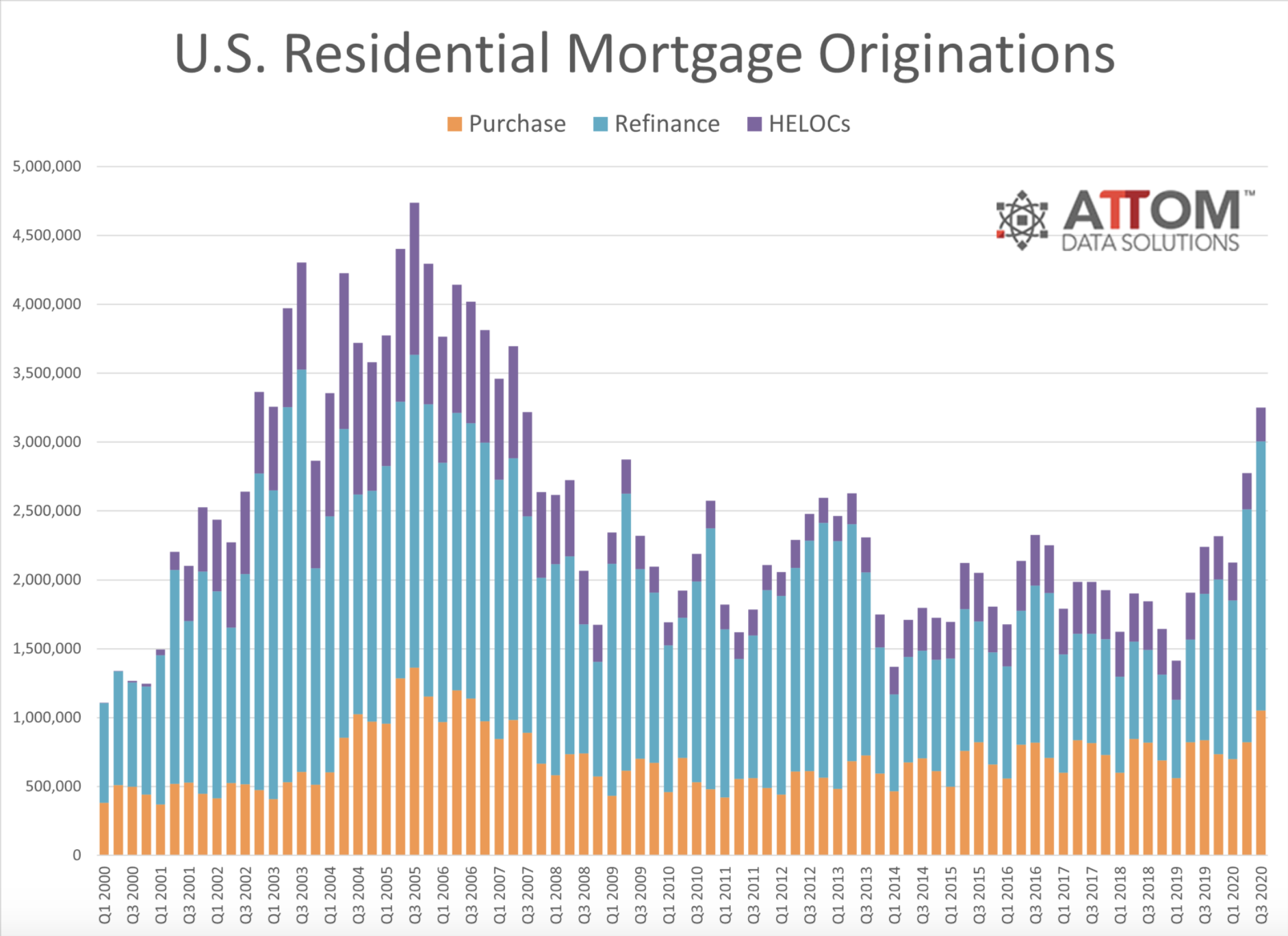

During the third quarter, 3.25 million mortgages were originated on residential properties, the highest level this figure has reached in 13 years.

During the third quarter of 2020, 3.25 million mortgages were originated on residential properties. According to a report from Attom Data Solutions, that figure was up 17 percent from Q2 2020, and up 45 percent from Q3 2019 to its highest level in 13 years.

As interest rates fell below 3 percent on 30-year fixed-rate loans, demand for mortgages spiked nationwide. Mortgage originations represented an estimated $974.1 billion in total dollar volume, a figure up from 20 percent during the second quarter, and up 52 percent from the year before to its highest dollar amount since 2005.

Purchase mortgages jumped during the third quarter, growing at a faster quarterly rate than the number of refinance loans for the first time in over a year. Home-purchase mortgages were up 28 percent from the second quarter and up 25 percent from the third quarter of 2019 to the highest level since the third quarter of 2006. Likewise, the dollar amount of purchase loans rose to $336.3 billion, up 35 percent from the previous quarter and up 36 percent from the year before.

Refinance activity also increased during the third quarter, but at a slower rate than purchase lending. Refinance loans increased 16 percent from the second quarter to the third quarter, while the amount refinanced rose 15 percent to $587.6 billion.

“The home loan industry got even busier in the third quarter of 2020, with the housing market still operating as if the recession brought on by the pandemic didn’t exist,” Todd Teta, chief product officer at Attom Data Solutions, said in Attom’s report. “Buyers and owners, lured by low mortgage rates, kept lining up for loans at levels not seen in more than a decade.”

“The one difference in the third quarter was that purchase lending beat out refinance activity for the first time in more than a year,” Teta added. “However, we do cautiously note again, as we have with other recent market reports, that the pandemic and other factors could come together and halt the market boom. In the meantime, the third quarter stands out as another banner quarter for lenders.”

Across metro areas

Residential purchase mortgage originations increased on a quarterly basis in 204 out of 215 metro areas with a population greater than 200,000 and with at least 1,000 total loans. The largest quarter-over-quarter increases were in Springfield, Illinois (up 233.5 percent); Savannah, Georgia (up 158 percent); Barnstable Town, Massachusetts (up 132.7 percent); Scranton, Pennsylvania (up 85.6 percent); and Bridgeport, Connecticut (up 77.5 percent).

Purchase mortgage lending only decreased in 11 metro areas from Q2 to Q3, with the largest declines in Sioux Falls, South Dakota (down 60.1 percent); Myrtle Beach, South Carolina (down 17.5 percent); Cedar Rapids, Iowa (down 16.6 percent); Ann Arbor, Michigan (down 14.5 percent); and Baltimore, Maryland (down 7 percent).

Refinance activity rose by at least 25 percent in 56 metro areas (about 26 percent of metros analyzed) on a quarterly bases. The largest increases were seen in Laredo, Texas (up 73 percent); Clarksville, Tennessee (up 60.4 percent); Scranton, Pennsylvania (up 58.6 percent); Erie, Pennsylvania (up 50.3 percent); and Visalia, California (up 48.8 percent).

Median down payments and loan amounts reach new highs

The median down payment on single-family homes and condos purchased with financing during the third quarter spiked to $20,775, an increase of 48.9 percent from the previous quarter, and a jump of 68.6 percent from one year ago. That number was the highest down payment recorded since at least 2000, according to Attom’s records.

That median down payment was 6.6 percent of the median sales price for homes purchased with financing during Q3 2020, up from 5 percent the previous quarter, and up from 4.7 percent the year before.

The median loan amount also reached a new high of $275,500 during the third quarter. That number was up 10.3 percent from Q2 2020, and up 24.2 percent from Q3 2019, the highest point the figure has reached since 2000.