HousingWire

However, sales are up 20.8% year over year with low supply.

By Logan Mohtashami

Reports on housing data are headline-driven, and headlines are designed to cause folks to overreact in both positive and negative ways. We’ve seen our share of hyperbolic headlines in the housing reports this year, and for that reason, I have been compelled to reiterate my belief that the “too-hot” data will moderate to a more normalized trend. But, we hadn’t seen that moderation in any meaningful way until today’s new home sales data.

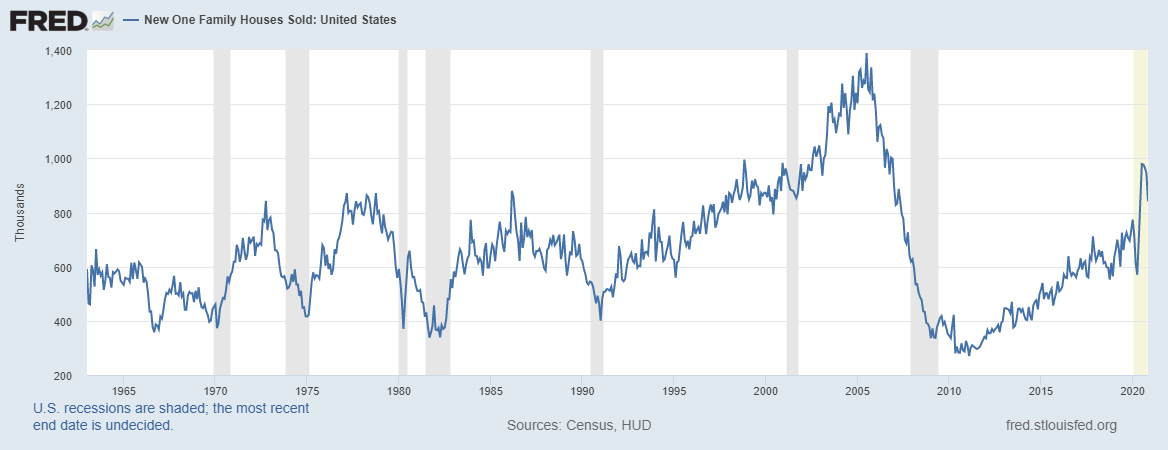

The new home sales marketplace has been showing abnormally fast growth for the last several months. This parabolic spike in recent new home sales from the lows in April to July’s highest levels has never happened in the data line.

But this kind of exponential growth is not sustainable. Exponential growth in any housing market data will eventually moderate. And that is what we see in the data for new home sales today, with negative revisions to previous reports.

From the Census Bureau: “Sales of new single-family houses in November 2020 were at a seasonally adjusted annual rate of 841,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 11% (±9.5%) below the revised October rate of 945,000, but is 20.8% (±19.5%) above the November 2019 estimate of 696,000.”

Despite what you may hear to the contrary, this is not the beginning of the end.

Those who follow me on social media are aware of my admonitions against overreacting to this moderation. All housing data will moderate to a normalized trend, but the trend data is still good. I warned about the negative headlines that would inevitably follow the moderation in sales in a recent article.

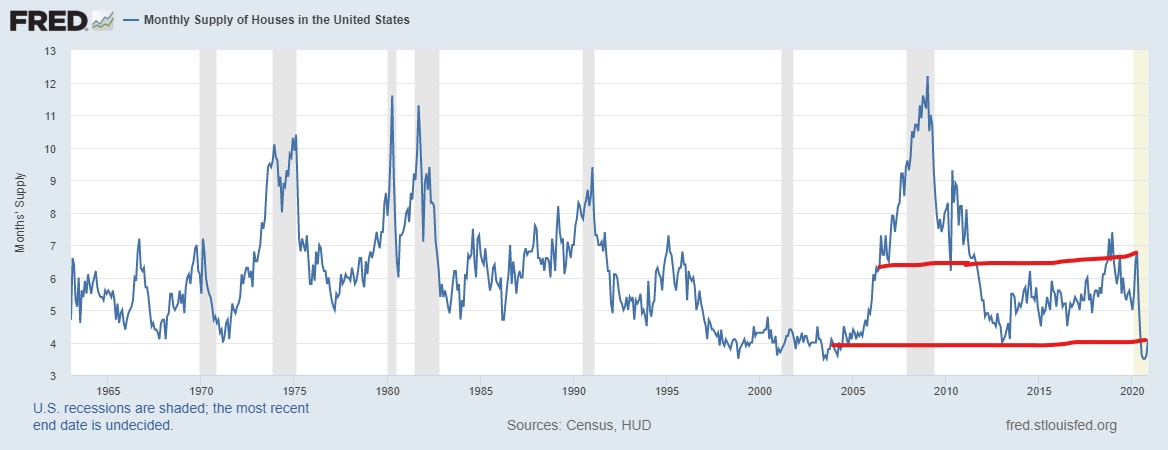

We don’t need to be concerned about the moderation in the new home sales data because inventory is still low.

From the Census Bureau:“The seasonally adjusted estimate of new houses for sale at the end of November was 286,000. This represents a supply of 4.1 months at the current sales rate.”

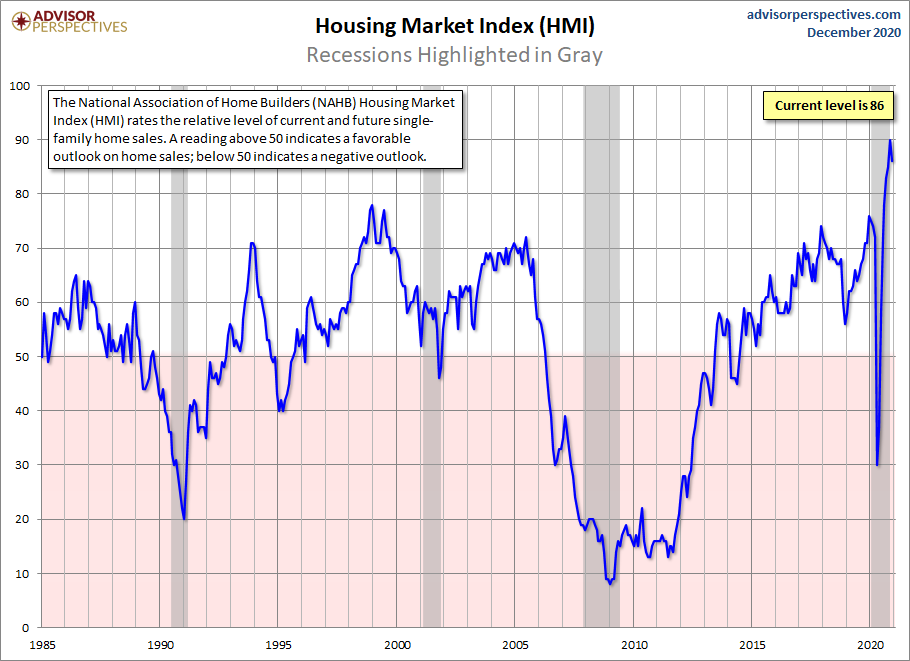

I’m sure you’ve heard the thesis that low inventory suppresses sales. First, there is no evidence for this, and second, this makes no sense. Home sales have gotten to pre-cycle highs with the inventory at pre-cycle lows. Builder confidence is primarily based on inventory.

When the monthly supply for new homes is below 4.3 months, builder confidence will be too high, and they will continue to build with much enthusiasm. The evidence is here with the NAHB’s builder’s confidence index, which will moderate in time as well.

When monthly supply is 4.4 to 6.4 months, builders become cautious about oversupplying a market. However, construction should continue at a slow and steady pace.

When monthly supply gets to 6.5 months and above, builders tend to halt construction. We saw this happen when inventory rose in 2018 and 2020.

The best way to predict builder behavior is to look at the three-month average of sales and supply. The month-to-month data is too wild and is frequently revised toward trend. Significant revisions happen a lot when data gets too hectic in a positive and negative direction.

According to the Census Bureau, we currently have 4.1 months of supply, with a three-month average of 3.73 months. From the builder’s perspective, this would be considered excellent. The monthly supply of new homes is the most critical data line we have for the American housing market.

I used the monthly supply chart in the previous expansion to prove my thesis that housing would have its weakest recovery ever in the years 2008-2019. However, the years 2020-2024 would be different. We finally cracked under 4.3 months and are on our way to finally start a year at 1.5 million housing starts in 2022.

This chart is the best chart to track what’s going on with housing starts.

Spoiler alert: A big theme of my 2021 predictions (which will come out next week) is that the hot housing data of 2020 will moderate. But there is no need to go into panic mode. When mortgage rates rise it will impact the new home sales market the most, and we should get to 4.3 months plus supply. However, we aren’t there yet.

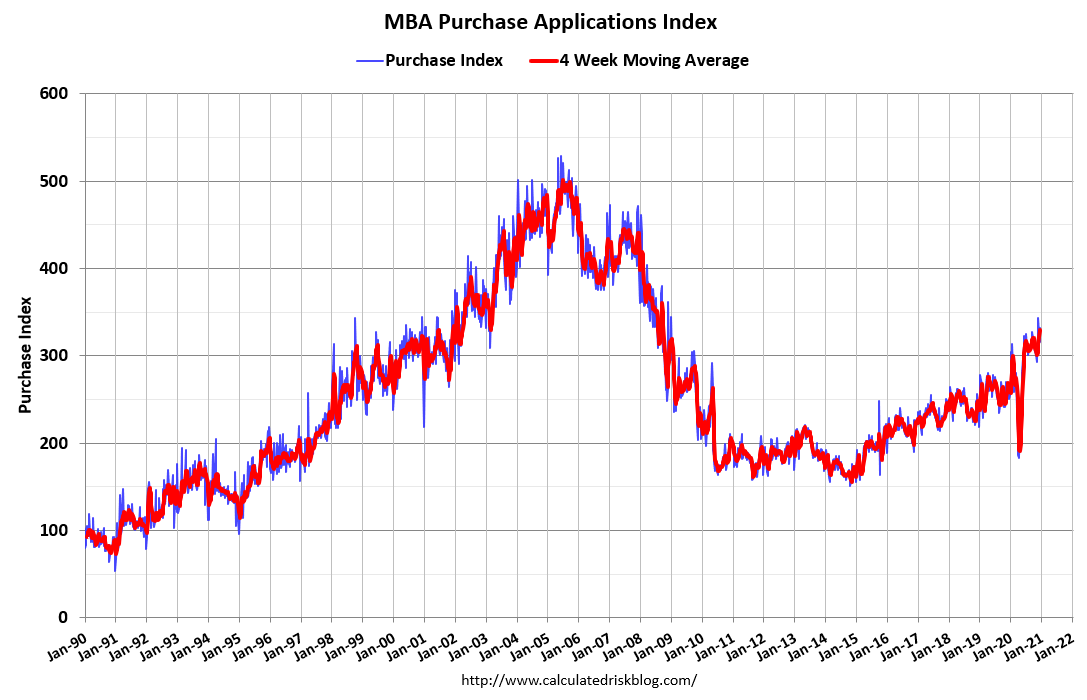

One final note: Purchase application data came out today. The data showed 26% year-over-year growth, making it 31 straight weeks of growth, averaging over 20%, compared to last year. All of this is make-up demand for the lost weeks due to COVID-19.

Logan Mohtashami is a Housing Data Analyst for HousingWire and a financial writer covering the U.S. economy with a specialization in the housing market. Additionally, he served as a senior loan manager at AMC Lending Group, which has been providing mortgages for California residents since 1987. Mohtashami’s work is frequently quoted in BankRate.com and Bloomberg. He has been an invited speaker at the Americatlyst, California Association Of Realtors and the National Association Of Women In Real Estate Business and other economic conferences.