Inman News

Appraisal gaps and bidding wars have people really worried

By Logan Mohtashami

A recent article published by CNBC showed that internet searches for the term “housing crash” had gone up 2,450% in the past month. A lot of folks are concerned about a housing market crash. They may be wishing for it, or they may be fearing that it will happen — but they are thinking about it.

I understand the concern. A home is your shelter. A home is not like bitcoin or even holding a piece of gold in your hand. You don’t need either of those to conduct the business of your everyday life. But when the housing bubble burst in the mid-2000s, many Americans were seriously impacted because their house was not only their shelter; it is also tied to work, their kid’s school, and the general well-being of their family. It is part of who you are.

This is why I stress that housing is the cost of shelter to your capacity to own the debt, not an investment. Real estate investors buy to flip a home for a profit or get rental income, but they’re not the majority of buyers in America each year. For the majority of mortgage holders, the loan is the cost of shelter. If taking a mortgage was an investment first and foremost, then the home we purchase would be the one that offered the most incredible long- or short-term return on investment. It would not be the home with the best floor plan, distance to work, how we feel about the city, or the one closest to the school of choice for our children.

Last year and this year have been crazy for real estate. A year ago, I was trying to convince people that housing wasn’t going to crash and that if they just waited until July 15 — when the June numbers would be published — they would see real estate start to rebound. People were still buying homes during the pandemic. Ordinary people needed shelter and wanted to take advantage of low mortgage rates and less competition. Think about all those Americans who bought homes to live in last year who are now grateful they don’t have to deal with this unhealthy housing market for buyers.

It’s a seller’s marketplace, but does that make it a bubble?

No, it’s not a bubble, and I wouldn’t even call it a booming sales demand cycle. We currently have an unhealthy housing marketplace because millions of Americans want to buy homes this year when inventory levels are low. This story is more about low inventory than speculative demand. Inventory is abnormally low when housing demographics are solid; we have low mortgage rates and some make-up demand for opportunities lost in 2020 during the COVID-19 shutdowns.

However, we don’t have anything that looks like the speculative credit bubble we saw from the years 2002-2005.

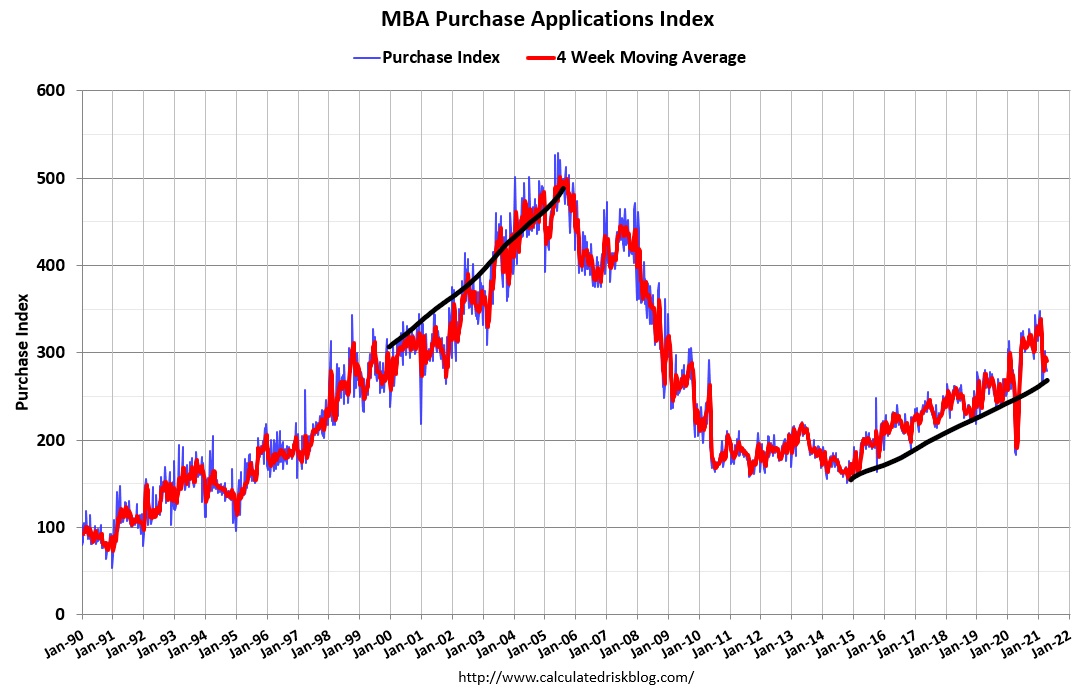

I’ve often said in the previous expansion that we should not expect to see the MBA Purchase Application Index get to the 300 level until the years 2020-2024. During the years 2008-2019, U.S. demographics didn’t favor increased demand for homes to get net demand back to the 300 level. The household formation wasn’t there, as the population was too young and too old to create mortgage demand to grow much higher. However, in the years 2020-2024, it would be different.

Now that we got to the 300 level before COVID-19 hit, it will be an epic battle between demographics versus affordability. Take a close look below; you can easily see the difference between now and then. Lending standards post-2010 are much different than what we had during the housing bubble years.

The housing market has exhibited some of the symptoms of an overheating marketplace — a fast-selling market with multiple bids per offering being common. These symptoms are why so many folks are concerned and searching the internet to confirm or deny the bubble hypothesis. But think of it this way, just because you have a dry cough and everyone is talking about COVID-19 doesn’t mean you have COVID-19. You might just have allergies.

If we continue with our analogy of a differential diagnosis, we would also need to confirm other symptoms before concluding we may be facing a bubble crash. Those symptoms would be a mass influx of cash buyers or investors and a marked increase in speculation buying on credit, but we don’t have either of these. Existing home sales only ended in 2020 with 130,000 more homes bought than 2017 levels.

What we do have is the best housing demographics ever recorded in U.S. history in the years 2020-2024, and we have the lowest mortgage rates ever recorded in U.S. history. That is pretty remarkable, and you would think that would be enough for a sexy headline.

Americans just want a home to live in, but they are being forced into dramatic bidding wars to get a place to live. For these folks, the very last thing on their minds is the possibility that home prices are going to crash next week. When rates rise, I believe the home price growth rate will cool, and the days on the market should grow.

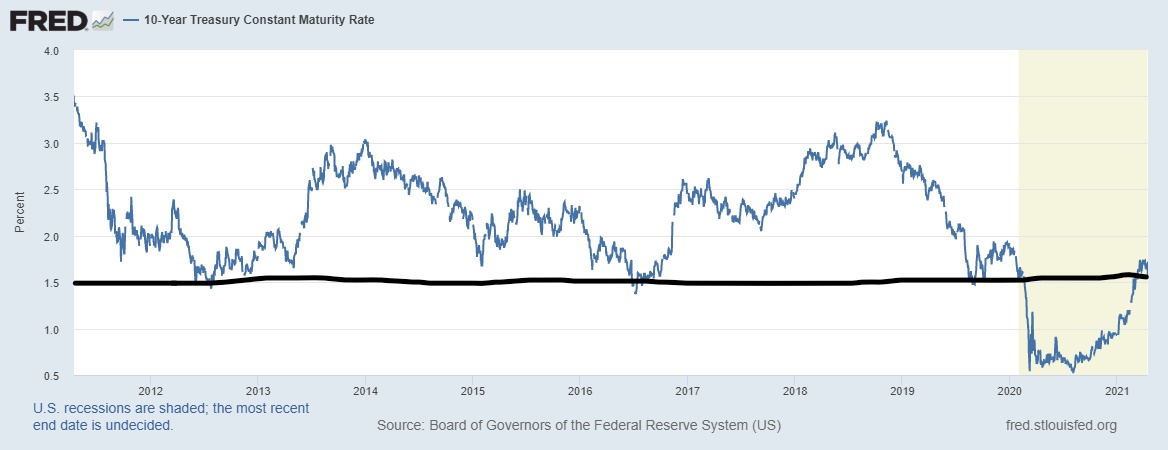

Our country is still recovering from COVID-19 and some sectors of the economy are still lagging as job growth is still being hindered by not being able to walk the earth freely just yet. We have a world economy, and the rest of the world isn’t doing as well as the U.S. on the economic consumption front. This sluggishness in the rest of the world is impacting the ability of the bond market to go higher.

I capped my 2021 forecast for the 10-year yield at 1.94% because COVID-19 is still with us. If rates and bond yields were just based on the U.S. economy, they should be higher. Higher bond yields and mortgage rates have cooled down the housing market in the previous expansion, and we don’t have that luxury now because of COVID-19. This is part of the Chaos Theory and Butterfly Effect of COVID-19. It has kept mortgage rates and the 10-year yield lower than if we had no COVID-19. This is also happening when we have solid retail sales, manufacturing data, and housing starts data.

The nature of yellow journalism in our society is that fear and loathing sell. Impending doom is somehow sexy and gets many eyeballs and clicks, whereas the standard economic truth does not. People like myself who spend their time yammering on about demographics, prime-age employment to population levels, and how much shelter inflation can move Core CPI, are pleasant to listen to when the double martini doesn’t do the job of putting you to sleep. I get it.

Lastly, I’m guessing that part of the appeal of the bubble crash hypothesis is just wishful thinking. I understand the temptation to believe that if home prices get too high, demand will eventually collapse to below 4 million existing home sales, and then prices could fall 35%, 55%, or even 75% in a year.

Let’s be honest: If you’re a housing bubble boy and the bubble started back again in 2012, you would need a 74.7% decline to justify the bubble thesis. Suppose you’re not a housing bubble boy, just a concerned citizen. How stupid would you feel if you bought at the top of the market, then your new neighbor gets essentially the same house for so much less? No one wants to be a sucker.

But, if we go back to our differential diagnosis analogy, we can conclude that this will not be the case for the current housing market. Overbought speculation in stocks can indeed lead to a crash quickly because the velocity margin debt moves 1-1 with stock prices. Housing isn’t like that. Housing is very sticky.

Housing is a “must-buy,” just like renting a place. It is like food, water, and clothing. Despite the economic downturn last year, we still have a lot of people in this country who make a decent amount of money and are of household formation age at a time when interest rates are low. Those people tend to buy homes. Then you have Americans who are moving up, down, investors and cash buyers. This makes housing demand stable in the years 2020-2024. Stable replacement buyers are the term I love to use, rather than using the term housing boom.

This is a complex concept for some people to understand, but since 1996, it has been infrequent to have existing home sales under 4 million for a month. Now, and for the next several years, we just have more Americans in their home-buying ages than we had from 1996-2019, and that will keep demand stable. Lending standards right now will prevent speculation credit from booming; this explains why the MBA purchase application data in 2018, 2019, 2020 and 2021 doesn’t look 2002,2003, 2004 and 2005.

Stick to the facts, don’t get sidelined by the sideshow, and we will all be better off.

Logan Mohtashami is a Housing Data Analyst for HousingWire and a financial writer covering the U.S. economy with a specialization in the housing market. Additionally, he served as a senior loan manager at AMC Lending Group, which has been providing mortgages for California residents since 1987. Mohtashami’s work is frequently quoted in BankRate.com and Bloomberg. He has been an invited speaker at the Americatlyst, California Association Of Realtors and the National Association Of Women In Real Estate Business and other economic conferences.