Inman News

By Jeff Tucker

Windermere’s Principal Economist Jeff Tucker looks at the Federal Reserve’s interest rate cut and what it means for the real estate market

The Fed has finally started cutting interest rates. The two big questions are: Why? And now what?

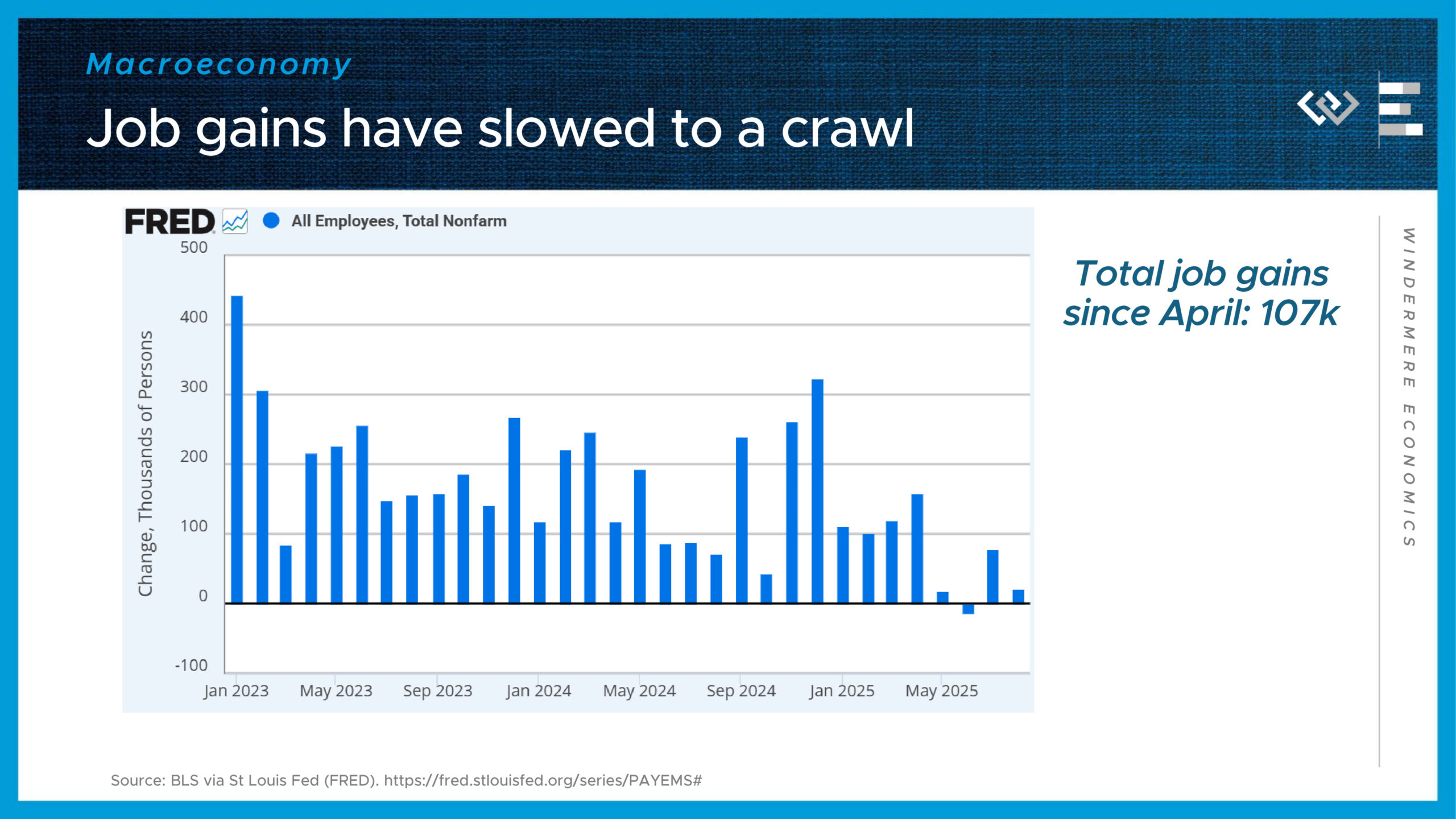

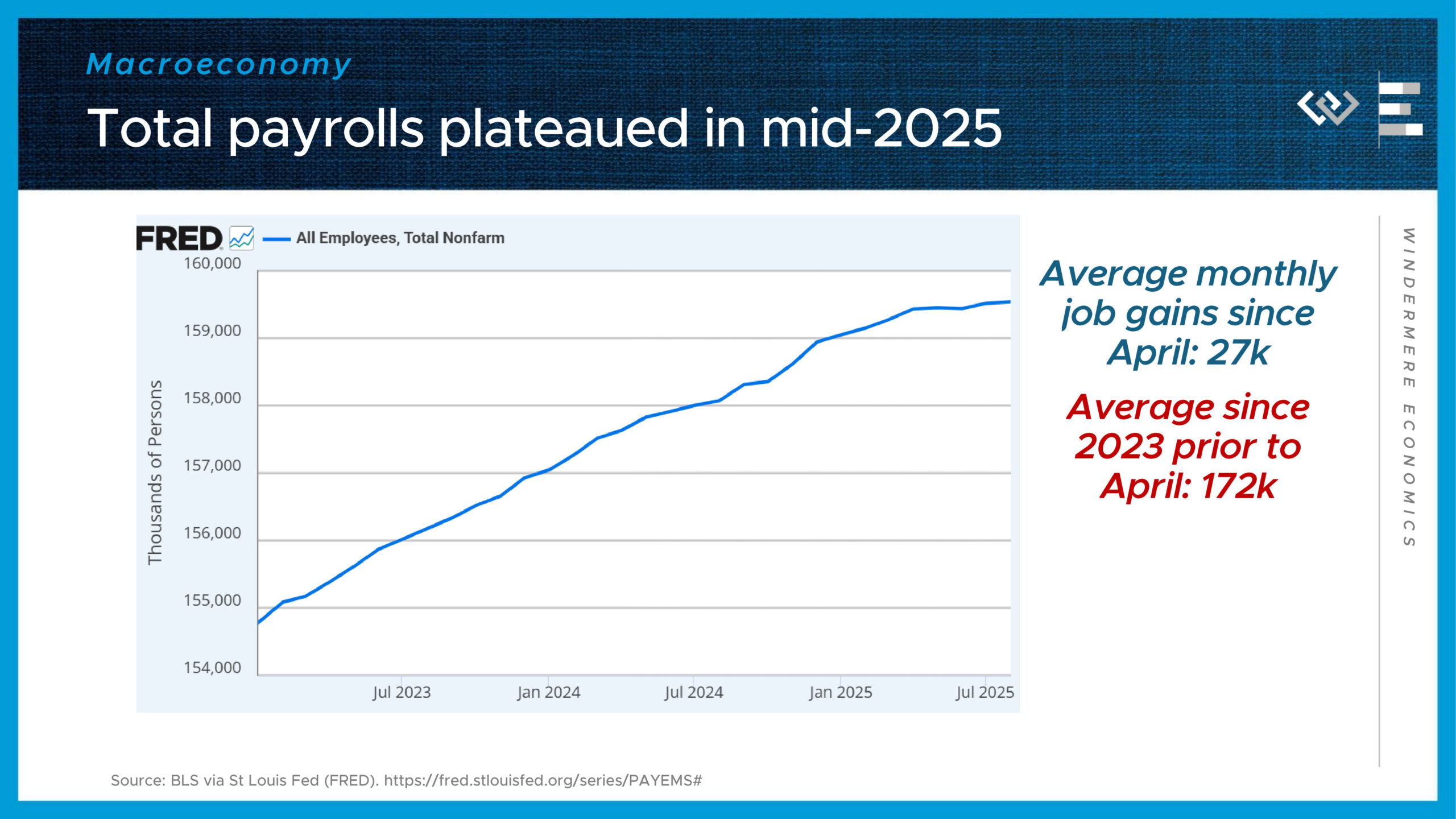

I’ll start with the why: The labor market has started showing signs of distress. The August jobs report delivered more bad news, continuing a streak of weak job growth since April.

The overall growth of nonfarm payrolls – the number of employed workers in the country — clearly passed a turning point this spring, as growth has slowed to a crawl.

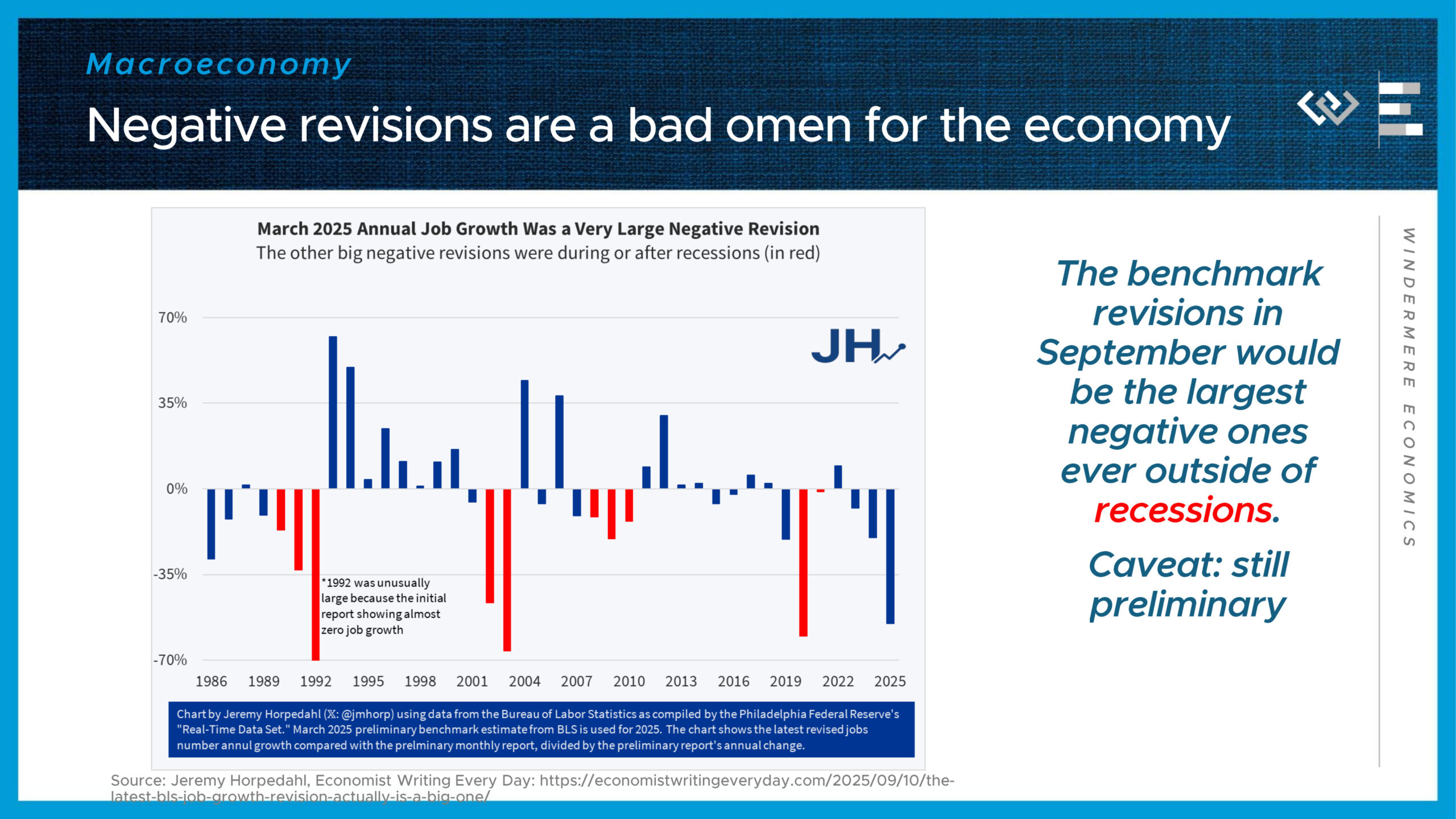

Moreover, the Quarterly Census of Employment and Wages just revised away more than half of the job growth previously estimated to have happened in the year ending March 2025, wiping out over 900,000 jobs originally thought to have been added in those 12 months.

Historically, as this chart by Jeremy Horpedahl highlights, big negative benchmark revisions, like the preliminary one released this month, have occurred during recessions. And big negative monthly revisions, like last month’s have been more common just before recessions.

That doesn’t mean a recession is around the corner, but it helps explain why the Fed is changing their posture to try to stop a recession before it gets going.

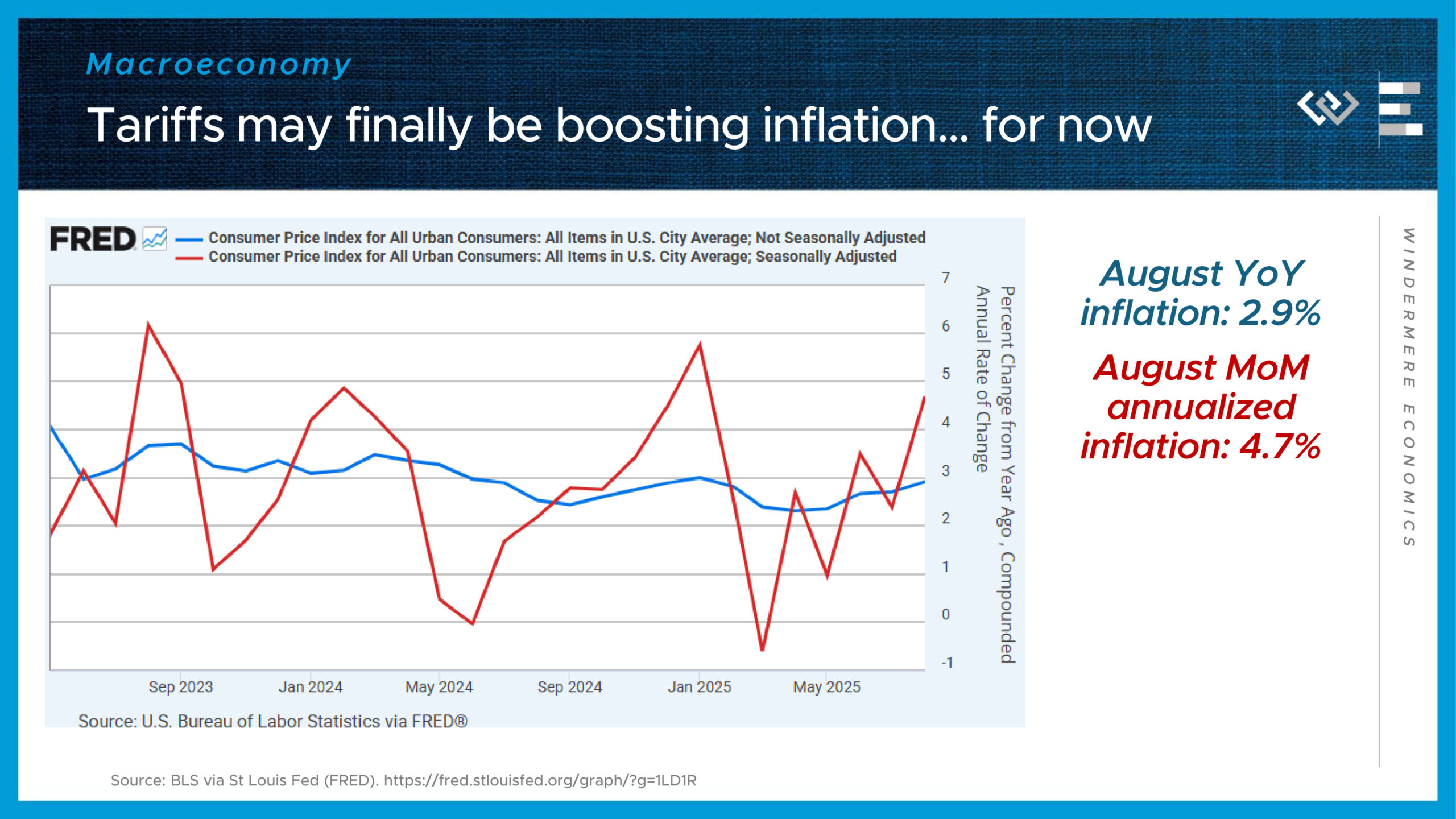

One challenge they’re facing, though, is that they have paused their fight against inflation before it was quite finished: Annual inflation stopped falling this spring and has now re-accelerated to nearly 3 percent, while the more volatile monthly inflation rate is running at 4.7 percent annualized.

Part of the reason the Fed is now willing to cut may be that they view some of this inflation as a transitory, one-time bump from tariffs, that they are willing to look through, but I think the biggest reason is just that the warning sirens in the labor market became too loud to ignore.

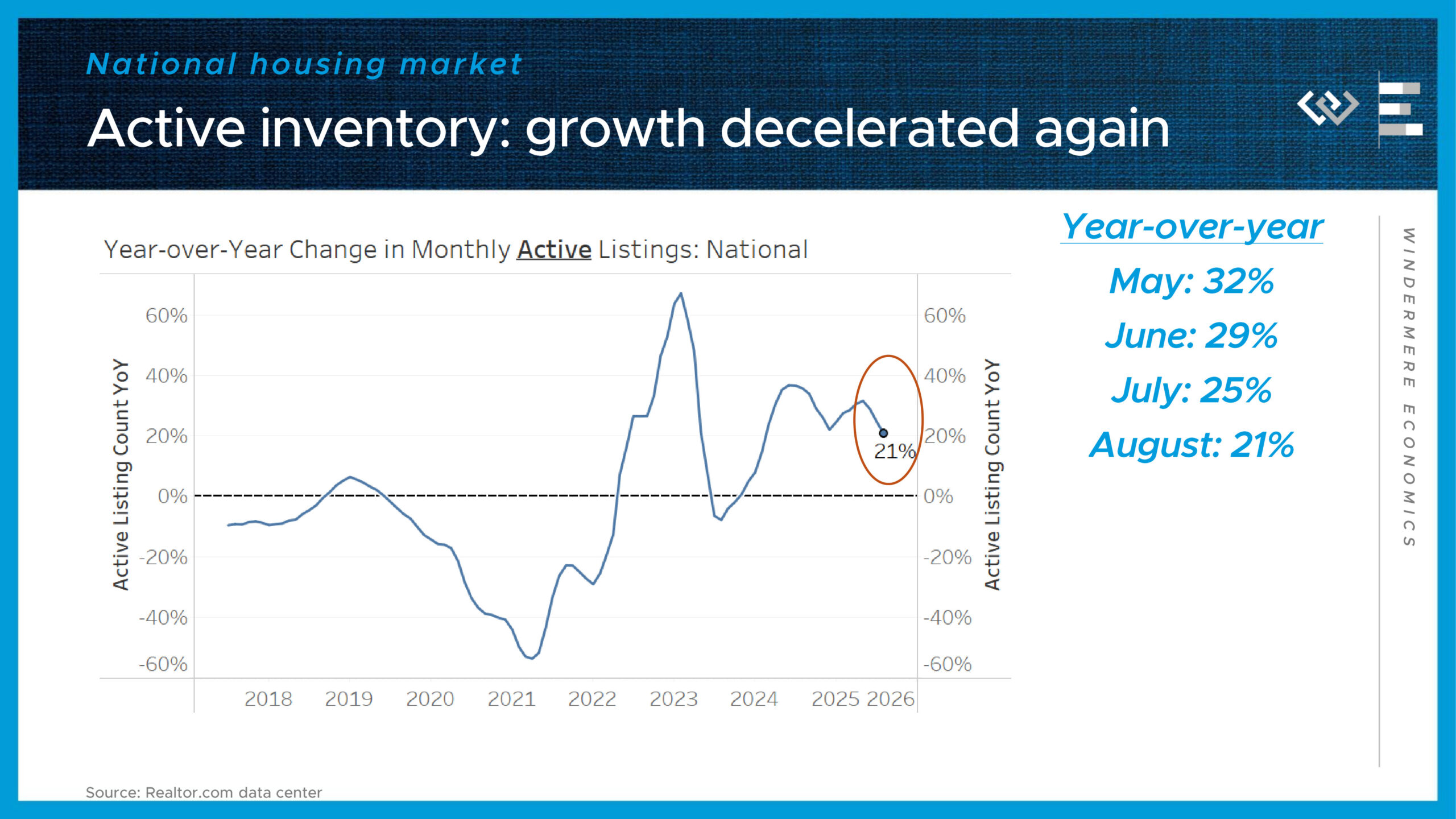

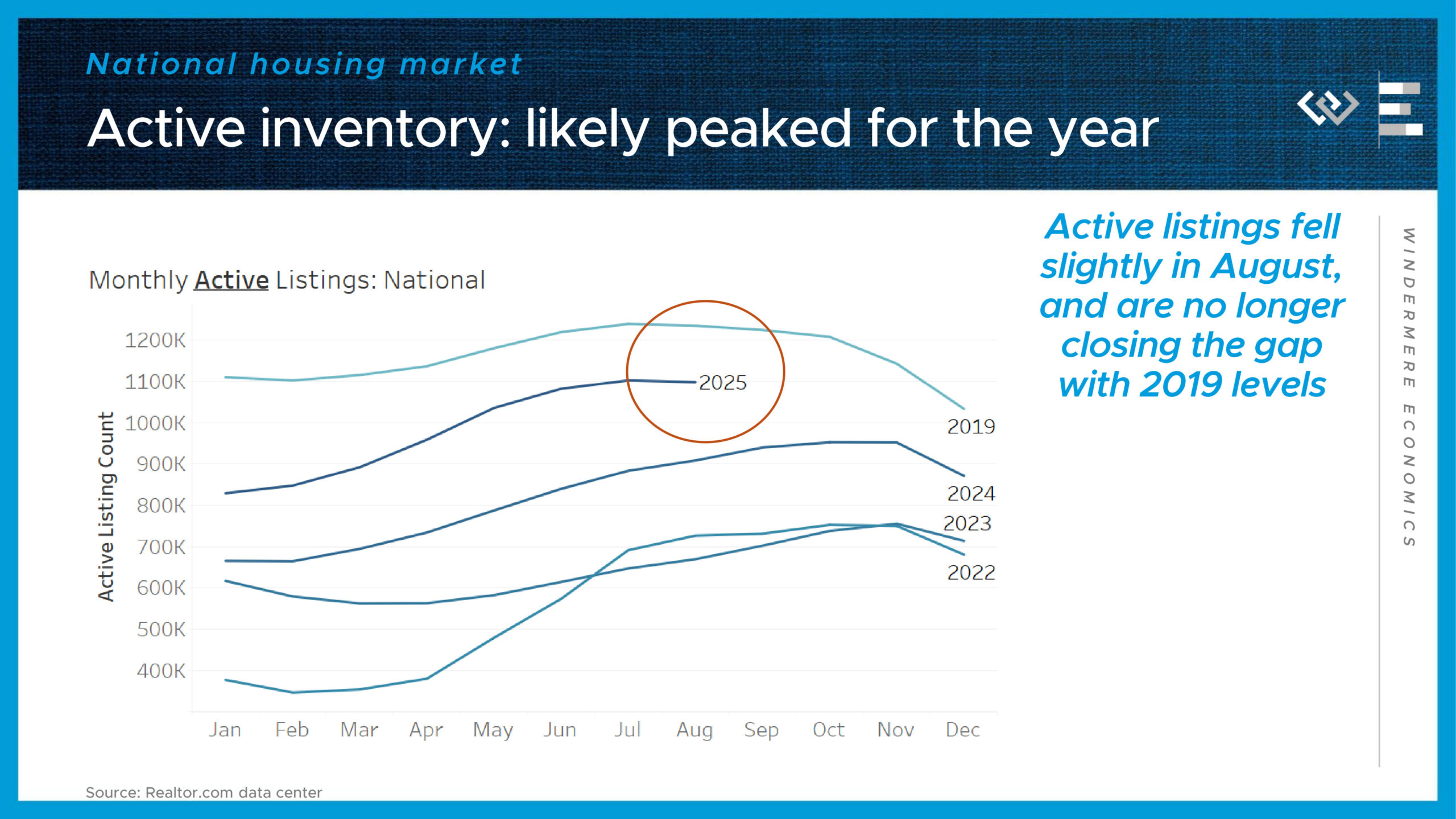

Turning to the housing market: The balance of power has swung in buyers’ favor this year, thanks to higher inventory. However, it’s now clear that inventory growth passed an inflection point: For the third month in a row, the pace of growth of inventory has come down again. Now it’s down to just 21 percent growth from August of last year.

At the end of August, there were just under 1.1 million active listings on the market, down slightly from July, while each of the past three years saw inventory grow in August. This means buyers are still favored in many markets, but they can’t count on that pendulum to keep swinging further in their favor.

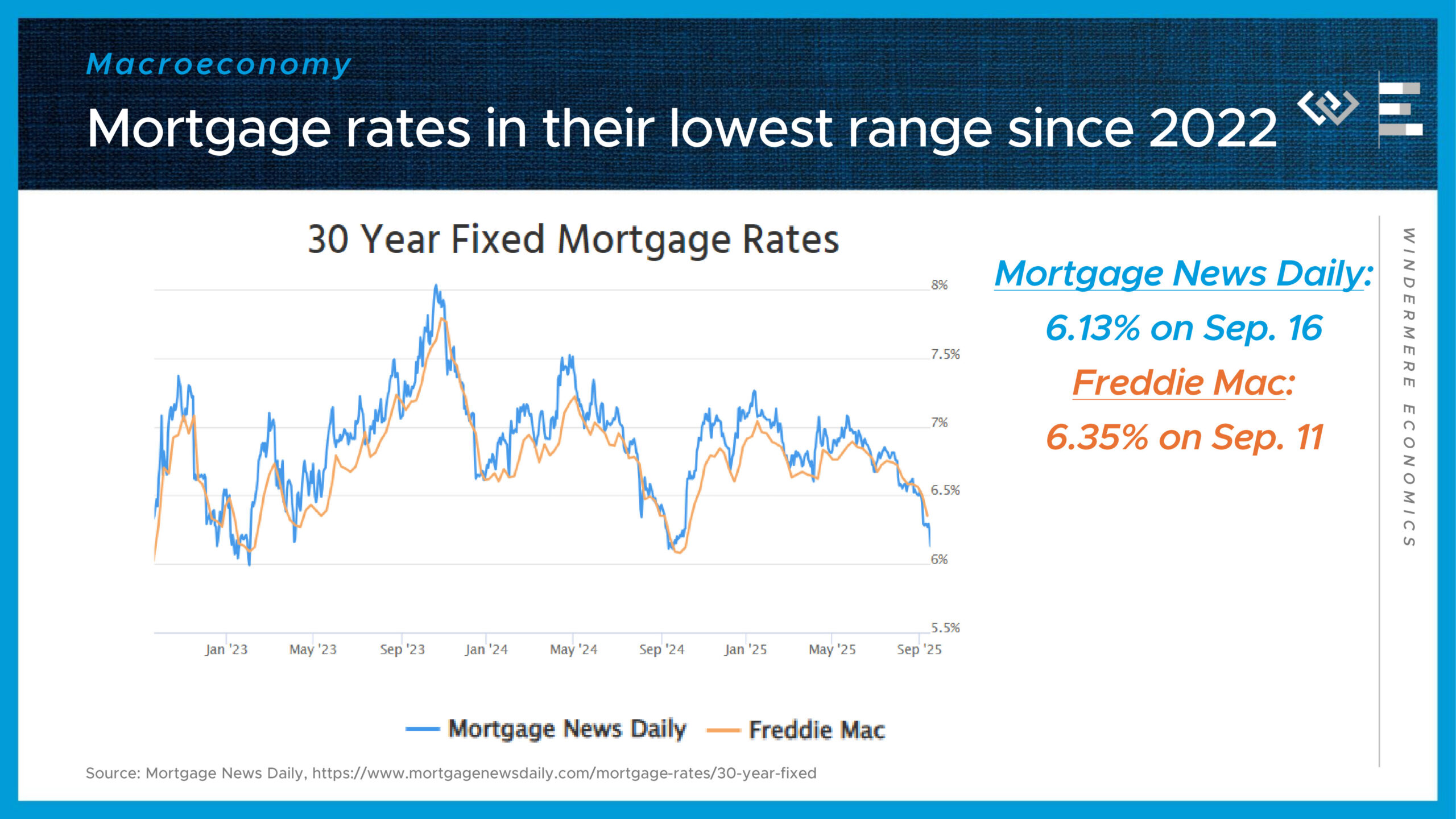

Especially because of the huge news for everyone in the housing market, mortgage rates have fallen to the neighborhood of 6.125 percent, roughly their lowest level since 2022. Investors were anticipating this rate cut by the Fed, and if anything, the fact that the Fed was willing to press ahead with cutting rates, in spite of firmer inflation data, demonstrates their commitment to focus on helping the labor market with easier monetary policy, while setting aside inflation fighting to another day.

Maybe more than anything, that change of posture by the Fed is helping to bring mortgage rates low enough that well-qualified borrowers are starting to see a five-handle without paying any points. There’s no guarantee that the low rates will last; just look at what happened last October.

Therefore, I’d advise everyone to strike while the iron’s hot. If rates do fall further this winter, well, you can always refi then.

As Principal Economist for Windermere Real Estate, Jeff Tucker analyzes economic data to explain its impact on national and regional housing markets. His insights and analysis empower real estate professionals and consumers to make informed decisions. Jeff has 10 years of professional experience as an economist, including over 5 years at Zillow, as well as Amazon, AirDNA, and in economic consulting. While at Zillow, Jeff researched housing market trends, authored economic outlook reports for the Board of Directors, presented to policy makers like the White House Council of Economic Advisers, and served as media spokesperson for the economic research team. Jeff received his B.A. in Economics from Amherst College and his M.A. in Economics from the University of Washington.