Calculated Risk

Early reports suggest NAR reported sales will rebound to mid-4 million range in January

By Bill McBride

This is the second look at local markets in January. I’m tracking about 40 local housing markets in the US. Some of the 40 markets are states, and some are metropolitan areas. I’ll update these tables throughout the month as additional data is released.

Closed sales in January were mostly for contracts signed in November and December. Since 30-year fixed mortgage rates were over 6% for all of November and December closed sales were down significantly year-over-year in January, however, the impact was probably not as severe as for closed sales in December (rates were the highest in October and November 2022 when contracts were signed for closing in December).

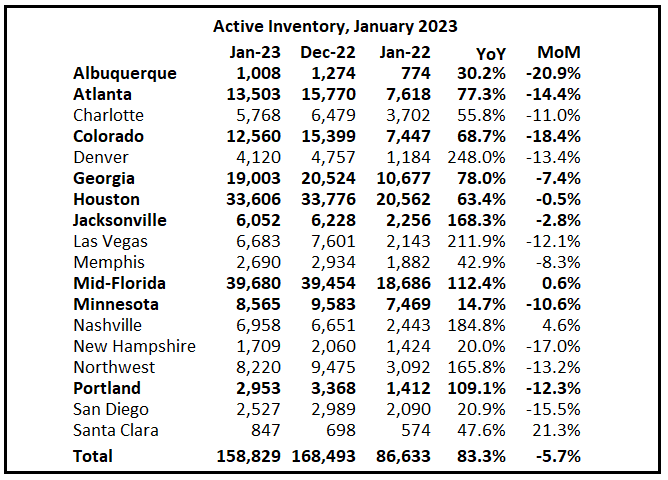

Active Inventory in January

Here is a summary of active listings for these housing markets in January.

Inventory in these markets were down 25% YoY in January a year ago and are now up 83% YoY! So, this is a significant change from early 2022, and about the same YoY inventory increase as in December (up 81% YoY).

Notes for all tables:

- New additions to table in BOLD.

- Northwest (Seattle), Santa Clara (San Jose), Jacksonville, Source: Northeast Florida Association of REALTORS®

- Totals do not include Atlanta or Denver (included in state totals)

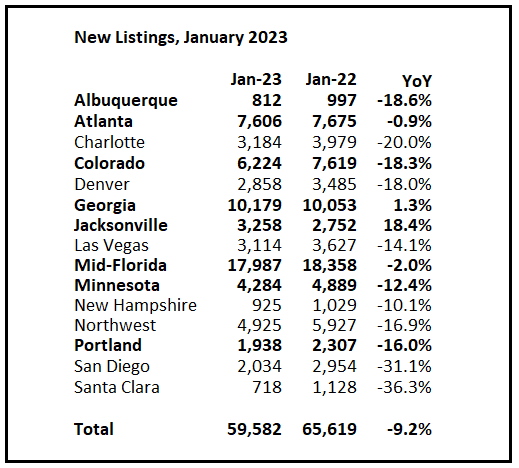

New Listings in January

And here is a table for new listings in January. For these areas, new listings were down 9.2% YoY. Potential sellers that are locked into their current homes with low mortgage rates has pushed down new listings.

Last month, new listings in these markets were down 21.7% YoY. This is a significantly smaller YoY decline in new listings, and something to watch. There are certain markets – like Georgia and Florida – where new listings are up YoY!

Realtor.com is showing a much smaller YoY decline in new listings in January too.

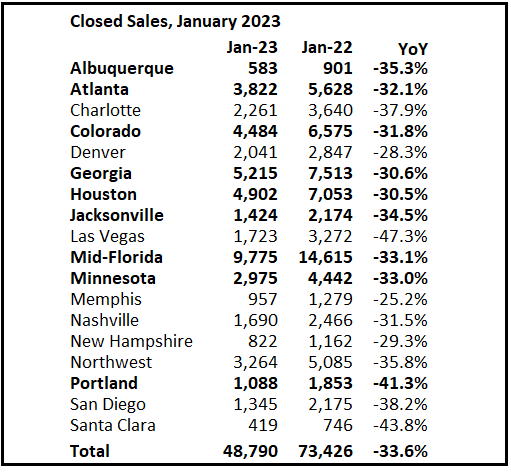

Closed Sales in January

And a table of January sales.

In January, sales were down 33.6% in these markets. In December, these same markets were down 37.9% YoY Not Seasonally Adjusted (NSA).

This is a smaller YoY decline than in December for these early reporting markets. The early data suggests NAR reported sales will rebound in January to the mid-4 million range (Seasonally adjusted annual rate) from 4.02 million SAAR in December.

This will still be a significant YoY decline, and the 17th consecutive month with a YoY decline.

Note: Even if existing home sales activity bottomed in December, there are usually two bottoms for housing – the first for activity and the second for prices.