Calculated Risk

By Bill McBride

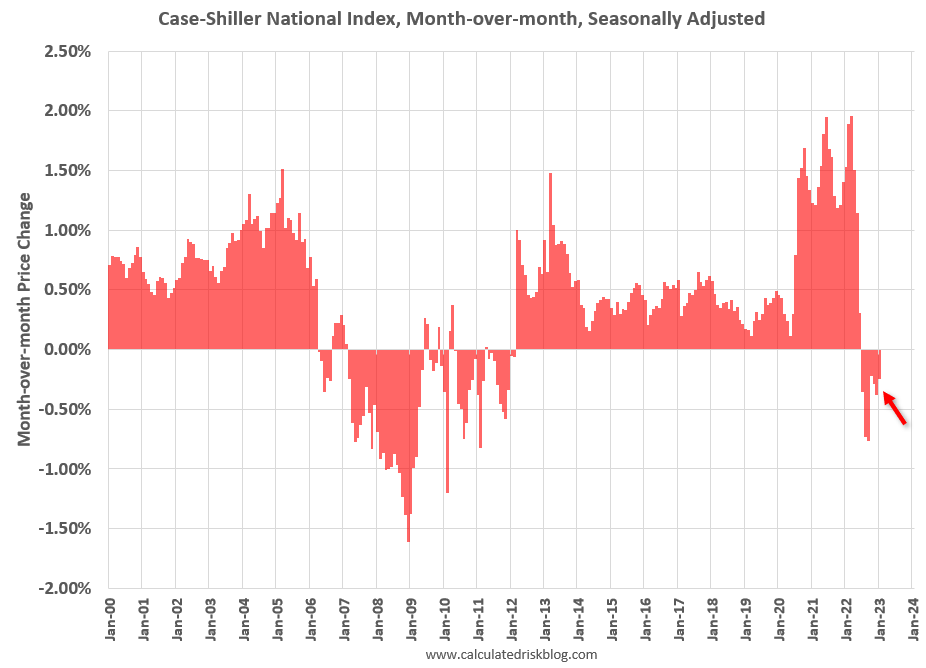

Both the Case-Shiller House Price Index (HPI) and the Federal Housing Finance Agency (FHFA) HPI for January were released today. Here is a graph of the month-over-month (MoM) change in the Case-Shiller National Index Seasonally Adjusted (SA).

The Case-Shiller Home Price Indices for “January” is a 3-month average of November, December and January closing prices. November closing prices include some contracts signed in September, so there is a significant lag to this data.

The MoM decrease in the seasonally adjusted Case-Shiller National Index was at -0.25%. This was the seventh consecutive MoM decrease, and a slightly smaller decrease than in December.

On a seasonally adjusted basis, prices declined in 15 of 20 Case-Shiller cities on a month-to-month basis. The largest monthly declines seasonally adjusted were in Seattle (-1.5%), Las Vegas (-1.1%), and Denver (-1.0%). Seasonally adjusted, San Francisco has fallen 13.2% from the peak in May 2022 and Seattle is down 11.4% from the peak. All 20 cities have seen price declines from the recent peak (SA).

FHFA House Price Index

On the FHFA index: FHFA House Price Index Up 0.2 Percent in January; Up 5.3 Percent from Last Year

U.S. house prices rose in January, up 0.2 percent from December, according to the Federal Housing Finance Agency (FHFA) seasonally adjusted monthly House Price Index (HPI®). House prices rose 5.3 percent from January 2022 to January 2023. The previously reported 0.1 percent price decline in December 2022 remained unchanged.

For the nine census divisions, seasonally adjusted monthly price changes from December 2022 to January 2023 ranged from -0.6 percent in the Pacific division to +2.0 percent in the New England division. The 12-month changes were -1.5 percent in the Pacific division to +9.6 percent in the South Atlantic division.

“U.S. house prices changed slightly in January, continuing the trend of the last few months,” said Dr. Nataliya Polkovnichenko, Supervisory Economist, in FHFA’s Division of Research and Statistics. “Many of the January closings, on which this month’s HPI is constructed, reflect rate locks after mortgage rates declined from their peak in early November. Inventories of available homes for sale remained low.”

emphasis added

The monthly index increased 0.2% in January. Here is a graph from the FHFA report showing the annual change by region for January 2023 compared to January 2022. Prices have increased YoY everywhere. Note that the Year-over-year increase is smaller this year, compared to the YoY increase in January 2022 in all of the nine regions – especially in the Pacific and Mountain regions.

Case-Shiller House Prices

From S&P: S&P Corelogic Case-Shiller Index Continued to Decline in November

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.8% annual gain in January, down from 5.6% in the previous month. The 10-City Composite annual increase came in at 2.5%, down from 4.4% in the previous month. The 20-City Composite posted a 2.5% year-over-year gain, down from 4.6% in the previous month.

Miami, Tampa, and Atlanta again reported the highest year-over-year gains among the 20 cities in January. Miami led the way with a 13.8% year-over-year price increase, followed by Tampa in second with a 10.5% increase, and Atlanta in third with an 8.4% increase. All 20 cities reported lower prices in the year ending January 2023 versus the year ending December 2022.

…

Before seasonal adjustment, the U.S. National Index posted a -0.5% month-over-month decrease in January, while the 10-City and 20-City Composites posted decreases of -0.5% and -0.6%, respectively.

After seasonal adjustment, the U.S. National Index posted a month-over-month decrease of -0.2%, while both the 10-City and 20-City Composites posted decreases of -0.4%.

In January, before seasonal adjustment, 19 cities reported declines with only Miami reporting an increase at 0.1%. After seasonal adjustment, 15 cities reported declines while Miami, Boston, Charlotte, and Cleveland had slight increases.

“2023 began as 2022 had ended, with U.S. home prices falling for the seventh consecutive month,” says Craig J. Lazzara, Managing Director at S&P DJI. “The National Composite declined by 0.5% in January, and now stands 5.1% below its peak in June 2022. On a trailing 12-month basis, the National Composite is only 3.8% ahead of its level in January 2022, a result also reflected in our 10- and 20-City Composites (both +2.5% year-over-year).

“January’s market weakness was broadly based. Before seasonal adjustment, 19 cities registered a decline; the seasonally adjusted picture is a bit brighter, with only 15 cities declining. With or without seasonal adjustment, most cities’ January declines were less severe than their December counterparts.

emphasis added

This graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is down 0.4% in January (SA) and down 4.5% from the recent peak in June 2022. The Composite 20 index is down 0.4% (SA) in January and down 4.7% from the recent peak in June 2022. The National index is down 0.2% (SA) in January and is down 3.0% from the peak in June 2022.

The Composite 10 SA is up 2.5% year-over-year. The Composite 20 SA is up 2.5% year-over-year. The National index SA is up 3.8% year-over-year.

House Prices and Inventory

This graph below shows existing home months-of-supply, inverted, from the National Association of Realtors® (NAR) vs. the seasonally adjusted month-to-month price change in the Case-Shiller National Index (both since January 1999 through January 2023). Note that the months-of-supply is not seasonally adjusted.

The last nine months are in black showing a possible shift in the relationship, and prices are now falling with low levels of inventory!

In January, the months-of-supply was at 2.9 months, and the Case-Shiller National Index (SA) decreased -0.25% month-over-month. The last seven months appear to be outliers with prices falling even though months-of-supply is still somewhat low. Historically prices haven’t declined until inventory reached 6 months of supply. NOTE that the NAR appears to include some pending sales in their inventory, and inventory is probably up more than the NAR is reporting.

In the February existing home sales report, the NAR reported months-of-supply declined to 2.6 months.

The year-over-year Case-Shiller house price increase was at expectations.

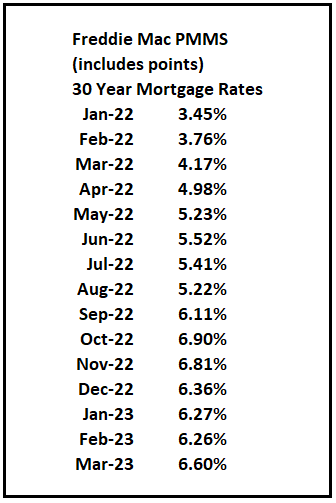

Here are the 30-year mortgage rates according to the Freddie Mac PMMS:

The January report was mostly for contracts signed in the September through December period – and was likely impacted by the surge in rates in October.

The impact from higher rates in October and November will also negatively impact the Case-Shiller index for “February”.

Note that mortgage rates increased in March, but that will not impact the Case-Shiller index for many months.

Comparing to Median House Prices

Here is a comparison of year-over-year change in median house prices from the NAR and the year-over-year change in the Case-Shiller index. Median prices are distorted by the mix and repeat sales indexes like Case-Shiller and FHFA are probably better for measuring prices. However, in general, the Case-Shiller index follows the median price.

The median price was down slightly year-over-year in February, and Case-Shiller will follow.