Calculated Risk

By Bill McBride

New Listings at Record Low for March

Here is a graph of new listing from Realtor.com’s March 2023 Monthly Housing Market Trends Report showing new listings were down about 20% year-over-year in March. New listings are at a record low for March, the year-over-year decline was larger in March than in February. From Realtor.com:

In March, the number of homes newly-listed for sale declined by 20.1% compared to the same time last year. This is a higher rate of decline than last month’s 15.9% decrease and new listings remained 29.7% below pre-pandemic 2017 to 2019 levels.

For the local markets I track that have reported so far, are show new listings were down about the same in March as in February.

For these areas, new listings were down 16.8% YoY. … Last month, new listings in these markets were also down 16.8% YoY.

Impact on Active Inventory

The following graph shows the seasonal pattern for active single-family inventory since 2015 from Altos Research. The red line is for 2023. The black line is for 2019.

Single-family active existing home inventory was up 59.1% compared to the same week in 2022, and down 50.9% compared to the first week in 2019. Inventory is still historically low. A key will be when inventory starts increasing in 2023 – that might have started in early April.

For new homes, there are 5.0 months of homes under construction (blue line below) – well above the normal level. This elevated level of homes under construction is due to supply chain constraints. There are 1.35 months of completed homes for sale (red). This is close to the normal level.

It is likely we will see a sharp increase in completed inventory over the next several months. It appears cancellations are now falling for new home builders (cancellations impact the New Home sales report from the Census Bureau).

And for housing starts there are a near record 1.69 million units under construction.

Red is single family units. Currently there are 734 thousand single family units (red) under construction (SA). This is 81 thousand below the recent peak in April and May. Single family units under construction have peaked since single family starts are now declining. Blue is for 2+ units. Currently there are 957 thousand multi-family units under construction. This is the highest level since November 1973!

30-Year Mortgage Rates Have Bounced between 6% and 7%

The following graph from MortgageNewsDaily.com shows mortgage rates since January 1, 2020. 30-year mortgage rates were at 6.42% on April 12th, up from 6.0% in early February, and down from the recent high of over 7% in early March – and still up sharply year-over-year.

A year ago, the payment on a $500,000 house, with a 20% down payment and 4.98% 30-year mortgage rates, would be around $2,142 for principal and interest. The monthly payment for the same house, with house prices up 2% YoY and mortgage rates at 6.42%, would be $2,582 – an increase of 20%.

But if we compare to two years ago, there is huge difference in monthly payments. In April 2021, the payment on a $500,000 house, with a 20% down payment and 3.06% 30-year mortgage rates, would be around $1,699 for principal and interest. The monthly payment for the same house, with house prices up 23% over two years and mortgage rates at 6.42%, would be $3,084 – an increase of 81%.

This increase in mortgage rates is probably the key reason new listings have declined sharply year-over-year – especially since a large number of homeowners refinanced at lower rates in 2020, 2021 and early 2022.

This is very different from the housing bust, when many homeowners were forced to sell as their teaser rates expired and they could not afford the fully amortized mortgage payment. The current situation is similar to the 1980 period, when rates also increased quickly.

House Prices

Reported YoY house price growth is still positive, but the Case-Shiller National Index slowed to 3.8% YoY in January.

The MoM decrease in the seasonally adjusted Case-Shiller National Index was at -0.25%. This was the seventh consecutive MoM decrease, and a slightly smaller decrease than in December.

Other measures of house prices indicated further declines in February. The NAR reported median prices were down 0.2% YoY in February. Black Knight reported prices were up 1.9% YoY, and Freddie Mac reported house prices were up 1.1% YoY in January. Here is a comparison of year-over-year change in the FMHPI, median house prices from the NAR, and the Case-Shiller National index.

The FMHPI and the NAR median prices appear to be leading indicators for Case-Shiller. The median price was down YoY in February, and based on the recent trend, the FMHPI will be negative year-over-year in March (reported at the end of April) – and Case-Shiller will follow within a few months.

Sales

We have seen declines in both new and existing home sales due to higher mortgage rates. The NAR reported sales were at a “seasonally adjusted annual rate of 4.58 million in February. Year-over-year, sales fell 22.6% (down from 5.92 million in February 2022).” This was in line with the local markets I track for February.

The early local market reports suggest a similar year-over-year decline in closed sales NSA in March. It is possible that existing home sales, seasonally adjusted, bottomed in December and January. But a bottom in existing home sales doesn’t mean other measures are near a bottom. There are usually two bottoms for housing.

[T]here will be two bottoms for housing: one for activity and the other for prices. Existing home sales may have already bottomed, but we will see further declines in residential investment. Prices – especially in real terms – will be under pressure for some time.

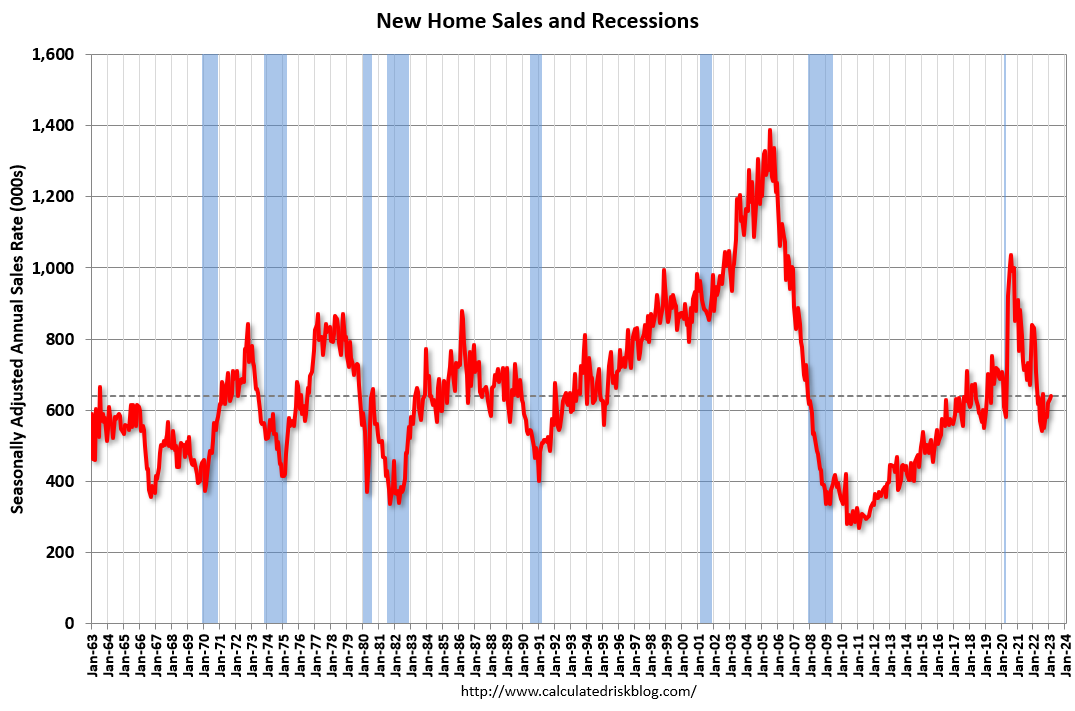

And the Census Bureau reported “Sales of new single‐family houses in February 2023 were at a seasonally adjusted annual rate of 640,000”, down 19.0% YoY from February 2022.

The lack of existing homes for sales is good news for homebuilders.

Rents Continue to Soften

Year-over-year rent growth continues to decelerate, household formation has slowed, and as more supply comes on the market, we will likely see rents under pressure in many markets.

Conclusions

We have seen a significant year-over-year decline in new and existing home sales, although it is likely that activity has bottomed (but not prices). House prices are under pressure due to higher mortgage rates but prices are being supported by low levels of inventory.

Existing home sales will likely be down about the same year-over-year NSA in March as in February. Housing starts will probably show further declines – especially multi-family – and still a near record number of housing units under construction.