Inman News

The trend toward remote work, along with the rising value of stock portfolios and home values, has fueled the demand.

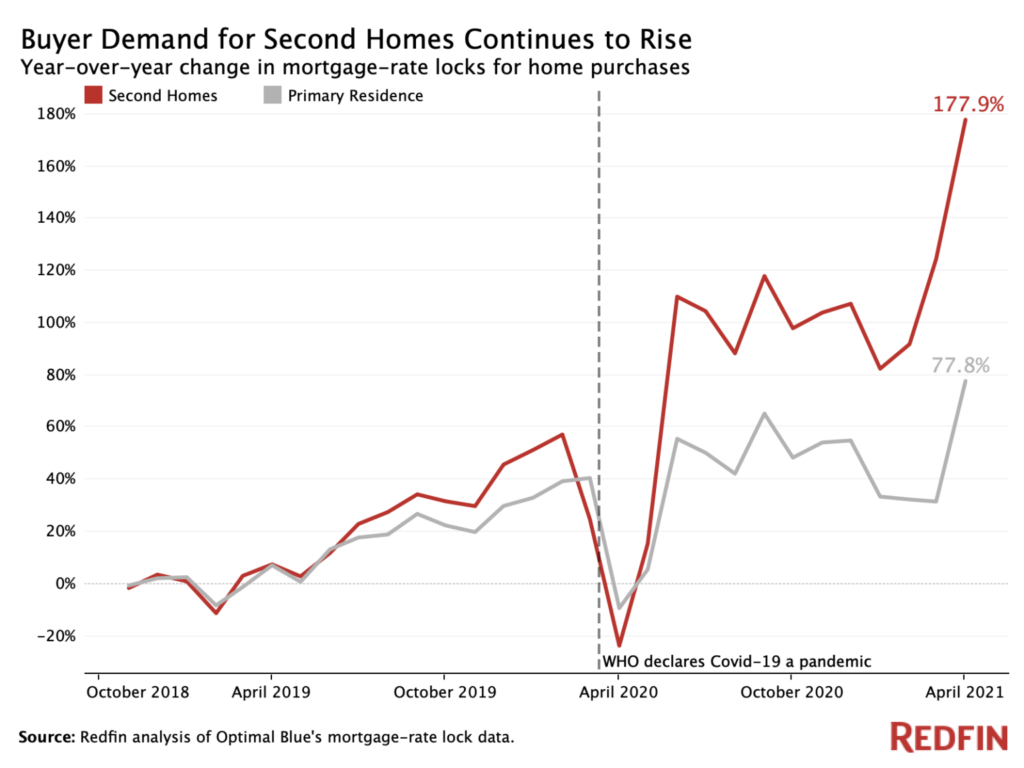

Demand for second homes and investment properties continues to hold steady at more than double pre-pandemic levels, despite a government order that mortgage giants Fannie Mae and Freddie Mac limit their appetite for loans backed by second homes and investment properties.

A Redfin analysis of mortgage data collected by real estate analytics firm Optimal Blue found rate locks for second homes were up 178 percent in April from a year ago. The record increase is due in part to the fact that demand for homes plummeted 24 percent last April as the pandemic got underway.

But the rise in demand for second homes is more than double the jump seen for primary residences, Redfin noted, likely driven by the freedom to work remotely and the rising value of many wealthy individuals’ stock portfolios and home values.

“The combination of the wealthy becoming wealthier, remote work turning into the new normal and low mortgage rates is creating an ideal environment for affluent Americans to buy vacation homes,” said Redfin Chief Economist Daryl Fairweather in a statement. “As long as the economy continues to grow, I don’t foresee demand for second homes slowing down anytime soon.”

Myrtle Beach, South Carolina, Redfin agent Lisa C. Smith said the same forces are motivating investor demand.

“A lot of investors are noticing the intensity of the rental market here and snapping up homes and condos for short-term rentals,” Smith said. “They feel property is still affordable and taxes are cheaper in this area than other parts of the country. There are new listings hitting the market every day because homeowners are realizing now is a great time to sell their vacation properties. Sellers have seen prices go up, and many of them are able to sell and pocket the equity.”

New limits on Fannie and Freddie

The demand for second homes and investment properties comes as Fannie and Freddie have started limiting their purchases of loans backed by such homes. As part of an attempt to help the mortgage giants raise the capital needed to exit government conservatorship, the Treasury Department and the Federal Housing Finance Agency in January placed stricter limits on riskier loans, capping purchases of mortgage secured by second homes and investment properties at 7 percent.

In a March 22 letter protesting the move, the Community Home Lenders Association said that if Fannie and Freddie implement the restrictions by capping purchases from each lender, the “likely result will be that … total loan volume purchase(s) of restricted loans will be far below (the 7 percent cap) — thus exacerbating the negative impact on access to mortgage credit.”

The National Association of Relators voiced similar concerns, claiming, “Any considerations to limit financing on second homes, investor properties or entry-level borrowers will have a negative impact on borrowing costs and a broader impact on the rental market. This would only undermine [Fannie and Freddie’s] ability to fund many of their charter duties and appropriately serve U.S. taxpayers and consumers.”

Fannie Mae informed lenders in a March 10 letter it would be implementing the changes on April 1, and Freddie Mac followed suit on March 31, announcing new restrictions that took effect on April 15 and May 1.

Lenders who can’t sell loans to Fannie and Freddie are likely to increase down payment requirements, and charge higher interest rates and points.

A recent analysis by Mike Vough, Product Manager for Black Knight’s Secondary Marketing Technologies Group, shows the impact of the caps when lenders try to sell loans backed by second homes and investment properties in secondary markets.

For second homes, bulk pricing is down 1.5 points, which translates into a $4,500 reduction in the price investors will pay for a $300,000 loan. For investment properties, pricing has improved slightly in the last two weeks, but is still down by 0.65 points, which means lenders will get $2,000 less for a $300,000 loan.

To make up for the reduced value of these loans to secondary market investors, lenders will need to charge borrowers more — either in the form of higher rates, or by charging up-front fees.

The 7 percent cap “is causing headaches for secondary marketing managers. Not only do these professionals have to more closely manage the population of loans delivered to [Fannie and Freddie], but they are seeing other investors begin to follow suit, imposing their own caps and/or back off pricing for investment and second home properties,” Vough wrote in a previous analysis.