Inman News

Margins are down, deals are tougher, but experienced flippers aren’t backing off

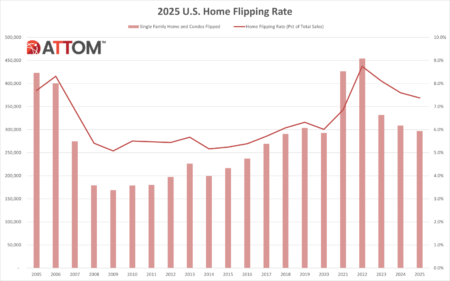

Home flipping lost momentum in 2025, as investors were squeezed by a high-cost, high-interest environment that drove profits to their lowest levels in nearly two decades.

Nationwide, 297,045 single-family homes and condos were flipped last year, a nearly 4 percent drop from 2024 and the lowest annual total since 2020, according to new data from ATTOM.

Even as median home prices peaked, returns moved in the opposite direction. The typical investor’s gross profit — measured as the spread between purchase and resale prices — fell to $65,981, down sharply from $77,000 a year earlier, underscoring the growing margin pressure facing flippers.

That translates to a 25.5 percent return on investment (ROI), the lowest level since 2008, when the U.S. housing market was unraveling during the Global Financial Crisis.

The easy money era is over

In the decade that followed the Great Recession, home flipping surged in popularity. Investors could often acquire properties for under $150,000 and resell them for $225,000 or more, riding a wave of recovering home values and relatively cheap financing.

Today’s market looks very different. In the wake of the pandemic-era housing boom, both home prices and borrowing costs have climbed sharply, compressing margins and making the math far less forgiving for flippers.

Another shift has been on the demand side, where buyer preferences have evolved in response to higher borrowing costs. Research from Realtor.com shows that house hunters are less drawn to flipped homes today than they were in 2021, when mortgage rates hovered near record lows.

Flipping falls in most metros, but not all

The pullback was widespread. Home flipping rates declined year over year in 142 of the 215 metros analyzed by ATTOM — each with populations above 200,000 and at least 100 flips recorded in 2025.

Some markets saw especially steep drops. Salisbury, Maryland, led the downturn, with its flipping rate plunging by more than 42 percent from 2024 levels. It was followed by Tallahassee, Florida (-37.5 percent); Lafayette, Indiana (-36 percent); Evansville, Indiana (-32.9 percent); and Warner Robins, Georgia (-32.6 percent).

Still, the trend wasn’t universal. Roughly one-third of metros posted gains in flipping activity, led by Binghamton, New York (up 126.4 percent year over year), Boulder, Colorado (up 72.4 percent), Greeley, Colorado (up 49.4 percent), Lexington, Kentucky (up 40.3 percent), and Scranton, Pennsylvania (up 31.2 percent).

The Midwest and South become flipping strongholds

Returns on investment declined year over year in roughly 70 percent of the metros analyzed by ATTOM, underscoring just how widespread the margin compression has become.

A cluster of more affordable markets — primarily across the South and Midwest — managed to buck the trend, delivering some of the strongest gains in profit margins.

Peoria, Illinois, led the way, with the typical flip’s profit margin jumping from 61.2 percent in 2024 to 91.4 percent in 2025. The gains were fueled in part by the city’s low cost basis: median listing prices hovered around $159,900 in late 2025, less than half the national median.

Located about 160 miles from Chicago, Illinois, and home to Caterpillar Inc., Peoria offered investors room to generate outsized returns even as national margins tightened.

Huntington, West Virginia, also stood out, with profit margins surging from 50.6 percent to 77 percent in a single year. In Lake Charles, Louisiana, ROI climbed from an already high 121.3 percent to 146.2 percent, marking the third-largest increase among the metros studied.

Cedar Rapids, Iowa, saw median profit margins rise from 29.7 percent to 49.6 percent, while Tuscaloosa, Alabama, rounded out the top performers, with ROI increasing by more than 17 percentage points to reach 26.4 percent.

The frenzy fades, but the business endures

During the pandemic housing boom, rapid home price appreciation acted like rocket fuel for fix-and-flip activity. That momentum came to a halt in 2022, when a sharp rise in mortgage rates reset the economics of the business. Margins tightened, homes sat on the market longer, and many newer investors were pushed out.

The first LendingOne-ResiClub Fix-and-Flip Survey in Q1 2025 captured a market in the midst of that reset. LendingOne-ResiClub says its latest survey suggests a recalibration has largely taken hold. Activity has stabilized, and experienced operators are still planning to deploy capital in 2026, even as national price growth remains muted.

The LendingOne–ResiClub Fix-and-Flip Survey for Q1 2026 includes survey responses from 201 active home flippers and was conducted between February 9 and March 5.

The survey found that demand expectations are holding steady across many regions, and while margins have cooled from their pandemic-era highs, they remain viable for disciplined, experienced operators.

Just over half of U.S. home flippers (53 percent) describe their local market as somewhat or very strong, a figure that has remained relatively consistent over the past year.

Expectations for the year ahead are even more resilient, with 75 percent anticipating strong demand over the next 12 months. Ninety percent of respondents say they are likely to complete at least one fix-and-flip project in the coming year, including 75 percent who say they are “very likely.” Strategies are evolving: 52 percent plan to convert between one and five projects into rentals using a fix-to-rent approach, while 38 percent have no plans to do so.

Rates matter, but speed wins in competitive markets

Regionally, the Midwest stands out as the most optimistic market, with 83 percent of flippers reporting strong buyer demand.

Looking ahead, most respondents — 58 percent — expect market conditions to remain largely unchanged over the next year, while 29 percent anticipate improvement and just 13 percent expect further weakening.

Optimism is strongest in the Midwest and West, while the Northeast shows the highest share of respondents expecting softer conditions.

On the financial side, most investors are maintaining a steady approach. About 61 percent report that their use of leverage is unchanged from a year ago, while 21 percent say they are using less and 18 percent are using more.

When it comes to financing decisions, interest rates remain the top priority overall (31 percent), followed by speed to close (24 percent). That calculus shifts in the West, where nearly half of flippers (47 percent) say speed is the most critical factor, underscoring the competitive nature of those markets.

Operational challenges continue to center on execution and timing. The sale phase is the biggest source of delays, cited by 30 percent of respondents, followed by rehabbing and construction (24 percent) and acquisition (23 percent).

Not surprisingly, lower holding costs top the list of factors that would improve returns, cited by 56 percent of flippers, well ahead of better contractors (32 percent), faster capital draws (9 percent), and more reliable inspections (3 percent).