Inman News

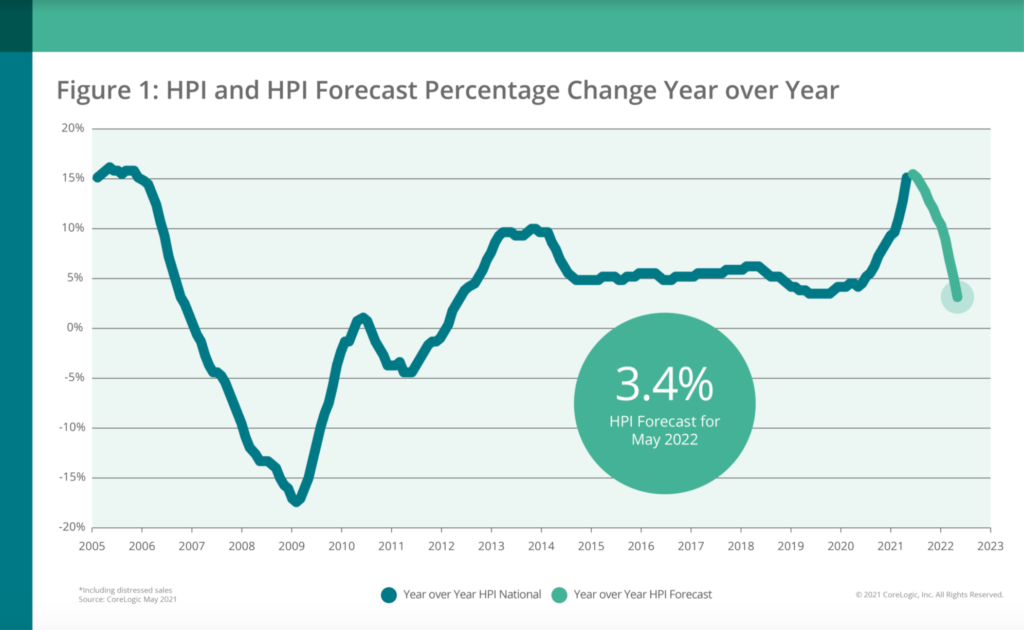

The last time home prices increased by so much was in May 2005, according to the latest CoreLogic Home Price Index report released on Tuesday.

In just one year, home prices across the country rose by 15.4 percent in May — the fourth straight month of double-digit growth and an extraordinarily high number unseen since November 2005.

Home prices also rose 2.3 percent from April to May, according to the latest CoreLogic Home Price Index report released on Tuesday.

While great for homeowners, such high growth is also stalling the market since many potential sellers are holding off on placing their homes on the market. Low mortgage rates, lack of inventory and steep competition from bidders is keeping many first-time buyers on the sidelines. Eighty-two percent of current homebuyers surveyed by CoreLogic view affordability as a major concern while 33 percent said that they would choose to hold off or not buy at all rather than sacrifice what they had wanted.

CoreLogic

“First-time buyers are hitting a wall in many places around the country as the pace of home price rises outpace the benefits of lower borrowing costs,” Frank Martell, president and CEO of CoreLogic, said in a statement. “Younger and first-time buyers, including younger millennials, are faced with the challenge of having sufficient savings for a down payment, closing costs and cash reserves. As we look to the balance of 2021, we expect price rises to continue which could very well push prospective buyers out of the market in many areas and slow home price growth over the next year.”

The property analytics provider predicts that growth will curb significantly in 2021. While still on the increase, homes prices are projected to grow by just 3.4 percent by May 2022.

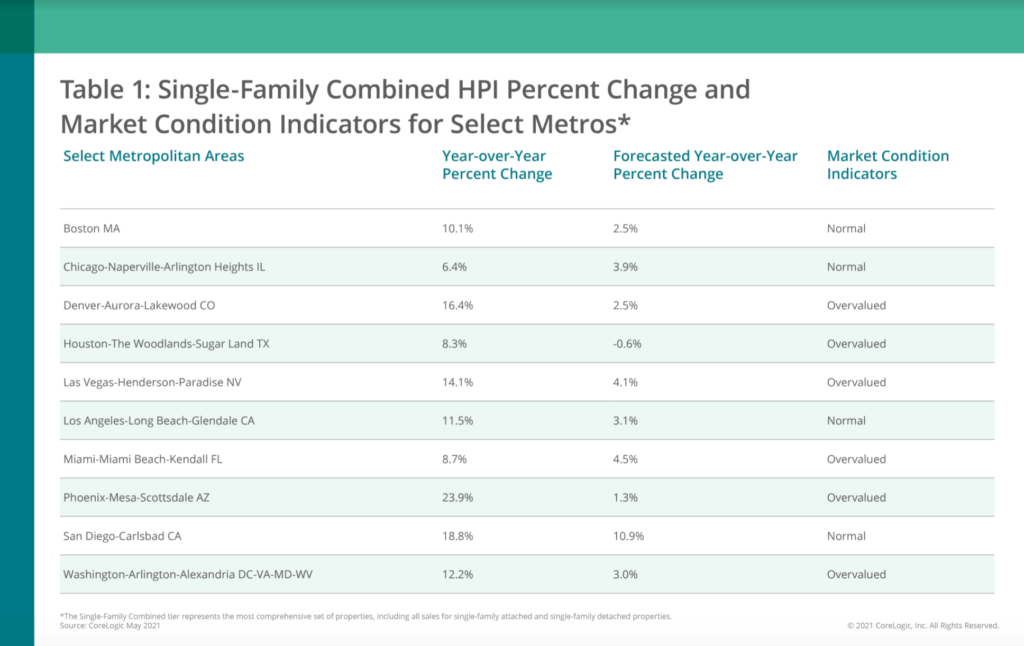

Somewhat unexpectedly, two towns in Idaho saw the highest home growth in the entire country. Both popular vacation destinations, Twin Falls saw 35 percent annual growth while Coeur d’Alene saw 32 percent annual growth. When looking by state, Idaho, Arizona and Utah saw the highest growth at 30.3, 23.4 and 20.4 percent. Several communities in Massachusetts and California, meanwhile, are oversaturated and at high risk of seeing a decline in prices in the coming year.

CoreLogic

“There are marked differences in today’s run up in prices compared to 2005, which was a bubble fueled by risky loans and lenient underwriting,” Dr. Frank Nothaft, chief economist at CoreLogic, said in a statement. “Today, loans with high-risk features are absent and mortgage underwriting is prudent. However, demand and supply imbalances — fueled by a drop in mortgage rates to less than one-half what they were in 2005 and a scarcity of for-sale homes — has fed the latest run up in sales prices.”