Inman News

For the first time, Fannie Mae is forecasting all the way out to 2023, when it expects the economy to enter ‘mature state of the business cycle,’ with the risk of another recession moving into focus.

Inflation is heating up and could accelerate further, but the impact on mortgage rates is likely to be modest thanks to the Federal Reserve laying out a clear roadmap of its plans to withdraw its support for mortgage markets in the months ahead.

That’s according to the latest economic and housing forecast from economists at mortgage giant Fannie Mae, who nevertheless see home sales declining over the next two years and mortgage refinancings plummeting as interest rates rise.

It’s the first time Fannie Mae has provided a forecast all the way out to 2023, when they expect the economy to have entered the “mature state of the business cycle,” with the risk of another recession moving into focus.

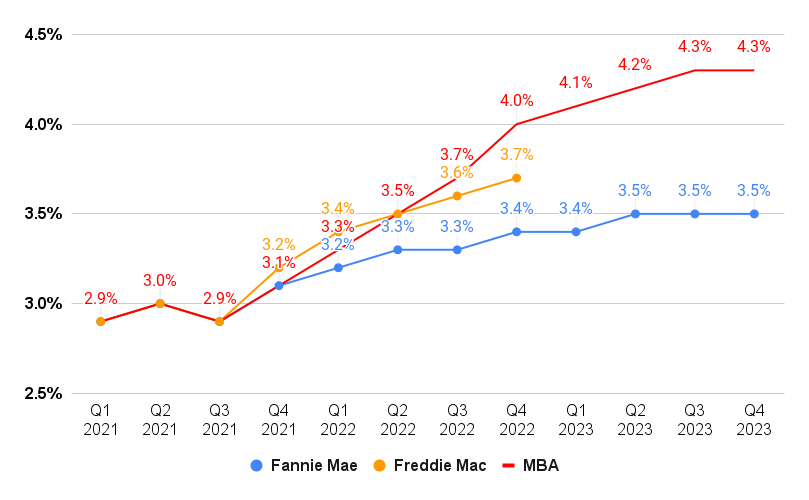

Gradual rise in mortgage rates forecast

Fannie Mae economists are forecasting that rates on 30-year mortgages will rise only modestly over the next two years, hitting 3.4 percent by the end of 2022 and then leveling off at 3.5 percent during the last nine months of 2023.

Even though the Fed has begun tapering its $120 billion in monthly purchases of Treasurys and mortgage-backed securities that have helped keep rates near historic lows during the pandemic, it’s given investors plenty of warning.

“The Fed has taken pains to broadcast its tapering and rate hiking plans to avoid a repeat of the 2013 temper tantrum, when market expectations suddenly shifted regarding the long-run real rate, and for now both financial market and survey measures of long-term inflationary expectations remain mostly anchored,” Fannie Mae forecasters said. “Therefore, our baseline forecast is that these effects are largely ‘baked in,’ leading to only a modest drift upward in mortgage rates over the next few years.”

If it starts to look like inflation is more than transitory, then mortgage rates could move “decidedly higher,” the report said. That’s the view of economists at the Mortgage Bankers Association, who anticipate rates on 30-year mortgages will rise to 4.3 percent by the second half of 2023. Economists at Freddie Mac and the National Association of Realtors are in the middle, forecasting that mortgage rates will average 3.7 percent during the fourth quarter of 2022.

By gradually reducing its asset purchases — by $10 billion a month for Treasury securities, and $5 billion for mortgage-backed securities — the Fed is on track to finish tapering by June. At that point, it’s likely to start raising the short-term federal funds rate if inflation is still running hot.

Doug Duncan

The Fed left “some room for policy change by committing to the speed of tapering assets for only two months, where adjustments could be made thereafter,” said Fannie Mae Chief Economist Doug Duncan, in a statement. Investors who buy mortgage bonds “will have one eye on the monthly inflation releases and the other eye on the Fed in the months ahead. How credible investors, business leaders, and consumers find the Federal Reserve’s evolving beliefs regarding the passing or sustained level of inflation and resulting monetary policy actions will be key – their choices will impact economic growth as well as housing and mortgage activity.”

Fannie Mae forecasters noted that inflation in October, as measured by the consumer price index, came in hotter than expected: 0.9 percent month over month, and 6.2 percent on an annual basis.

“However, it was the underlying details that are more worrying,” the forecast said. “Unlike the similarly sized surges last spring that could be attributed mostly to auto industry issues and reopening sectors, this report showed broad-based price growth.”

It takes about 15 months for rising home prices and rents to show up in the consumer price index. Continued strength in home price appreciation and rents could add a full percentage point to the consumer price index next year. Fannie Mae economists say they would not be surprised to see the index exceed 7 or 8 percent by the end of March, 2022.

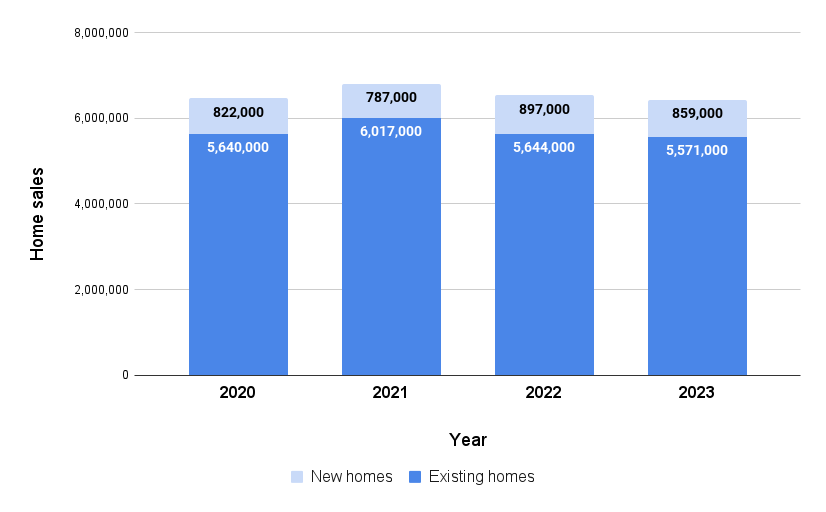

Two years of declining home sale projected

Source: Fannie Mae Economic and Housing Forecast, November 2021.

Fannie Mae forecasters continue to see home sales being constrained by a shortage of listings, strong home price gains, and modestly higher mortgage rates. They envision sales of existing homes dropping for the next two years — by 6.2 percent in 2022, to 5.64 million homes, and by another 1.3 percent in 2023, to 5.57 million homes.

Not only do listings remain scarce in many markets, but “much of the strength in home purchases over this past year and a half stemmed from first-time buyers moving forward their purchases due to COVID-related disruptions, as well as to take advantage of historically low mortgage rates,” the forecast noted. It’s likely that this component of demand from first-time homebuyers, “will have to be given back.”

Higher home prices and listings shortages are good for builders, however, and despite ongoing supply chain disruptions and labor shortages,

Fannie Mae forecasters see new home sales growing by 14 percent next year, to 897,000.

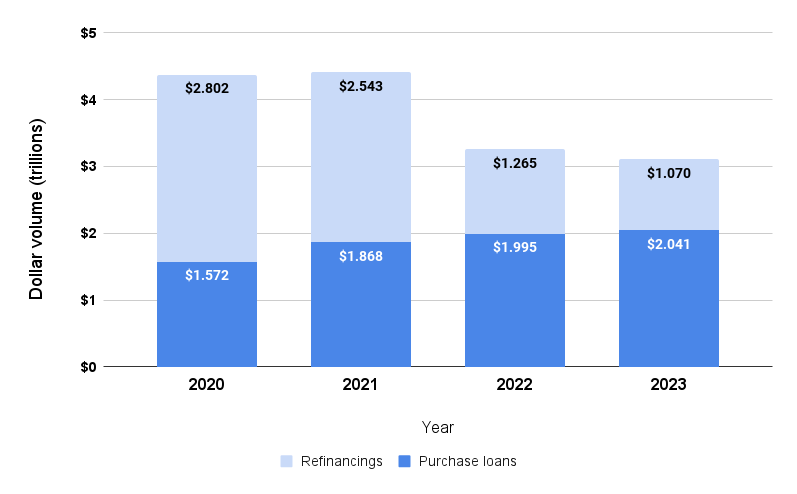

Mortgage refinancings expected to drop by 50 percent

Source: Fannie Mae Economic and Housing Forecast, November 2021.

Higher home prices also explain why Fannie Mae economists expect mortgage lenders to boost the total dollar volume of purchase loans funded, even if they do make fewer loans.

The expected 7 percent increase in purchase loans next year, to roughly $2 trillion, would only take some of the sting out of a projected 50 percent drop in refinancings, to $1.265 trillion in 2022.

At the current mortgage rate of 2.98 percent, Fannie Mae economists estimate that about 43 percent of outstanding mortgages have at least a 50-basis point incentive to refinance. But many will lose that incentive if rates rise, as expected.

Looking ahead to 2023

Fannie Mae’s first forecast for 2023 envisions an economy that is likely to have entered “the mature stage of the business cycle” — with the next recession perhaps looming around the corner.

A mature stage means growth “has recovered back to trend, the labor market is at ‘full employment,’ and the Federal Reserve is in the process of tightening monetary policy,” Fannie Mae’s forecast said. “At that point in the business cycle recession risk moves into focus, as there is no longer pent-up demand or excess production slack providing momentum. The economy is therefore more vulnerable to be knocked off its growth trend by any ensuing shocks. Additionally, imbalances or inefficiencies become more exposed in an environment of slower growth and tightening monetary policy.”

If it seems “odd to be discussing the next potential recession so shortly after the 2020 downturn,” Fannie Mae economists point out there were four recessions between 1948 and 1960, and four downturns between 1970 and 1983.

Typically, once the Fed starts hiking rates, “the next downturn occurs between one and three years later,” the forecast notes. “Uncertainties over the future path of labor productivity and immigration flows will affect how long the cycle can potentially persist, but the current expansion is not likely to be as long-lasting as the previous one, which was the longest in the post-World War II era.”

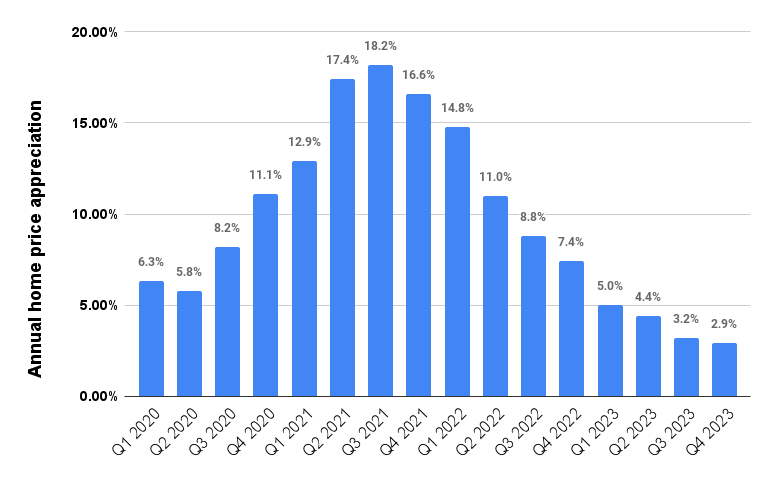

Home price appreciation expected to cool

Source: Fannie Mae Economic and Housing Forecast, November 2021.

Fannie Mae economists see home price appreciation cooling off somewhat next year, with the annual rate of appreciation dropping back into the single digits in the second half of 2022. The forecast calls for even more chilling in 2023, with home price appreciation dropping below the current rate of inflation.