CityLab

7 May 2018

The rise of renting in the U.S. isn’t just about high housing prices, or preferences for city living, but about the flexibility to compete in today’s economy.

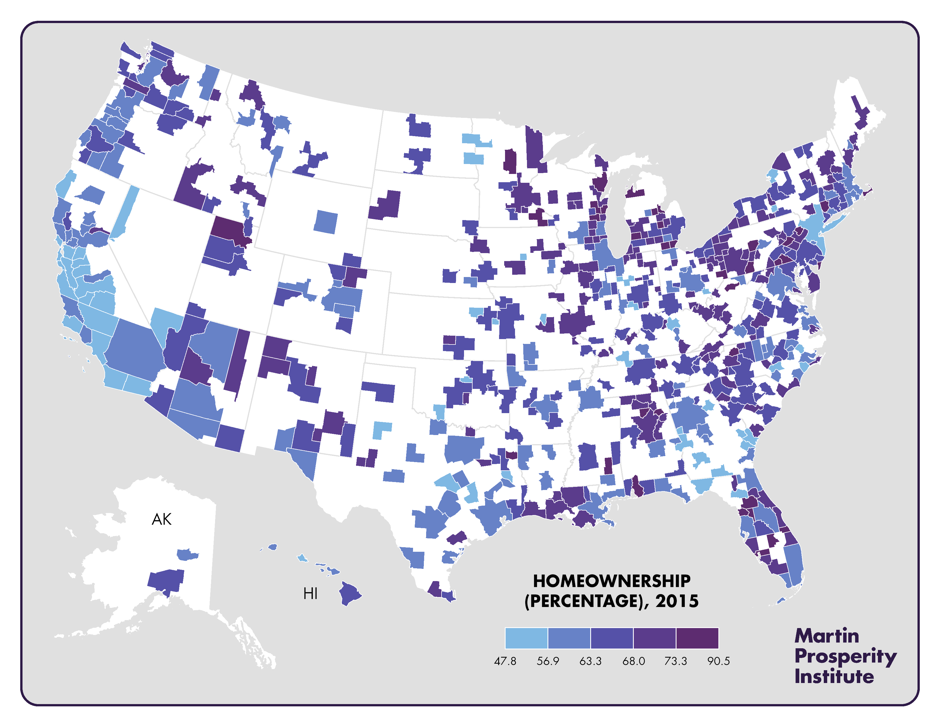

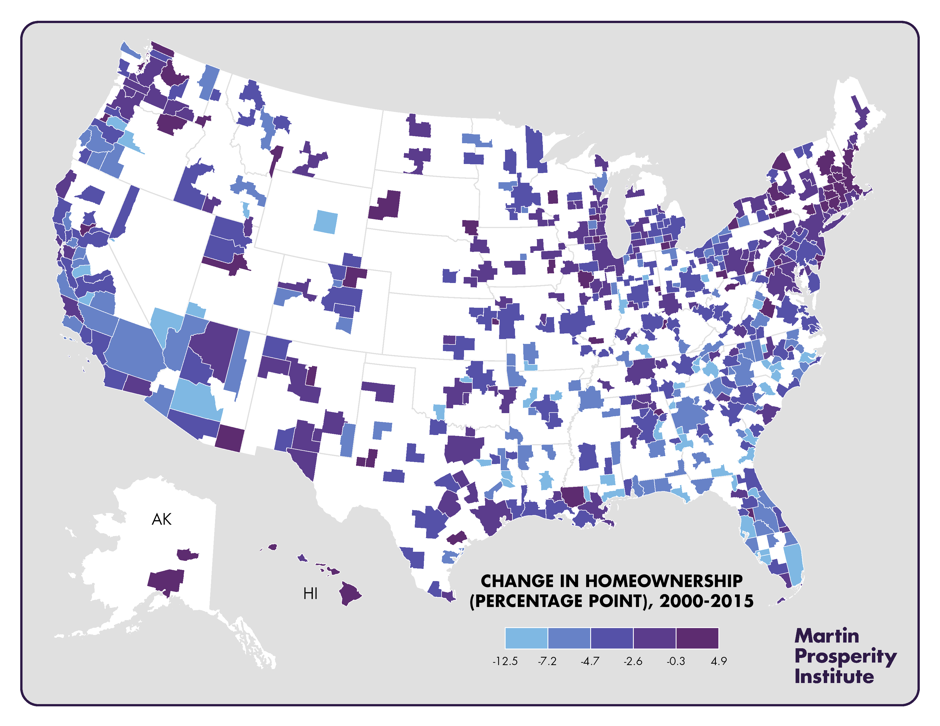

But the shift from owning to renting a home is much more dramatic in certain cities, and the most innovative and dynamic metropolitan areas consistently post the lowest homeownership rates. My Martin Prosperity Institute colleague, Karen King, and I used Census data to dig into the extent of this great housing reset across American metros from 2000 to 2015—a period that includes the economic crisis of 2008 and the subsequent recovery.

The homeownership rate is lower in America’s more dynamic, more innovative, and more knowledge-based metros. This a product of the fact that these metros are more expensive, but it also speaks to their urban form. Having a larger stock of rental (usually multifamily) housing helps provide the flexibility required to absorb the young people and mobile talent that fuel their economies.

Nearly three-quarters (72.4 percent) of larger ZIP codes (those with at least 1,000 occupied housing units) across the nation saw their homeownership rate decline between 2000 and 2016, according to a Trulia analysis. Homeownership has declined by more than 30 percent in some of these ZIP codes, which include North San Jose, Riverview in St. Louis, and Maryvale in Phoenix. One thing these disparate places have in common: an influx of multifamily rental units. Indeed, a major aspect of the great housing reset is the gradual shift away from single-family-home construction and an increase in multifamily development.

The neighborhoods where homeownership has increased substantially tend to be rapidly gentrifying areas. These have experienced an influx of wealthy owners who have displaced less advantaged renters. An example is the neighborhood surrounding Georgia Tech (the Georgia Institute of Technology) in Atlanta, where homeownership increased from 13 percent to 32.5 percent as median incomes tripled.

The great housing reset varies across class, race, and demographic lines as well as geographic lines, according to the Urban Institute. The homeownership rate among younger Americans between the ages of 25 and 34 declined from a high of almost 50 percent in 2005 to just 35 percent in 2015. It plummeted almost as much among those ages 35 to 44, falling from 69 percent to 56 percent.* It fell from 68 percent to 60 percent for high-school graduates and from 57 to 49 percent for those who never completed high school. And although the rate also went down slightly for college graduates over this 10-year period, it actually rose for them over the broader three-decade period of 1985 to 2015, which is not the case for the previous two categories.

Toledo, Memphis, Tampa, Hialeah, Stockton, Honolulu, and Anaheim each saw a 25 percent or more increase in renters over this period. Another dozen or so cities saw their share of renters increase by between 10 and 25 percent, among them Detroit, Cleveland, Columbus, St. Louis, Baltimore, and Minneapolis. Even more striking, the analysis found that 97 percent of the nearly 24 million new residents the U.S. added over that same period are in rental households.

Yet despite widespread declines, homeownership is not becoming obsolete. In fact, the national rate saw a small uptick in 2017 and early 2018, rising to 64.2 percent, alongside a modest decline in rental households. A large proportion of households will continue to choose homeownership, whether in urban condominiums or suburban single-family homes. But the historic ratios between homeowner and renter households will likely continue to shift—in a process that is still in its early stages. And, of course, the balance will continue to vary widely across cities and metro areas.

Great resets are generational events representing an adjustment to a new economy. We are still in the middle of the shift from an industrial system that was powered in large part by suburban homeownership—and the demand for manufactured products it helped create—to a new, highly clustered knowledge-based system in which cities are the basic platform for economic activity. The shift from homeownership to more flexible rental housing reflects the realities of that broader transformation.