CALCULATEDRISK

By Bill McBride

With house prices up mid-single digits over the last year, an interesting question is: How much will the Fannie & Freddie conforming loan limits (CLL) change for 2025? And how much will the FHA insured loan limits change?

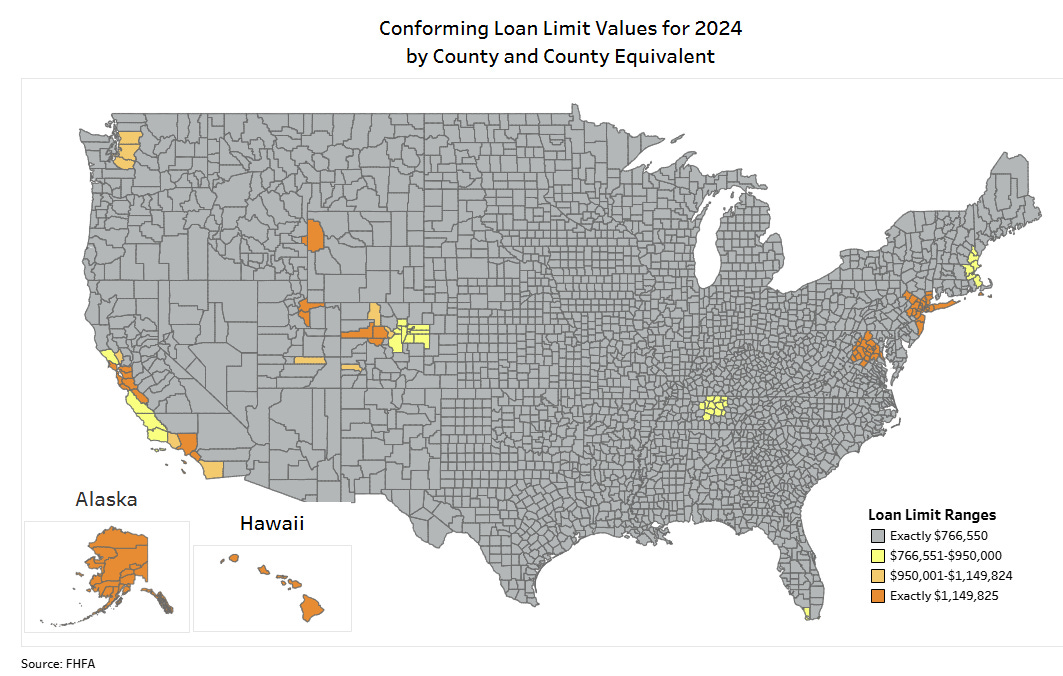

First, there are different loan limits for various geographical areas. There are also different loan limits depending on the number of units (from 1 to 4 units). For example, currently the CLL is $766,550 for one-unit properties in low-cost areas. For high-cost areas like Los Angeles County, the CLL is $1,149,825 for one-unit properties (50% higher than the baseline CLL).

The CLL for each county is available at 2024 Conforming Loan Limits (excel file).

The limit is updated annually, and is adjusted using the FHFA’s quarterly national, seasonally adjusted, expanded-data index: Expanded-Data Indexes (Estimated using Enterprise, FHA, and Real Property County Recorder Data Licensed from DataQuick for sales below the annual loan limit ceiling). The adjustment is based on the House Price Index value in Q3 divided by Q3 in the prior year. The FHFA index is a repeat sales index, similar to Case-Shiller.

Note: This calculation has changed with the Housing and Economic Recovery Act of 2008 (HERA). Also, in 2015, the FHFA decided to use the seasonally adjusted expanded data index.

Currently we only have data for Q1 2024 for the quarterly index (up 6.6% from Q1 2023), and the monthly House Price Index was up 5.7% YoY through May 2024.

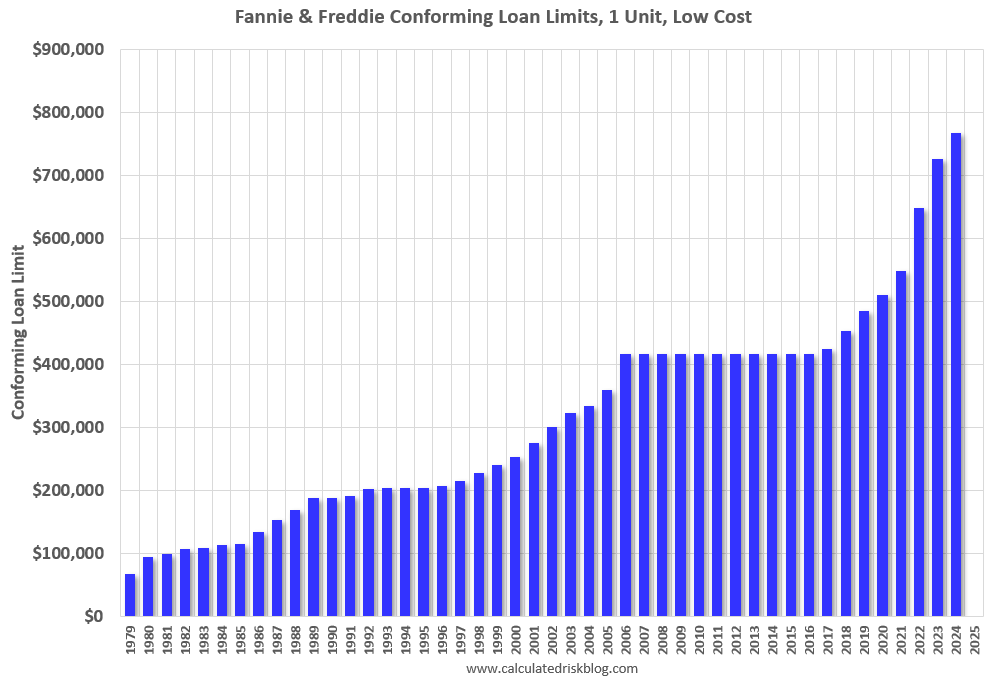

Note that during periods when house prices decline, the CLL is not reduced. The CLL was at $417,000 from 2006 through 2016, and only increased slightly in 2017 as the house price index caught back up to the previous high reached during the housing bubble. This graph shows the CLL since 1979. The CLL was unchanged from 2006 though 2016.

We need the house price data through September 2024 to calculate the conforming loan limit for 2025. This quarterly data will be released in late November.

Based on the current year-over-year house price change (through May), the CLL would be close to $810,000 in 2025.For high-cost areas like Los Angeles, the limit could increase to over $1.2 million. However, the year-over-year (YoY) increase in house prices has been slowing, and it is likely the increase will be less than 5.7%.

What about FHA insured loans? From the FHA:

FHA’s nationwide forward mortgage limit “floor” and “ceiling” for a one-unit property in CY 2024 are $498,257 and $1,149,825, respectively.

The current FHA insured limit (low-cost area) is 65% of $766,550 or $498,257. In high-cost areas, the FHA insured limit could be as high as $1,149,825. The limit varies by geographical area (based on average house prices).

Note that HERA changed this relationship. For low costs areas, prior to HERA, the FHA insured limit (low cost) was 48% of the CLL.

Once again, we need the expanded index house price data for Q3.

Note: In some years, private lenders have announced an increase in the CLL in October prior to the official release in late November. Since house prices increased sharply in 2021 and 2022, these lenders estimated the likely increase in the CLL – minus a comfortable buffer – and started accepting larger loans. These lenders qualified buyers as if they were selling the loans to Fannie and Freddie, except for the loan limit. Then these lenders held any loans made with the “unofficial limit” in their own portfolio until the following January. With a much smaller increase in house prices this year, it is unlikely we will see lenders announce unofficial increases this year.