HousingWire

Deficit financing might be the cure to the housing shortage blues.

The U.S. housing market was the single best outperforming economic sector globally during the COVID-19 pandemic in 2020. The reasons for that are solid demographics and low mortgage rates, which will not change much in 2021. Due to the solid demand for homes, housing market supply for both new and existing homes are at all-time lows.

New Housing Market Supply

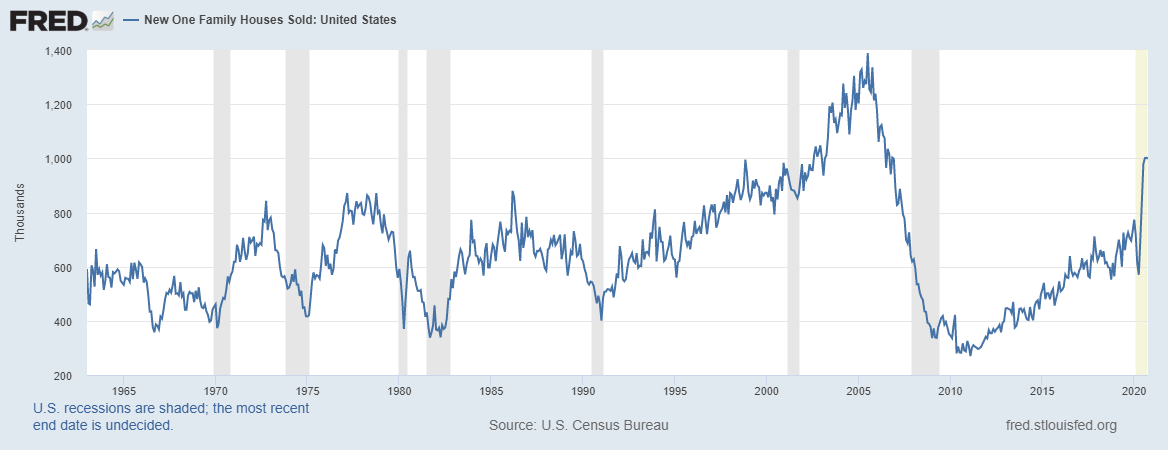

The monthly supply for new homes is currently at 3.3 months. This matters because builders like to see monthly supply below 6.5 months to have the confidence to continue building. If supply goes over 6.5 months, builders will halt the rate of growth for new construction plans as they did in 2018 and again for a brief period this year.

For now, though, the low inventory means housing starts have legs to move higher. Keep this rule of thumb in mind for the future, below 4.3 months; the builders are very excited; from 4.4 -6.4 months, the builders are ok with construction as long as new home sales grow. Above 6.5 months, Houston, we have a problem.

Existing Supply

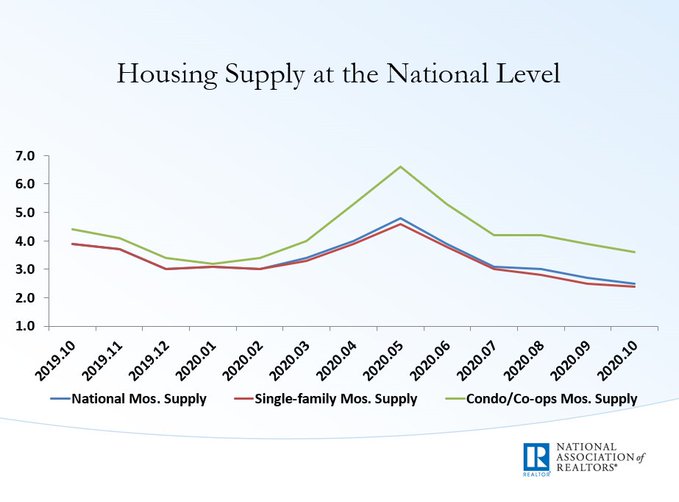

Existing housing market supply is also at all-time lows. We had a temporary increase in housing supply due to the lack of activity from COVID-19, which was quickly ended as housing activity picked up after a few weeks.

Unsold inventory sits at an all-time-low 2.5-month supply at the current sales pace, down from 2.7 months in September and down from the 3.9-month figure recorded in October 2019.

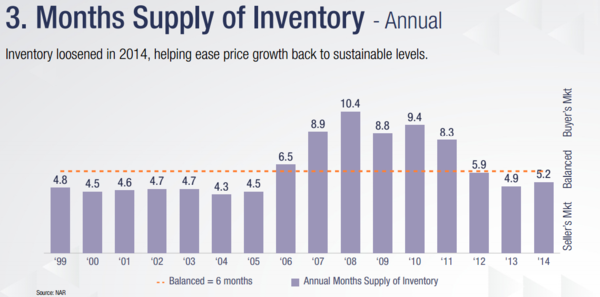

My housing economic mindset really starts from 1996 as mortgage rates are much lower now than in previous decades. The monthly housing market supply for the existing home sales has only gone above six months during the bust years after the housing bubble (2006-2011). We had a lot of forced selling during that time due to bad debt quality for home loans and over 8.7 million jobs lost. This period was also during a lull in our prime-age labor force growth, so demand was soft during the years 2006-2011.

Of course, today is a much different story; our demographics are much better, and mortgage rates are lower. Our homeowners on paper look better than ever.

Demand right now is not an issue for both the existing and new home sales market.

However, higher mortgage rates are a factor that can kill builders’ enthusiasm to build. When rates rise, demand cools, and the builders are mindful of this.

In 2013/2014, when the economic data was improving, mortgage rates rose. As a result of the increase in rates, demand for housing fell in 2014. The new home sales market had an epic miss from sales estimates in 2014. Even though it was barely positive, people had anticipated much higher growth levels because new home sales were meager historically.

For a while in 2014, purchase applications data were trending down 20%, year over year. Existing home sales dipped below 5,000,000, and monthly housing market supply rose. Even so, monthly supply for existing homes never got above six months as it did during the years of the bust from 2006-2011. Similarly, in 2018 and 2019, mortgage rates rose to 4.75 to 5%, causing the monthly supply for existing homes to increase slightly. In turn, price growth cooled so that real home price growth went negative year over year in 2019.

Now mortgage rates are far from 4.5%-5%. Low mortgage rates combined with a sweet spot in the demographics for housing in 2020-2024 suggests we could see real home-price growth in 2021. The only thing that can cool this seemingly inevitable growth in home prices is higher mortgage rates and increased inventory. Considering the tenuous state of the economy, a significant increase in mortgage rates seem unlikely in 2021 and what I mean by significant is above 4.5%.

And we cannot depend on builders to massively overbuild housing starts beyond demand just to cool prices. This would be the antithesis of their business model.

So if we want to increase inventory so more affordable housing is available, what can we do?

1) End forbearance plans immediately so more homes come on the market. This is a terrible idea that would force homeowners most affected by the COVID crisis to help others be homebuyers. Hard pass.

2) Tighten lending standards, so there are fewer buyers that qualify for the existing inventory. This could be accomplished by raising the minimum down payment, removing the mortgage interest deduction and the property tax benefit. This, too, could have the effect of dampening demand, so fewer buyers would be chasing the existing inventory. I am joking when I say this, as I can see the housing industry scream at this idea. Also, housing has been a bright spot during this crisis.

Fortunately, there is a zero percent chance of either of these things happening. In fact I expect forbearance to be continued the entire year of 2021.

My solution for increasing inventory and mostly affordable inventory would be to take it out of private market hands. I propose that the federal government allocate funds via significant deficit financing to any state that wants to build homes right away. We would contract builders to construct housing and directly through any weakness in housing demand or period of higher mortgage rates.

This would create enough housing market supply to cool price growth and help balance the market to include lower-income buyers and renters. It could also function as a jobs program. Even after the last jobs report, we still have 9.8 million Americans out of work due to COVID-19, which is still more than the jobs lost due to the great financial crisis. Since this is on the government tab, the builders won’t care so much about profit margins being met.

For this to work, we would need to prevent NIMBY lawsuits from delaying construction projects. I would put this responsibility on the states. If cases linger, project funding will be removed and given to another state. Since the program will be deficit financed through the federal government, no taxes will need to be raised.

This is a simple plan that will never happen because we want contradictory things. We want homes to be more affordable, but we don’t want to build affordable housing in our neighborhoods. Homeowners want to have the Mortgage Interest Deduction and other tax benefits of being a homeowner. But we want home prices to cool down, right? On the other hand, a hot housing market means those households who spend will have more wealth, that wealth effect all over again.

Also, the government is in love with the idea of forced savings through equity building of a home. Let’s not kid ourselves; keeping home prices up is part of the American way of doing things. Wait, I’m confused. Do we want the inventory to go up, or don’t we? Do we want home prices to go up, or don’t we?

The truth is we talk a lot about building, but it never happens outside of the normal supply and demand balance in the housing market. Once housing demand fades and inventory rises, there will be a pause from the builders, and this conversation of building, building, and building will go away. This is the actual reality of the world we live in.

A push to build more rentals is a bit more realistic. In costly areas where most people are forced to rent rather than buy, vertical building projects are a great idea – but Japanese vertical-style living is not for everybody. And we would need to be careful not to repeat some of the egregious mistakes of the past with building just luxury rental units.

Don’t hold your breath on any massive build-out of housing to increase inventory and control price growth. For the past 10 years, countless housing advocates have professed the need to build more housing. In 2018, when monthly supply spiked to over 6.5 months and builders paused construction, the fear became has housing peaked.

The only way the builders continue this is if demand continues to grow and we no longer have the low bar in new home sales that we enjoyed from 2008-2019. This sector gets impacted by higher and lower rates the most.

Until housing advocates, builders, homeowners and the government all agree on a cohesive philosophy regarding housing in America, prepare to remain confused and conflicted.

Also, has infrastructure week started yet? No, it hasn’t and there is a reason for that.