HousingWire

We can finally see a path to a Fed pivot

By Logan Mohtashami

Today’s double event of the CPI inflation report and the Fed meeting gave us something that I have been waiting for: a hint from Fed Chairman Jay Powell that the labor market has softened. Today he acknowledged what I have been talking about for months: the Fed’s key data lines are at pre-COVID-19 levels today.

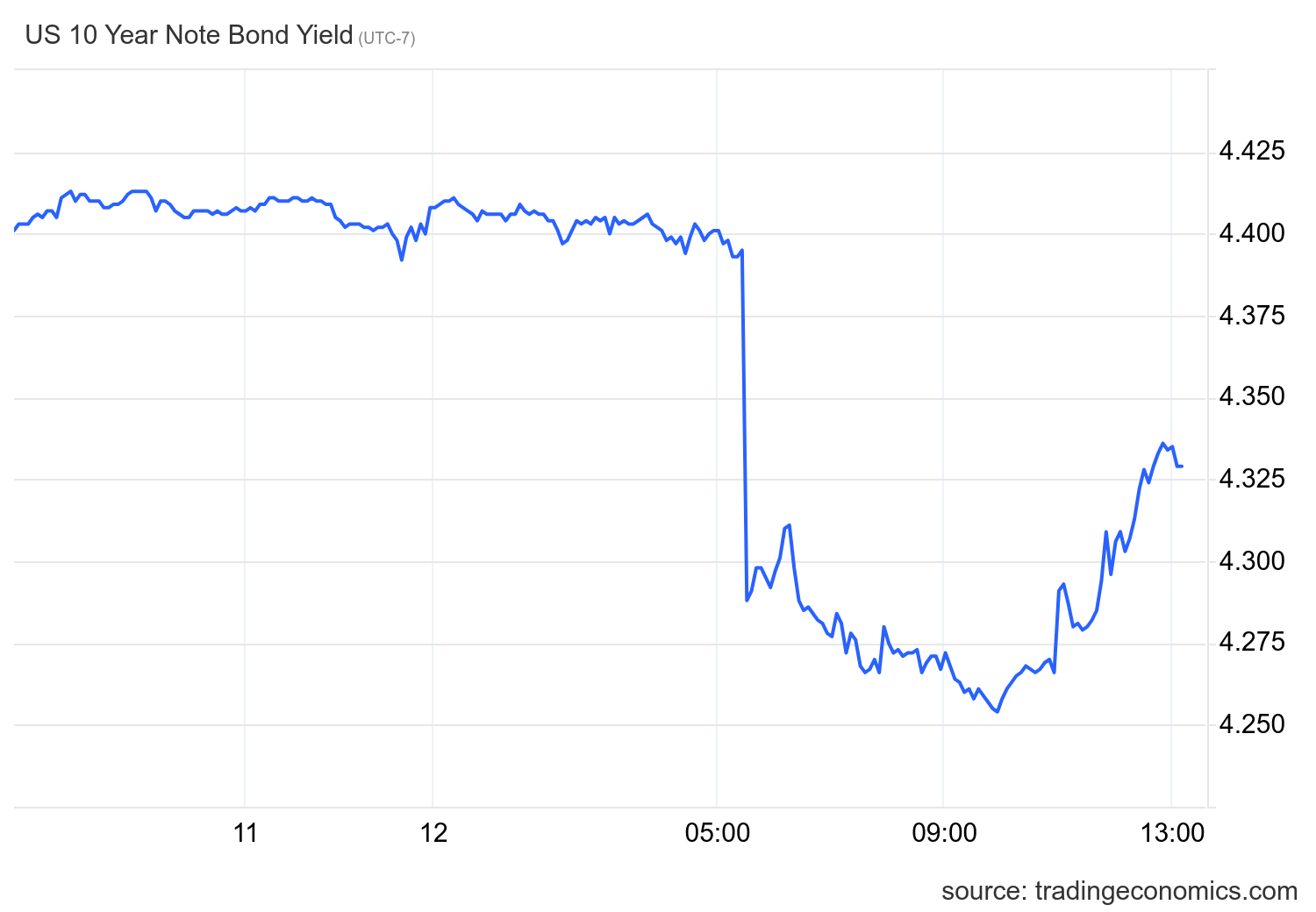

Before the Fed held its press conference, we got a softer-than-anticipated CPI report, which sent the 10-year yield (and mortgage rates) lower at first. Then, the Fed announced its policy and bond yields headed higher as Powell spoke. However, the 10-year yield finished the day lower. We have had some wild moves on key data lines lately, but we have itchy fingers from crowded trades, as shown in the 10-year yield below.

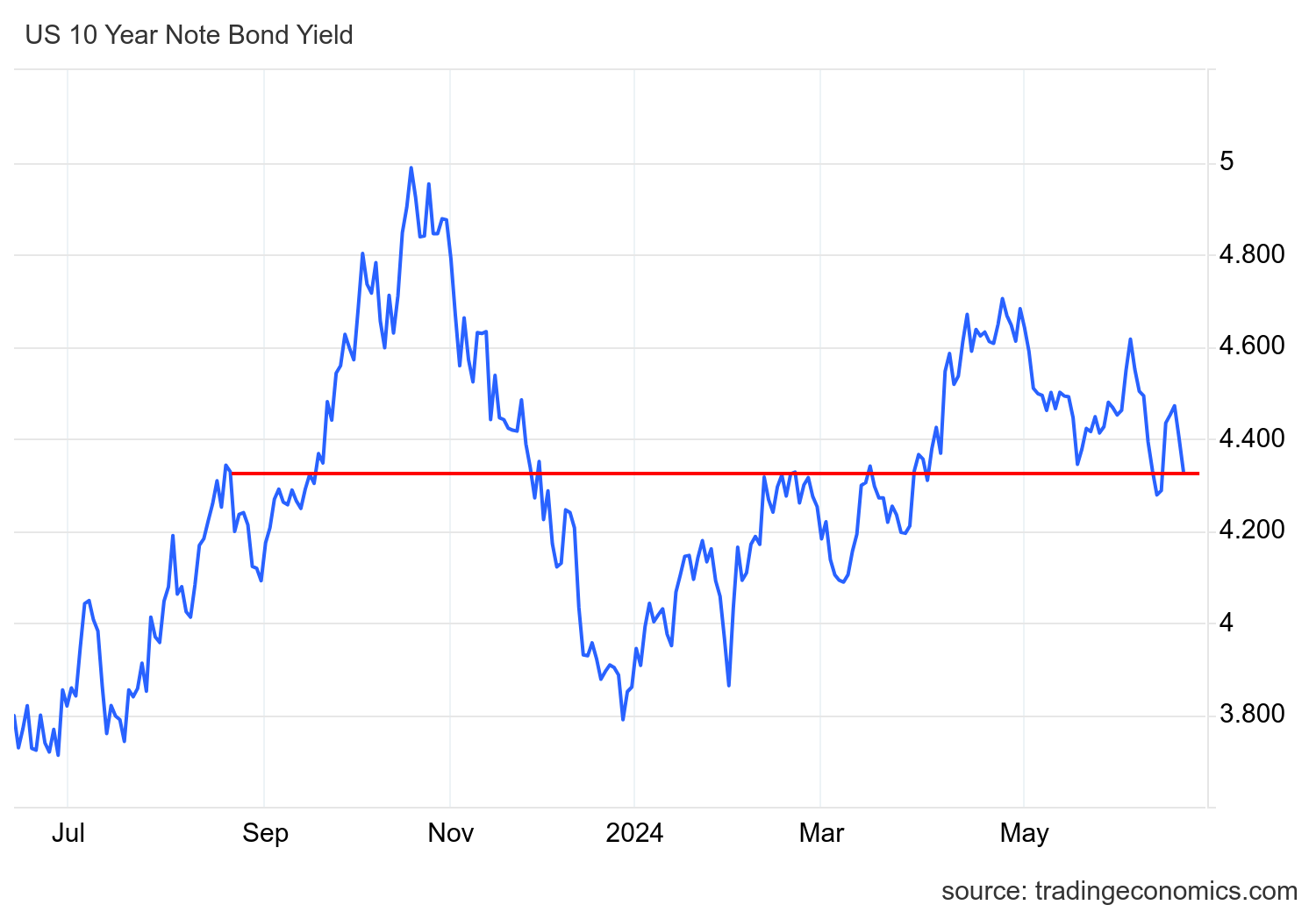

The ten-year yield, vital for mortgage rates, closed at a critical technical level today. However, we must remain vigilant, as we need to see softer economic data or a much softer PPI inflation print tomorrow morning to confirm this trend.

The PPI inflation report is critical because it filters more into the PCE inflation report later in the month, and that is the Fed’s preferred inflation data to track. As you can see below, we are again at this crucial level for the 10-year yield, so we shall see if this breaks lower.

Let’s first look at today’s inflation report because the CPI inflation report was a big surprise today.

From BLS: The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in May on a seasonally adjusted basis after rising 0.3 percent in April, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 3.3 percent before seasonal adjustment.

The month-to-month inflation data shocked bond traders, hence the big waterfall dive with the 10-year yield right after the report. It wasn’t like rent inflation drove this lower either — the shelter inflation grew monthly, but other inflation data came in lower than anticipated. As you can see in the chart below, we have made some good progress on the year-over-year inflation data heading lower.

However, going out for the second half of the year, the base effects of the CPI data means it will be harder for these year-over-year gains to show progress. This is one thing Jay Powell discussed, which is a huge deal. This means the Fed will be more focused on the month-to-month data reports, as they should be, going out for the rest of the year.

The big takeaway from the Fed meeting is that although they talked about the inflation data being good, the key talking point wasn’t about inflation at all — it was about the labor market.

The Fed believes the labor market data is back to balance enough to publicly say we are at levels we had before COVID-19. This is very big, as I feared Powell would wait for the job openings data to get back toward 7 million or the wage growth data to get back to 3% before he said this. The fact that he made this public is enormous.

So, what do we make of today’s double event? The inflation data was cooler than expected, but that won’t move the needle for Fed rate cuts. However, Powell’s labor talking points are a big deal.

The fact that the Fed is open to talking about labor supply data being balanced means they know that the labor market is softening. If we see labor data breaking, they will find the cover needed to cut rates without worrying so much about inflation because they will be back to a dual mandate Fed. On the mortgage rate side, this means mortgage rates can go lower and stay lower when the labor data gets weaker.

I see this as a sea change because one concern I had was the Fed would wait too long before admitting that the labor market is back to pre-COVID-19 trend data. It has been at that level for months now, so better late than never! As Powell said today: the best thing we can do for housing is get inflation lower so we can cut rates. My argument has been that the labor data will dictate this and today, we can finally see the path to a Fed pivot, but it does require the labor market getting weaker.

Logan Mohtashami is a renowned expert in the mortgage and housing ecosystem, recognized for his insightful analysis and commentary on the U.S. economy and real estate market. Mohtashami is a lead analyst for HousingWire and is a regular contributor on the HousingWire Daily podcast. With a background spanning over two decades in the mortgage industry, Mohtashami — nicknamed “The Chart Guy” — has the remarkable ability to decipher complex economic data and translate it into understandable, actionable insights. This knowledge has made Mohtashami a sought-after commentator and his expertise has been featured extensively in news outlets, including CNBC, where he is a frequent guest.