Inman News

Luxury home sales fell 44.6% year over year, according to data released Friday by Redfin. Prices are nevertheless still high because inventory is so low, economists say

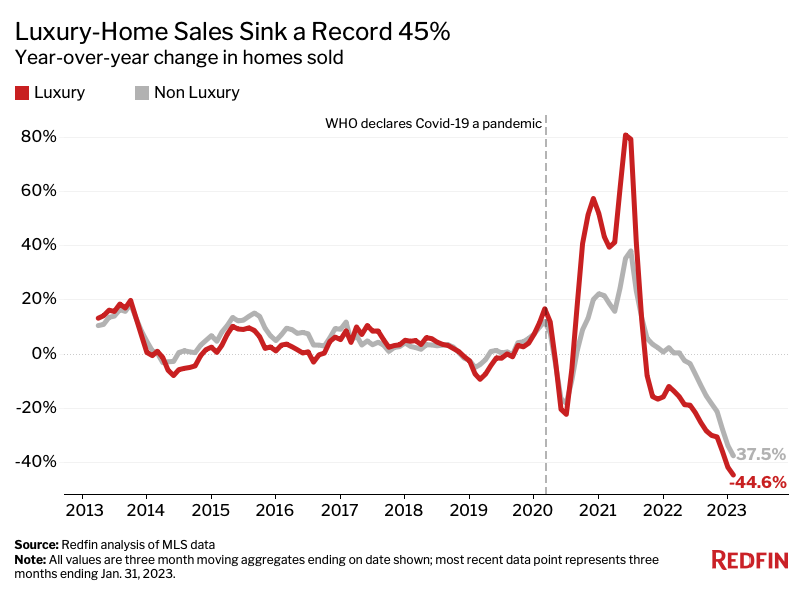

In a sign of the now-troubled times facing the real estate market, Redfin on Friday reported that luxury home purchases experienced a record-breaking drop at the end of 2022 and beginning of this year.

Redfin’s report specifically shows that in November, December and January, U.S. luxury home purchases were down 44.6 percent compared to the same period a year earlier. That was the biggest drop Redfin has ever recorded. The company’s records go back to 2012, and the previous record was a year-over-year dip of 37.5 percent.

In its report, Redfin noted that “the housing market has cooled significantly over the last year due to elevated mortgage rates, persistently high home prices, ongoing inflation and a shaky economy.” And as a result, many wealthy Americans — who make up the market for luxury homes — are turning to investments other than real estate.

Redfin defines luxury homes as those in the top 5 percent based on market value.

Despite the record drop in sales, Redfin’s report also notes that prices for high-end houses are “near their peak” and actually rose 9 percent year over year during the three month period that ended on Jan. 31.

The reason prices have been able to remain high even as sales have dropped off is because inventory is tight. The report notes that the number of luxury homes for sale rose 7.1 percent in November, December and January, but that such a rise happened against the backdrop of an extreme shortage.

“The sizable year-over-year increase is largely due to the fact that supply hit rock bottom roughly a year earlier; supply is also piling up because so few people are buying homes,” the report notes.

Credit: Redfin

The report goes on to note that fewer people are putting their homes up for sale thanks to higher mortgage rates, and that supply consequently “remains near historic lows.”

Moreover, the supply of new luxury listings actually fell 6.6 percent year over year in November, December and January. The fact that overall listings increased even though fewer homes came on the market means properties are sitting unsold for longer.

Broken down by metro area, the places that saw the biggest dips in luxury sales were Miami, New York state’s Nassau and Suffolk counties, and Riverside, Anaheim and San Jose, all in California.

The metro areas with the smallest declines in luxury sales were Kansas City, Missouri, Cleveland, Ohio, and Pittsburgh, Pennsylvania.

Of the metro areas included in the report, San Francisco had the highest median sales price for luxury properties, at $4.7 million. Cleveland had the lowest, at $663,400.

In the report, Los Angeles area Redfin agent Alin Glogovicean noted that another key factor driving luxury housing dynamics right now is uncertainty.

“If you’re investing millions in a property, you want to make sure it will hold its value,” Glogovicean said. “Most luxury buyers and sellers are thinking, ‘Let’s just wait and see what happens to the market. When it stabilizes, we’ll be ready to go.’ Everyone is kind of at a standstill.”