CALCULATEDRISK

By Bill McBride

Intercontinental Exchange, Inc. today released its March 2026 ICE Mortgage Monitor Report. According to the analysis, total mortgage originations reached an estimated 1.44 million in the fourth quarter — the largest quarterly tally since Q3 2022 — as a surge in refinance activity drove lending to its highest level in three and a half years and servicer retention climbed to an eight-year high.

“The fourth quarter marked a meaningful inflection point for mortgage market activity,” said Andy Walden, Head of Mortgage and Housing Market Research at ICE. “Refinances accounted for nearly 40% of Q4 lending and servicers retained one in three refinancing borrowers, the strongest overall retention rate since early 2014. Underpinning it all, February’s dip in mortgage rates expanded the refinance-eligible population to 5.4 million borrowers, the largest pool we’ve seen since early 2022, further improving affordability, which is at its best level in nearly four years.”

Key findings from the March Mortgage Monitor include:

- Refinance incentives surged while affordability held at multi-year highs

The number of borrowers considered refinance-eligible by at least 75 basis points jumped to 5.4 million, the highest level since early 2022. An estimated 565,000 first-lien refinances closed in the fourth quarter, up roughly 50% from a year earlier and representing the highest quarterly volume since Q2 2022. Affordability continued to improve on its near four-year high, with the monthly payment needed to purchase the average-priced home declining 8% from a year ago to $2,063.

- Q4 lending reached 3.5-year high, driven by refinance activity

Total mortgage originations reached an estimated 1.44 million in the fourth quarter, the largest quarterly tally since Q3 2022. Refinances accounted for nearly 40% of fourth-quarter lending, the highest quarterly share since early 2022. Activity was concentrated among recently originated loans, with the average rate-and-term refinancer carrying a $510,000 balance and reducing their monthly payment by $248.

- Equity extraction remained strong, led by largest second lien volume in 18 years

Homeowners withdrew $52 billion in equity during the fourth quarter, bringing full-year 2025 equity withdrawals to $205 billion — the highest annual total since 2022. Of that figure, $116 billion was extracted through second liens, marking the largest annual second-lien volume since 2007. Homeowners continue to hold nearly $17 trillion in total equity, with approximately $11 trillion considered tappable.

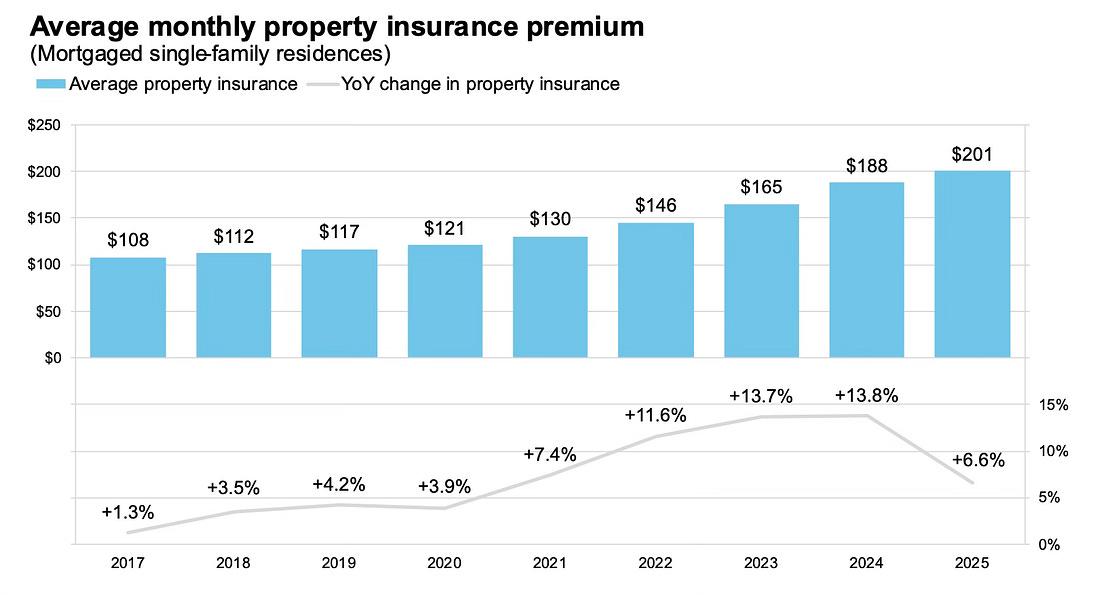

- Property insurance costs hit another record high, though rate of growth slowed

Average annual property insurance payments rose 6.6% ($149) in 2025 to an all-time high, but at the slowest pace since 2020. The fourth quarter also marked the first quarter-over-quarter decline in insurance costs since ICE began tracking monthly data in late 2023. ICE Climate research found that borrowers in the highest insurance-burden quintile were at least 22% more likely to be non-current than those in the lowest quintile of credit score tiers analyzed. For every percentage-point increase in housing expenses allocated to insurance, the non-current rate rose by roughly 0.14 percentage points, on average across credit score quintiles. …

emphasis added

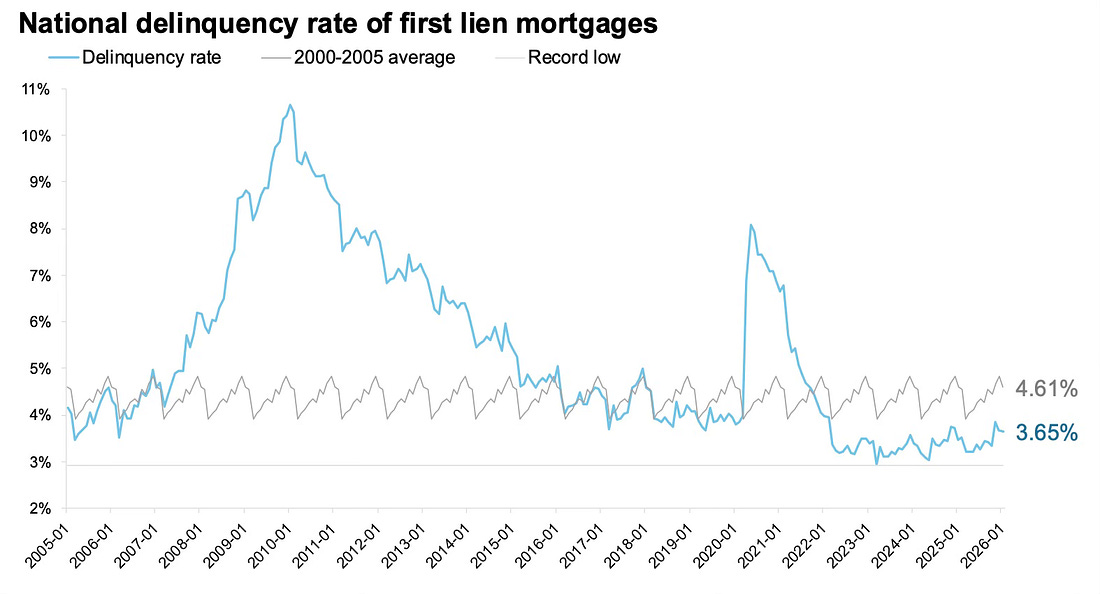

Mortgage Delinquencies “Dipped” in January

Here is a graph of the national delinquency rate from ICE. Overall delinquencies decreased in January and remain below the pre-pandemic levels. Source: ICE McDash

- The national delinquency rate dipped 3 basis points in January to 3.65% and is now 15 basis points below the pre-pandemic January 2020 benchmark

- Early-stage delinquencies improved, with 54,000 fewer borrowers 30 or 60 days late compared to December

- Later-stage stress increased as 90-plus-day delinquencies rose 35,000 and active foreclosures rose 16,000 in January, continuing their upward trend

- More than 850,000 borrowers are now 90-plus days past due or in active foreclosure — up 104,000 year over year, the highest level since mid-2018 outside of the immediate COVID-19 onset

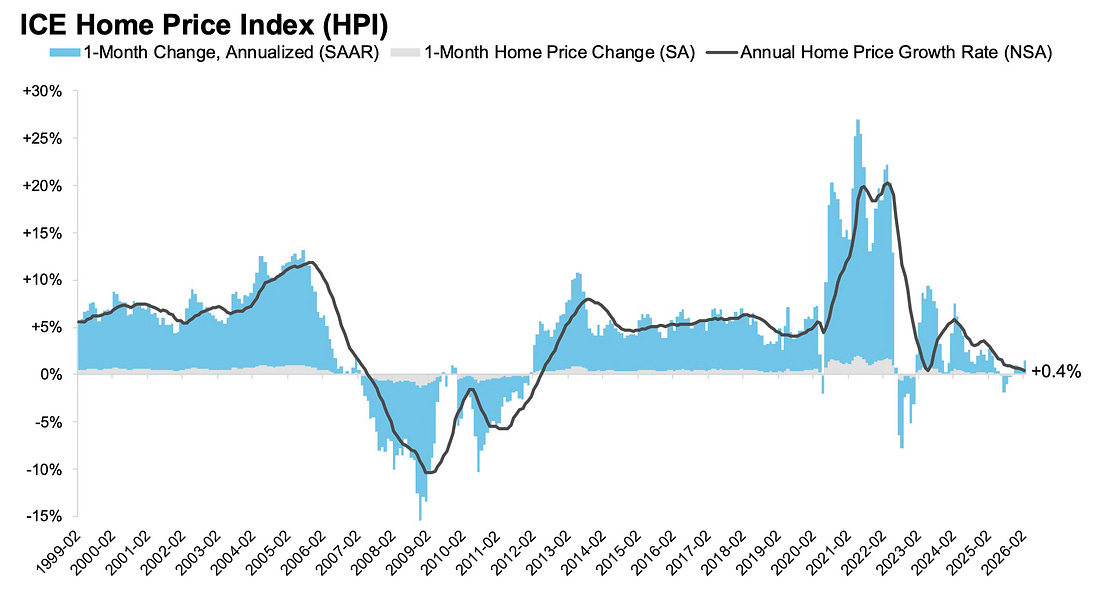

House Prices Up 0.4% Year-over-year in February

Here is the year-over-year in house prices according to the ICE Home Price Index (HPI). The ICE HPI is a repeat sales index. ICE reports the median price change of the repeat sales. The index was up 0.4% year-over-year in February.

- Annual home price growth continued to slow in February, with prices up 0.4% year over year — the second-slowest growth rate since 2012, behind only May 2023

- On a seasonally adjusted basis, prices rose 0.13% from January (equivalent to a 1.5% seasonally adjusted annualized rate), the strongest single-month gain in nearly a year

- That modest rebound may be an early sign of price reheating as rates fell and affordability improved to its best level in nearly four years — a trend worth monitoring as the spring buying season gets underway

- Single-family prices are up 0.67% year over year. Condo prices are down 2.2%, with nearly 60% of major markets seeing condo price declines and 97% seeing condos underperform single-family homes

Average annual property insurance payments rose to an all-time high

- Average annual property insurance payments rose 6.6% ($149) in 2025 to an all-time high, though this was the slowest rate of growth since 2020

- The fourth quarter saw a slight quarterly decline — the first since ICE began tracking the metric in late 2023

- Insurance cost growth (6.6%) modestly outpaced overall PITI growth (6.3%); the largest PITI increases were in mortgage interest (10.2%) and property taxes (7.4%), while principal payments edged down 0.5%

- The more moderate insurance increase reflected slower growth in both coverage amounts (4.6%, smallest since 2020) and the cost per $1,000 of coverage (up 2% to $6.21, vs. 14% over the prior two years)

Here is the ICE March Mortgage Monitor report (pdf).

Press Release: ICE Mortgage Monitor: Q4 Lending Climbs to 3.5-Year High as Refinance Activity Accelerates and Servicer Retention Strengthens