CALCULATEDRISK

By Bill McBride

I started the year taking Fed Chair Jerome Powell’s approach to the impact of policy: I’d wait to see what was implemented before changing my outlook.

Now we know a little more. Although there is still significant uncertainty, it appears that tariffs will stay (and likely increase in early April). Deportations will likely pickup. And net legal immigration will slow sharply.

On immigration and deportations, Goldman Sachs economists wrote in February:

We expect net immigration to slow further to 750k per year, well below the pace of the last three years but only moderately below the normal pre-pandemic pace. This would consist of 750k net authorized immigrants per year and zero net unauthorized immigrants, with roughly 500k deportations per year offsetting a similar number of asylum seekers and other entrants. …

In a more extreme risk scenario where the immigration crackdown creates a climate in which unauthorized immigrants are afraid to go to work or employers are afraid to employ them, the economic consequences would be more serious because unauthorized immigrants already in the US account for 4-5% of the total workforce and 15-20% in some industries. Abruptly losing these workers could be very disruptive for many of these industries and have a larger inflation impact.

We are also seeing a sharp decline in international tourism that will impact hotels and the travel industry. However, my focus is on housing.

A few impacts:

• Tariffs will lead to higher costs. I spoke to a contractor last week who hasn’t seen any price increases yet, but he said he had received “warning letters” from key suppliers about likely price increases. The uncertainty around tariffs also makes it more difficult to bid projects.

• Less immigration will lead to less household formation. This suggests less demand for housing, especially for rentals.

• An immigration crackdown would lead to fewer workers in construction. This would push up costs for construction. This would also lead to more rental vacancies.

This suggests higher costs for construction and less demand for housing.

On regulations, the NAHB reported this month:

Builders are starting to see relief on the regulatory front to bend the rising cost curve, as demonstrated by the Trump administration’s pause of the 2021 IECC building code requirement and move to implement the regulatory definition of ‘waters of the United States’ under the Clean Water Act consistent with the U.S. Supreme Court’s Sackett decision.

However, most regulations are at the state and local level, so any regulatory relief will likely be minor.

And another factor is the recent stock market volatility. Ten percent corrections are common, a further sell-off will have a negative wealth effect for potential home buyers. Some buyer hesitancy – due to the market volatility – might be the reason Lennar reported they “Didn’t see typical seasonal pickup after February” for new home sales.

Finally, it is difficult to ascertain the 2025 impact of DOGE, but it appears negative for employment this year.

What does this mean for housing starts, new home sales and house prices?

Here was my outlook at the start of 2025:

My guess is multi-family starts will decline further in 2025, likely down 5% or so year-over-year (less than the previous 2 years). Single family starts will likely be mostly unchanged year-over-year, putting total starts down slightly.

I expect New Home sales to be up around 5% YoY.

If existing home sales remain fairly sluggish, we might see national months-of-supply above 5 months in mid-2025.

That would likely lead to mostly flat prices nationally in 2025. However, I expect some areas – with higher months-of-supply – will see price decline in 2025.

I don’t expect either a crash in prices or a surge in prices.

“Time” will likely lead to more new listings in 2025. Mortgage rates will remain well above the pandemic lows, and new listings will likely be depressed again in 2025 compared to pre-pandemic levels.

The bottom line is inventory will probably increase year-over-year in 2024. However, it still seems unlikely that inventory will be back up to the 2019 levels.

Housing Starts and New Home Sales

It is difficult to quantify, but it appears policy will negatively impact housing starts this year.

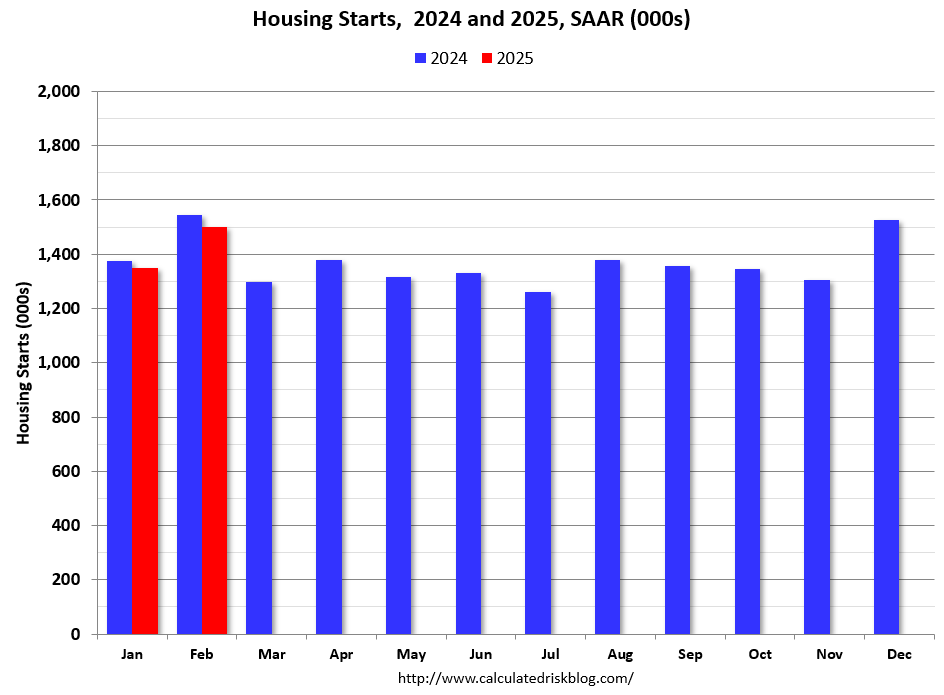

So far, through February, single family housing starts are down about 2% year-to-date (YTD) seasonally adjusted (SA) and multi-family starts are down about 4% YTD SA. This graph shows the month-to-month comparison for total starts between 2024 (blue) and 2025 (red).

With higher costs – and potentially less demand – I now expect single family starts to be down YoY, and multi-family starts down 10% or so.

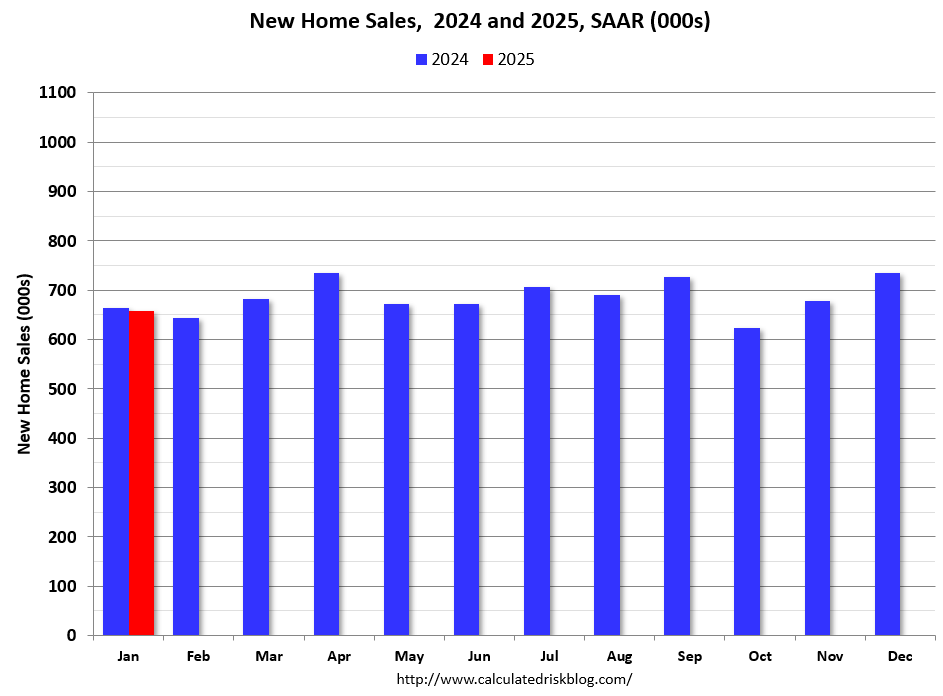

For new home sales, we only have data for January. Sales for February will be reported tomorrow and will likely not be impacted by policy changes. The February consensus is for new home sales of 680 thousand (SAAR). That would put YTD sales up about 2%. However, sales in March (see Lennar’s comments) might be impacted by policy and market volatility.

The next graph shows new home sales for 2024 and 2025 by month (Seasonally Adjusted Annual Rate). Sales in January 2025 were down 1.1% from January 2024.

My initial guess was that new home sales would be up about 5% YoY. My sense now is sales will be flat or even down YoY.

Note: If there is a negative impact from policy, it will show up in new home sales first, since new home sales are reported when the contract is signed whereas existing home sales are reported when the contract closes (usually 45 to 60 days after signing).

Housing Inventory and House Prices

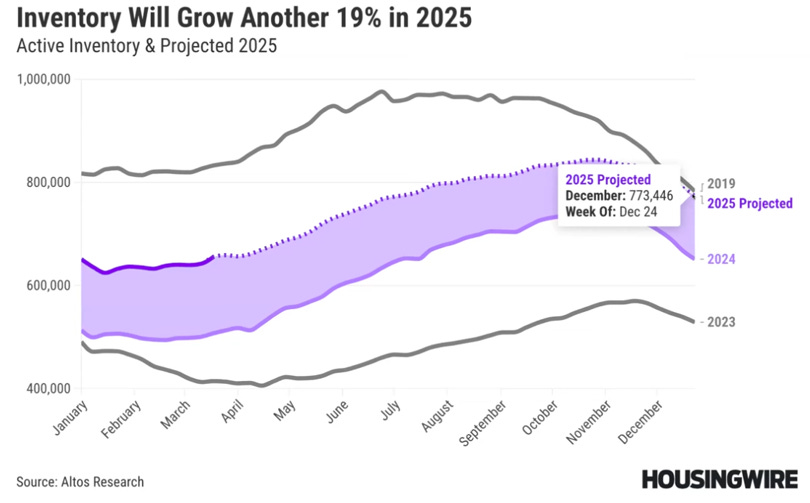

Altos Research put out an updated inventory projection last week showing that inventory might end the year at 2019 levels!

If inventory is close to 2019 levels by the end of 2025, and sales remain sluggish, months-of-supply will move up sharply. Sales could pick up if mortgage rates decline, however, if the decline is related to a weaker economy, the increase in unemployment might outweigh any boost from lower mortgage rates.

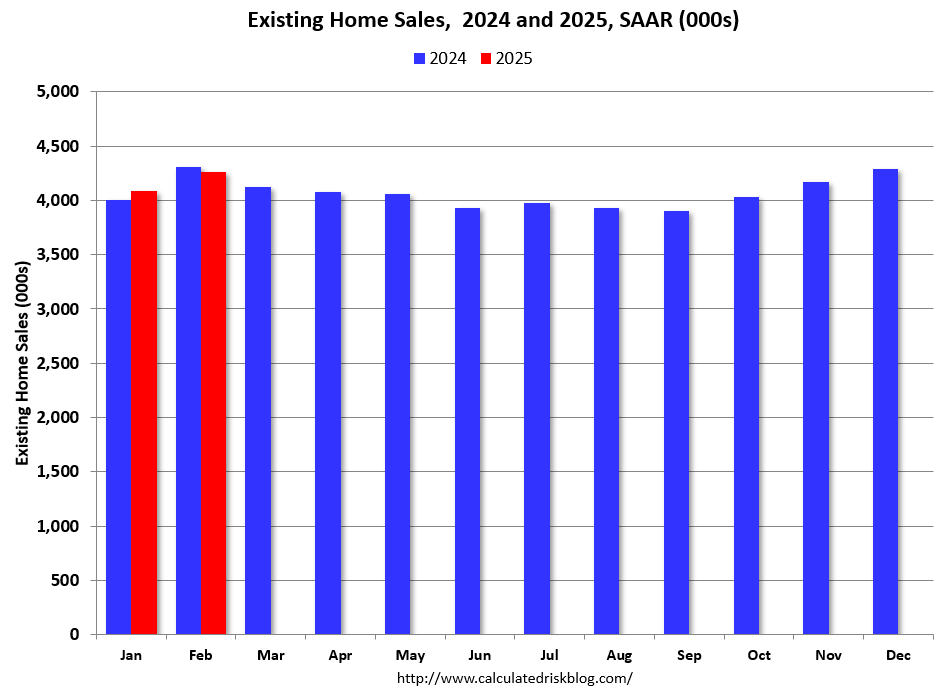

Note: The pickup in existing home sales in February surprised many analysts (but not readers of this newsletter!). The sales increase in February doesn’t mean sales are recovering, just that analysts underestimated the seasonal adjustment for February, especially this year since there was one fewer working day in February 2025 compared to February 2024. In fact, sales were down YoY.

Rising months-of-supply will put pressure on prices, but my guess is that that would be more of a 2026 story since house prices then to be sticky downwards (it takes time for sellers to realize they need to lower their price). So, I’ll stick with my “mostly flat prices nationally in 2025”.

In general, it appears that policy will be negative for housing this year. Also, the risks appear skewed to the downside. I’ll update the outlook if policy changes again.