Inman News

Rates on jumbo loans are currently lower than conventional mortgages, but could surge higher in the months ahead.

Demand for purchase loans rose last month to levels approaching records set in March, but rising home prices mean homebuyers are increasingly likely to need to apply for jumbo loans that have traditionally carried higher interest rates.

The latest Originations Market Monitor report from mortgage and property data aggregator Black Knight shows purchase loan rate locks surged by 6 percent last month, reversing two consecutive months of declines. Cash-out refinancings were also up 10 percent, while rate-and-term refis fell 4 percent.

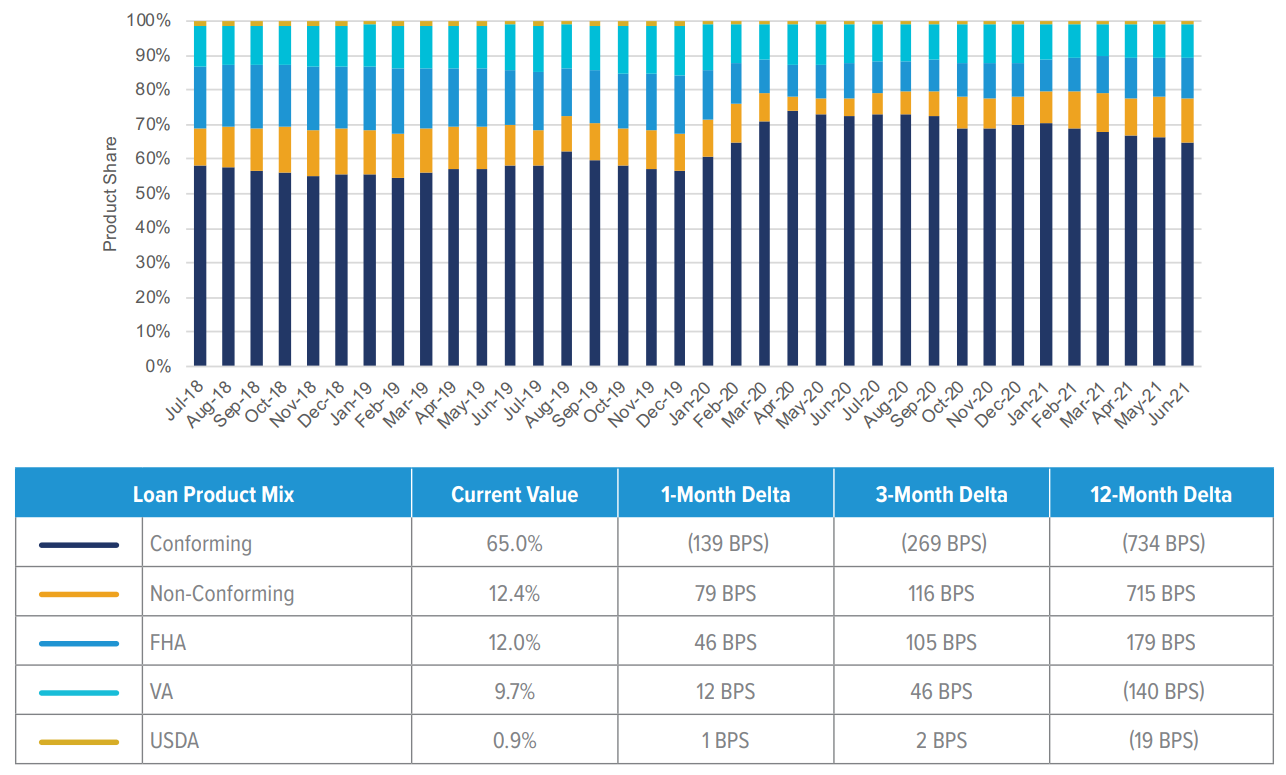

Non-conforming, “jumbo” mortgages accounted for 12.4 percent of all purchase and refinance rate locks, up from 5.25 percent a year ago. Conforming mortgages eligible for purchase or guarantee by mortgage giants Fannie Mae and Freddie Mac accounted for 65 percent of all mortgage rate locks in June, down from 72.3 percent a year ago. FHA loans captured a 12 percent market share, up from 10.2 percent a year ago.

Rate lock volumes by loan product.Source: Black Knight Originations Market Monitor.

Record-breaking home price appreciation is changing borrower behavior and the makeup of the mortgage market, said Black Knight Secondary Marketing Technologies President Scott Happ, in a statement.

Rising home prices track with “the continued, growing jumbo share of lending in the market and the decline in the conforming share a result,” Happ said. “With rates holding steady and purchase lending strong, additional growth in home prices may extend this trend further.”

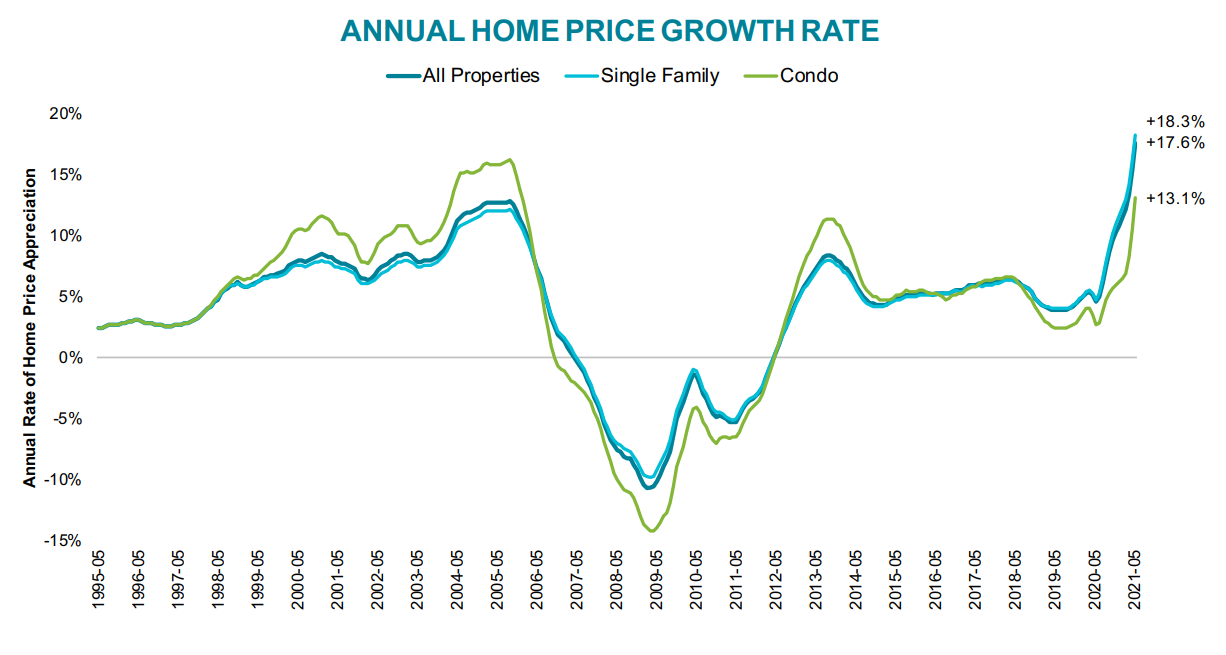

The latest Black Knight Home Price Index showed single-family home prices up a record 18.3 percent year-over-year in May, with condo prices up 13.1 percent during that time. That means even though interest rates remain low, homebuyers would need to devote 21.3 percent of the median household income to make their monthly mortgage payments, on average, up from 18.1 percent at the beginning of the year.

Source: Black Knight Mortgage Monitor

In markets like Los Angeles, monthly mortgage payments can take up as much as 46.5% of the median household income, “an unsettling number for buyers hoping to make the leap into homeownership,” Black Knight analysts said.

According to the National Association of Realtors, existing-home prices hit a record high of $350,300 in May, a 23.6 percent annual increase. The conforming loan limit is adjusted on an annual basis, based on a home price index maintained by Fannie and Freddie’s regulator, the Federal Housing Finance Agency.

In most of the U.S., the conforming loan limit for 2021 is $548,250. Bigger “jumbo” loans aren’t eligible for purchase or guarantee by Fannie and Freddie, although the mortgage giants can acquire loans of up to $822,375 in high-cost housing markets.

The Federal Housing Administration will insure mortgages that don’t exceed 65 percent of the conforming loan limit, or $356,362, in most markets. In high-cost areas, FHA will match Fannie and Freddie’s upper limit of $822,375. But FHA-insured loans typically carry higher interest rates and up-front and annual insurance premiums.

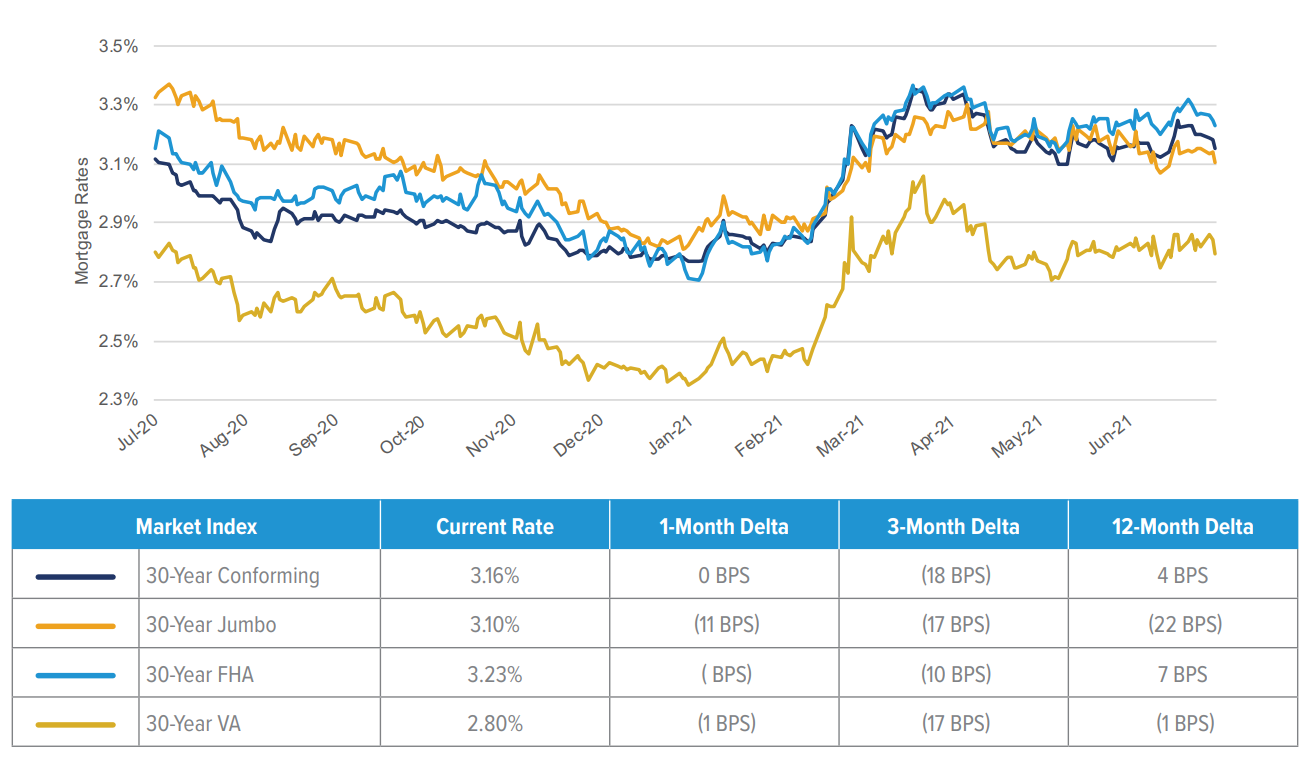

Jumbo mortgage rates drop below conforming, FHA loans.Source: Black Knight Originations Market Monitor

In the early days of the pandemic, lenders like Wells Fargo cut back on jumbo mortgage lending or charged higher rates, to offset the greater risk of making loans that aren’t backstopped against losses by Fannie, Freddie or FHA.

A year ago, jumbo loans carried higher interest rates (3.32 percent) than conforming loans (3.12 percent) or FHA loans (3.16 percent). But at 3.10 percent, rates on 30-year jumbo mortgages are currently more affordable than conforming loans (3.16 percent) or FHA loans (3.23 percent), according to Black Knight.

“A rapidly improving economy and job market has freed up jumbo credit, as banks have deposits to utilize,” Mortgage Bankers Association forecaster Joel Kan noted in June.

But rates on jumbo loans could quickly surge higher in the months ahead if lenders and secondary investors who buy mortgage backed securities not guaranteed by Fannie, Freddie or Ginnie Mae lose confidence in the economic recovery, or if default rates rise.