HousingWire

Prices for both new and existing homes are through the roof.

By Logan Mohtashami

The world has been dealing with a significant health crisis since the beginning of 2020. This has provided the American bear troll crowd numerous opportunities to pontificate about a likely long-lasting depression. If you bought into the theories being peddled by this crash-cult crowd (who, by the way, have been infecting the discourse of economics since the creation of social media and YouTube channels) then you would have believed that the second housing market bubble crash was imminent during 2020.

But the U.S. economy recovered quicker than anyone ever imagined — well, almost everyone (wink, wink). Life is much better today than it could have been, but we are now suffering from what can only be called a first-world problem in the U.S. housing market.

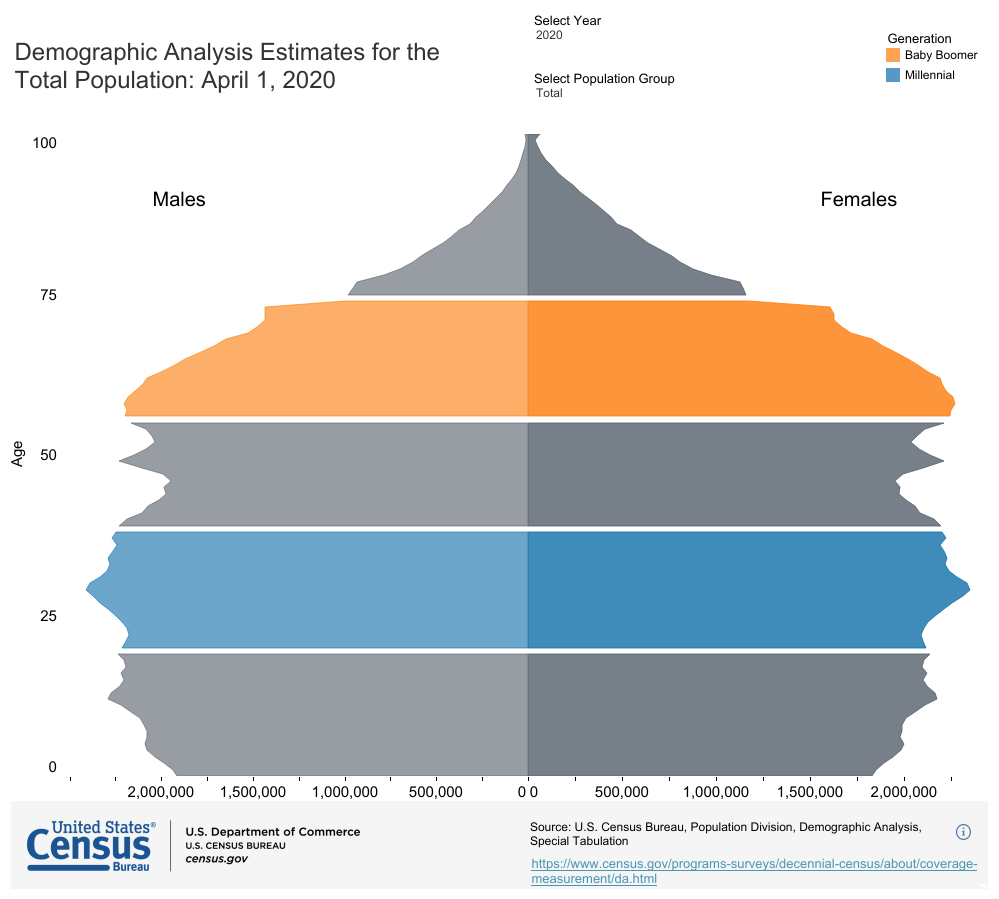

Here is the problem: In the years 2020 to 2024, Mother Demographics is providing the U.S. with the most significant number of adults of first-time home-buying age ever in history — and this is during a time when we are enjoying the lowest mortgage rates. With this one-two punch, is it any wonder that the U.S. housing market has outperformed all other economic sectors during COVID-19?

If every cloud has a silver lining, then every advantage has its disadvantage. The advantage of having great housing demographics and low mortgage rates at the same time is that we will have stable demand for homes during this period. Think of it this way: Every time a person buys a home, a potential homebuyer is removed from the market for the time that person (or family) remains in the home. Since housing tenure (the length of time a person stays in a home) has been increasing, that potential homebuyer is being removed from the market for a longer time.

Because we have the largest number of 27 to 33 year-olds in history now, we can count on a stable supply of replacement buyers in 2020-2024. Add to young homebuyers, move up, move down, cash buyers, and investors, and we have stable demand during this period.

The disadvantage to this seemingly ideal scenario for the housing market is that home prices could escalate to an unhealthy level during this period.

Providing housing to meet demand during and following the COVID-19 crisis has created its own set of problems. Shortages of goods and services are evident in everyday life here in America. Shortages of everything from computer chips to lumber along with shortages of labor to make and deliver goods means we are paying more for certain items and services. The world marketplaces are negotiating going from zero to full speed to meet demand.

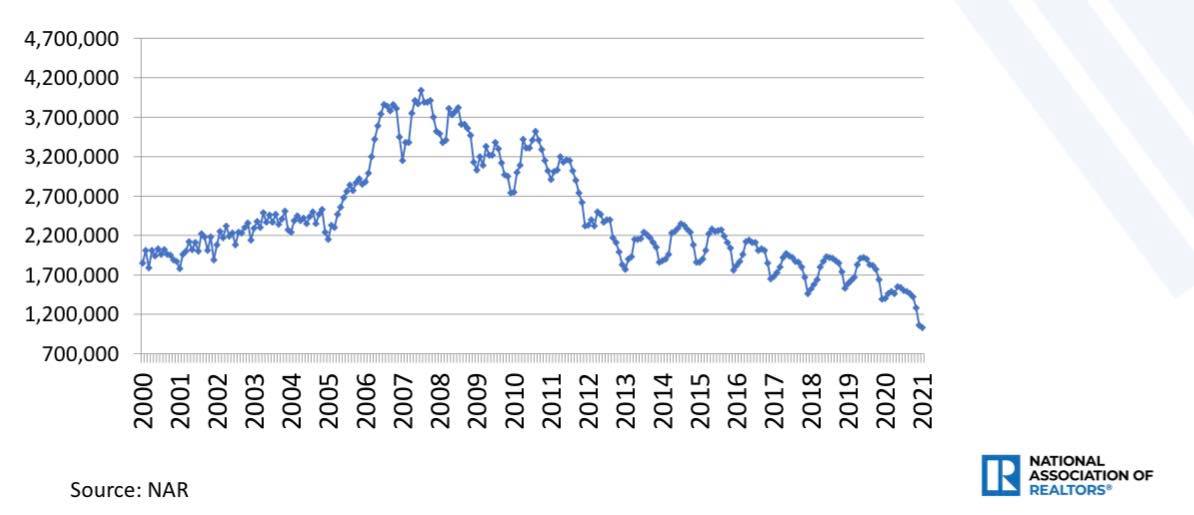

The U.S. housing market has had its own unique set of issues transitioning from pre-COVID to the post-COVID world. Since 2014, total housing inventory has been falling while purchase application data have been rising since the recent bottom in 2014.

From the National Association of Realtors:

COVID-19 made this situation worse because it disrupted the natural equilibrium between supply and demand. Millions of homes went into forbearance. If COVID-19 didn’t create the need for the successful forbearance program, some of those homes would have been available. Then, because the world economies were negatively affected by the COVID-19 crisis, mortgage rates fell and have stayed lower for longer than usual.

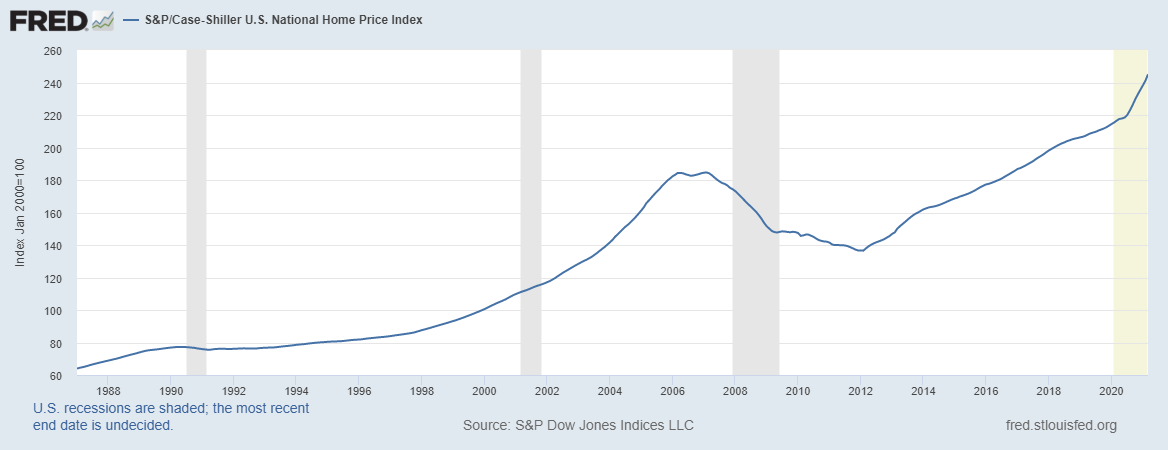

The COVID-19 crisis has kept mortgage rates lower and suppressed inventory, and these two factors have facilitated higher levels of price growth because COVID_19 happened right during the sweet spot for the U.S. housing market in the years 2020-2024.

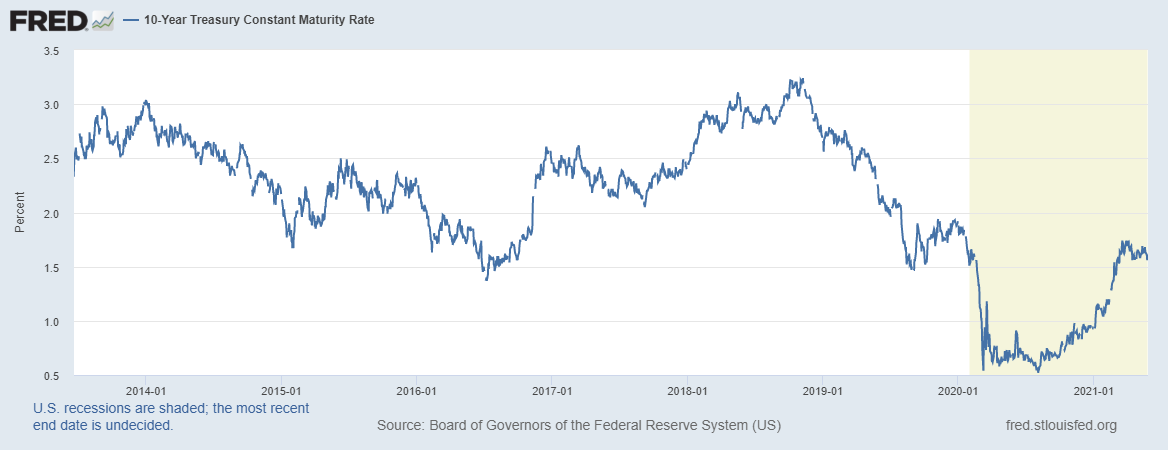

When mortgage rates were over 4% in the previous expansion, it never killed demand but kept price growth at bay. When the 10-year yield went over 2.62% is when we saw housing demand lose some steam. Don’t forget that in 2019 real home prices were negative year over year as the 10-year yield got to 3.24% in 2018. Even though nominal home prices still grew in 2018-2019 with 4.5% -5% mortgage rates, the rate of growth cooled down, and supply was there for Americans to buy without bidding wars.

2018 and 2019 were healthy in the sense that supply was there for Americans to buy and total existing home sales were still over 5 million.

If we look back to February of 2020, the housing data for that month show that the market was heating up after years of slow and steady growth. This was the prelude for what to expect in the housing market for the period of 2020 to 2024 when we hit our demographic sweet spot. COVID-19 put a temporary halt to housing-market growth while we redirected our energy toward hoarding toilet paper and learning to bake bread.

The demand for housing never went away, but the ability to act on that need was curtailed, and some supply was taken off the grid with forbearance and the moratorium on evictions for rental units. Today, I think we have finally hit the nadir in inventory, and we should see increases in inventory and days on the market going forward. For more on this, refer to the article I published back in April about how eventual increases in inventory should cool down-home price growth.

Home-price growth has been driven by an inventory shortage, not a boom in housing demand. If home price gains were due to demand, we would see a concurrent credit boom from all those new mortgages, but we do not see that. As I have stated many times before, during the period of 2020 to 2024 the housing market will have great replacement demand, which is fundamentally different from what we had from 2002 to 2005, which was due to expanding the purchase capacity beyond its normal scope of buyers to include those less financially stable and a lot of speculation buyers.

Today, for the most part, our buyers are the standard vanilla homebuyer — we just have slightly more of them because of demographics. This means we have a lot more folks coming into the first-time homebuyer age. Add to this the usual supply of move up, move down, cash buyers and investors, and we have stable demand during this period.

Unlike the period of 2002 to 2005 when speculation buying was rampant, those looking to purchase today just want somewhere to live. It is sad (and yes, I know this is a first-world problem) that they are being forced to compete against 10, 20, and even 30 other bidders for a home. And this is happening in a year when existing home sales will be only slightly higher than last year.

We have an increase in the number of buyers and a total collapse of inventory driving home-price growth. In the last expansion, the only thing that kept home-price growth from taking off was the higher mortgage rates of 4% to 5%. We are currently enjoying the lowest mortgage rates ever, so we don’t have that to dampen the market.

Yes, these are unhealthy realities of housing for 2020-2021. And there is not much that can be done to relieve these pressures. The housing bubble and bust was a real economic crisis and housing crisis. What is going on now is frustrating for would-be buyers but it is not an economic crisis. Homebuyers today are employed with well-paying jobs and adequate liquid assets to support a mortgage payment — even to the point of paying much higher than the asking price. This period in U.S. history of housing is unique, but these problems are those of the haves, not the have-nots — that is a whole other story.

Price gains in the existing home sales market are not the only drama going on in the housing market. New home prices have also escalated. Not just lumber, but the costs of appliances and other supplies necessary for new home construction have gone up, post-COVID-19. Builders have the pricing power to push these costs through to the buyer because their buyers tend to be older and wealthier, with higher incomes.

To exacerbate this issue, similar to what is happening in the existing home market, new homebuyers are moving from high-cost states to lower-cost states and out-competing local buyers. Here is an example with which I am personally acquainted. In my Irvine, California, neighborhood, a one-bedroom condo built-in 2004 that is roughly 800 square feet is priced at a tad over $500,000. That would buy you a nice new three-bedroom home in many areas of the country.

The new home sales marketplace is unhealthy, but when mortgage rates rise, this sector will get hit harder than the existing home market, like it always does. This won’t result in an epic housing crash, but it will impact future construction.

When builders sense a decrease in demand, they stop aggressively building to squeeze inventory in order to keep prices stable. This is their business model. Life is going to be much different for the builders in a 4% plus mortgage interest rate world compared to the 3% world. For more on this check out my housing supply article published last year where I warned that the new home sales sector didn’t look healthy.

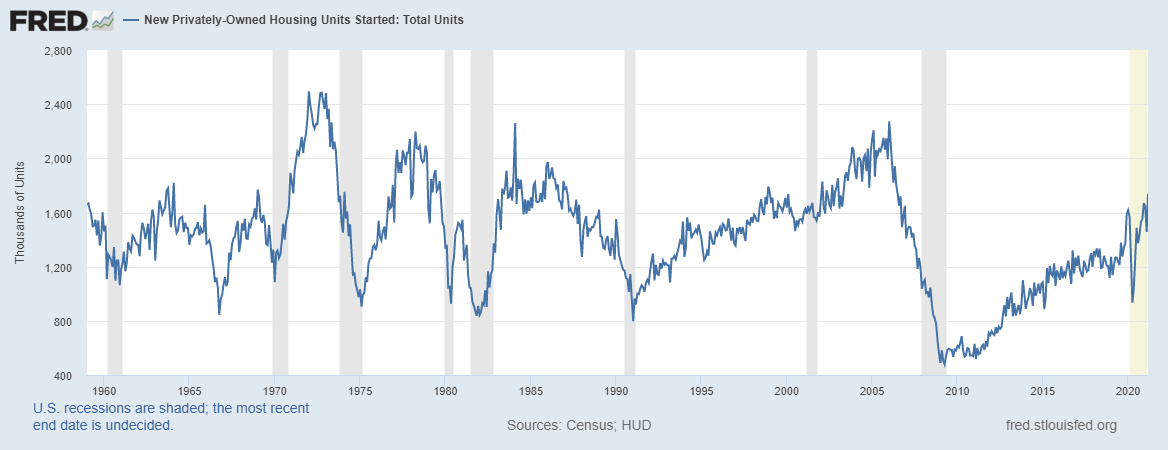

Don’t forget that the low bar that housing was working from in the previous expansion from 2008-2019 is gone. So we have all these price pressures in the new home sales market with housing starts getting near to starting a full year at 1.5 million, a call that I truly believed could only happen in the years 2020-2024. Something that I didn’t believe could happen from the years 2008-2019: we ended 2020 with 1,380,000 total housing starts. Trust me, if demand gets hit when rates go higher, the builders will slow things down.

So yes, for both new and existing homes I am saying this is an unhealthy housing market. In time, inventory will rise because we are not experiencing a massive credit boom and we have demographic limits on how many homes will be purchased in a year. For the years 2020 to 2024, if existing and new home sales combined are over 6.2 million, I will consider that the market has beat expectations. To cool price gains in the existing home market, I am rooting for an increase in the days on the market and total inventory to increase. I do believe this will happen. Price cooling is a good thing, not a bad thing.

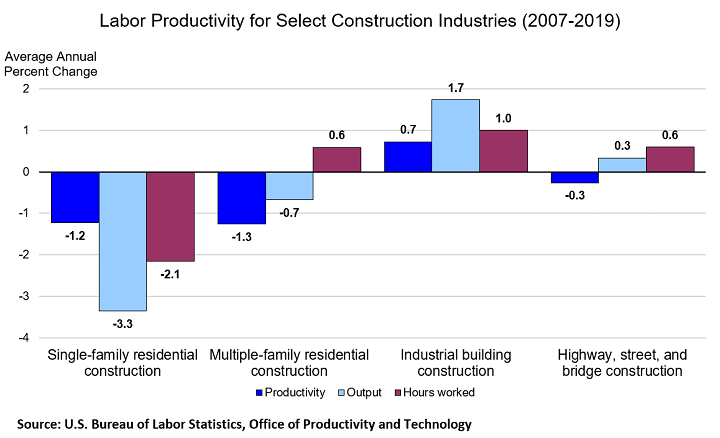

The new home sales market, on the other hand, has to contend with the increasing total cost to bring homes onto the market, Lumber has been the big story, but it is not just lumber driving the cost to build a house. Even if lumber prices collapse and the shortage of housing goods is solved, the expense of building homes in some regions of the U.S is making profitability not an easy task. Construction productivity has been awful in America for decades.

From BLS:

Remember, the new homebuilders with all their costs still must compete with the existing home market. There is a limit to how much they can increase prices. These are problems that are not going to go away unless we can find a much less expensive way to build homes. Even with all of that, new home sales and housing starts have been higher in 2020-2021 than any period from 2008 to 2019.

One question I get a lot is whether this is a good time to buy. Should you wait until the market cools down or pull the trigger before housing prices increase even more? This is both the easiest and hardest question to answer. Let me be blunt. If you need to be told when to buy a home, then you’re not ready because it is not about the marketplace — it is about you and your capacity to own the debt. The end. Millions and millions of Americans buy a home each year and in 2020 and 2021 more Americans bought homes than any year from 2008-2019. This with a global pandemic and the possibility of the economy in a brief recession.

It breaks my heart to see this unhealthy market in 2021, but I console myself with this: Americans are badass. After a few weeks of hunkering down during an epic health crisis, they started purchasing homes again because they needed a place to raise their families and because they could. And they’ve kept on buying houses in 2021 because they need shelter. These homebuyers are not listening to the crash cult fanatics, the YouTube doom-and-gloomers, or the bubble boys who spend all day crying about the collapse of the housing market, the dollar and massive inflation. You’re not one of those, are you? I know you’re not. A lot of that stuff is more for the show. I mean come on — housing was supposed to be in bubble 2.0 from 2012 and the playbook was not seeing housing outperform during this crisis.

So, to revisit the question: Should you wait it out?

First, we need to figure out what you are waiting for. If you can’t compete in this marketplace, I feel your pain. Nobody wants to overpay for anything, let alone the biggest single item you will buy in your life. Listen, housing is the cost of shelter to your capacity to own the debt. It is not a short-term or long-term investment. You are buying a payment to sleep with every night and wake up every morning. Millions and millions of Americans buy homes every year to live in, end of the story.

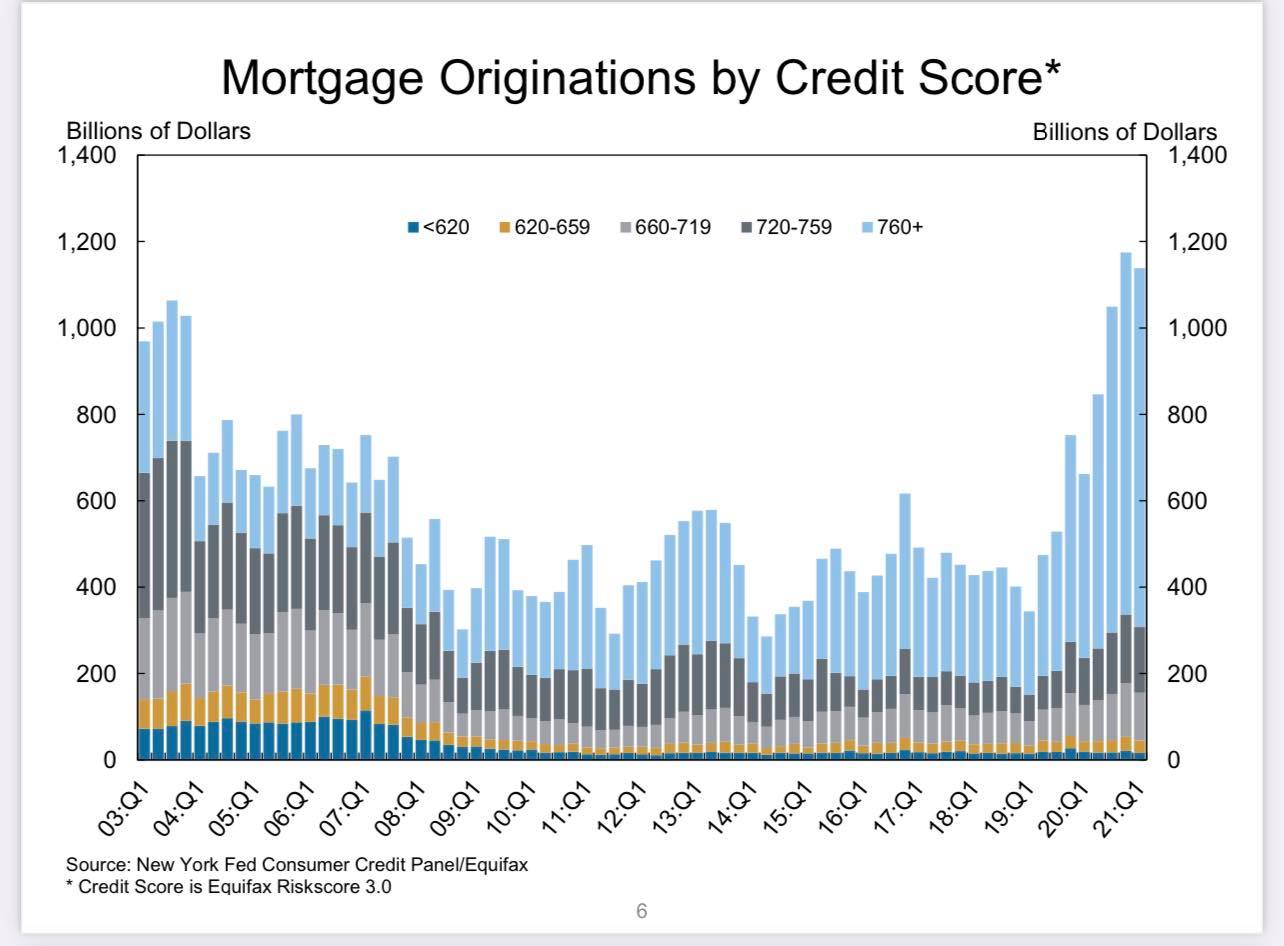

We have a few more homebuyers in 2020-2021 than we had from 2008-2019. It’s not a boom in demand — heck, 2020 existing home sales only ended 2020 with roughly 130,000 more homes sold than 2017 levels. We have no exotic loan debt structures. Which means that when a person buys a home, they have the financial capacity to own the debt. Lending standards are still very liberal, and tight lending in America is one of the most prolific urban myths of the 21st century.

Having said that, most Americans buy when they’re ready to own that debt. If 2020-2021 hasn’t convinced you of that, then you need to look in the mirror and ask why Americans are buying homes. A home is a place to raise your family in a neighborhood where you send your kids to school and just live life. The obsession over home prices, and how good of an investment it might be is kind of missing the point.

Keep it simple. It’s shelter. That is why Americans buy homes every year. Yes, we have investors, cash buyers, and those looking for rental yield – and I don’t want to dismiss that, but for most Americans, home is just home. Don’t ask yourself if you should wait, ask yourself are you ready to have a home and that payment. In the past decade, the advantage of homeowners is that they have fixed low debt cost versus rising wages, hence the great FICO scores.

Trust yourself to know if you’re ready to own a home or buy another one. If you feel like you’re being stretched financially to own a home, then go with that feeling. That payment that you’re buying should make you sleep easy at night and you shouldn’t need to overthink it. If your current housing situation, whether owning or renting — is more comfortable than trying to buy in this market, don’t dismiss that thought. You know better about your own finances than anyone else on planet earth. I trust that you know what you’re doing, I just wish we had more supply so this hunger housing games wouldn’t be so vicious.

Don’t forget; we are early in this economic expansion. A lot of the economic data, especially in housing, has been wild to the upside, and the moderation in the housing data that I have been talking about since last year is still in its process. This moderation in the data, I am sure, will be misinterpreted by the doom and gloom crowd. We have been through a lot as a country, but know that America is back from the COVID-19 crisis and soon we will all walk the earth freely. Economic cycles come and go and I need to be more focused than ever with housing data because this first-world problem is still an unhealthy housing marketplace.

Logan Mohtashami is a Housing Data Analyst for HousingWire and a financial writer covering the U.S. economy with a specialization in the housing market. Additionally, he served as a senior loan manager at AMC Lending Group, which has been providing mortgages for California residents since 1987. Mohtashami’s work is frequently quoted in BankRate.com and Bloomberg. He has been an invited speaker at the Americatlyst, California Association Of Realtors and the National Association Of Women In Real Estate Business and other economic conferences.