CALCULATEDRISK

Housing Starts Decreased to 1.321 million Annual Rate in March

By Bill McBride

Housing Starts Decreased to 1.321 million Annual Rate in March

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately‐owned housing starts in March were at a seasonally adjusted annual rate of 1,321,000. This is 14.7 percent below the revised February estimate of 1,549,000 and is 4.3 percent below the March 2023 rate of 1,380,000. Single‐family housing starts in March were at a rate of 1,022,000; this is 12.4 percent below the revised February figure of 1,167,000. The March rate for units in buildings with five units or more was 290,000.

Building Permits:

Privately‐owned housing units authorized by building permits in March were at a seasonally adjusted annual rate of 1,458,000. This is 4.3 percent below the revised February rate of 1,523,000, but is 1.5 percent above the March 2023 rate of 1,437,000. Single‐family authorizations in March were at a rate of 973,000; this is 5.7 percent below the revised February figure of 1,032,000. Authorizations of units in buildings with five units or more were at a rate of 433,000 in March.

emphasis added

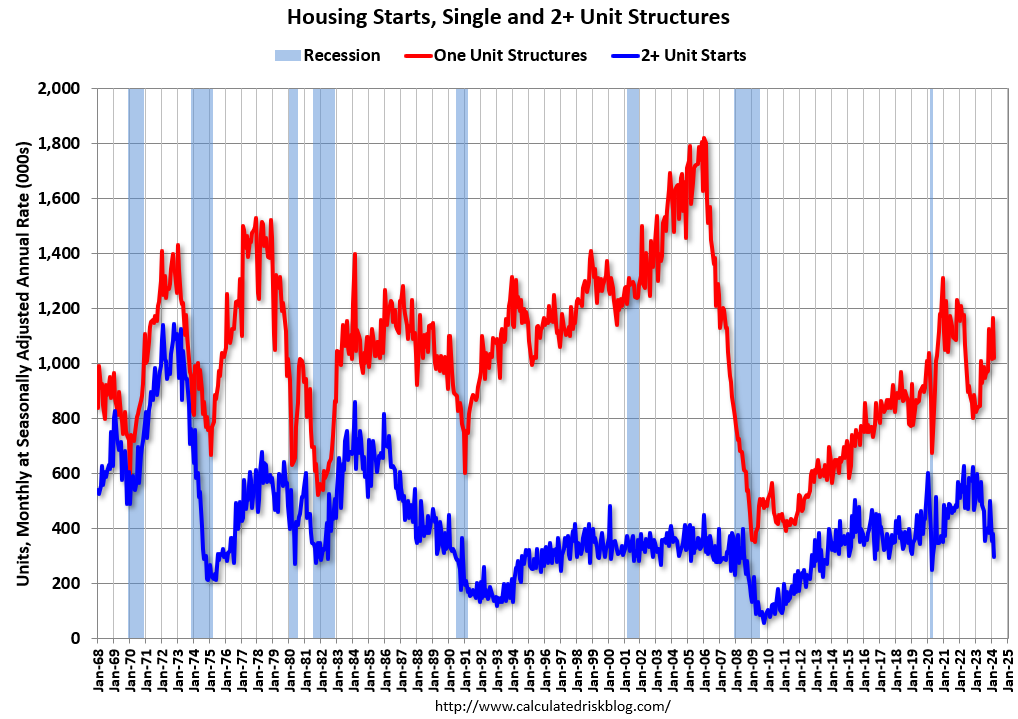

The first graph shows single and multi-family housing starts since 2000 (including housing bubble).

Multi-family starts (blue, 2+ units) decreased in March compared to February. Multi-family starts were down 44.3% year-over-year in March. Single-family starts (red) decreased in March and were up 21.2% year-over-year.

Note that the weakness in 2022 and early 2023 had been in single family starts (red), however the weakness has moved to multi-family now while single family has bounced back from the bottom.

The second graph shows single and multi-family starts since 1968. This shows the huge collapse following the housing bubble, and then the eventual recovery – and the recent collapse and now recovery in single-family starts.

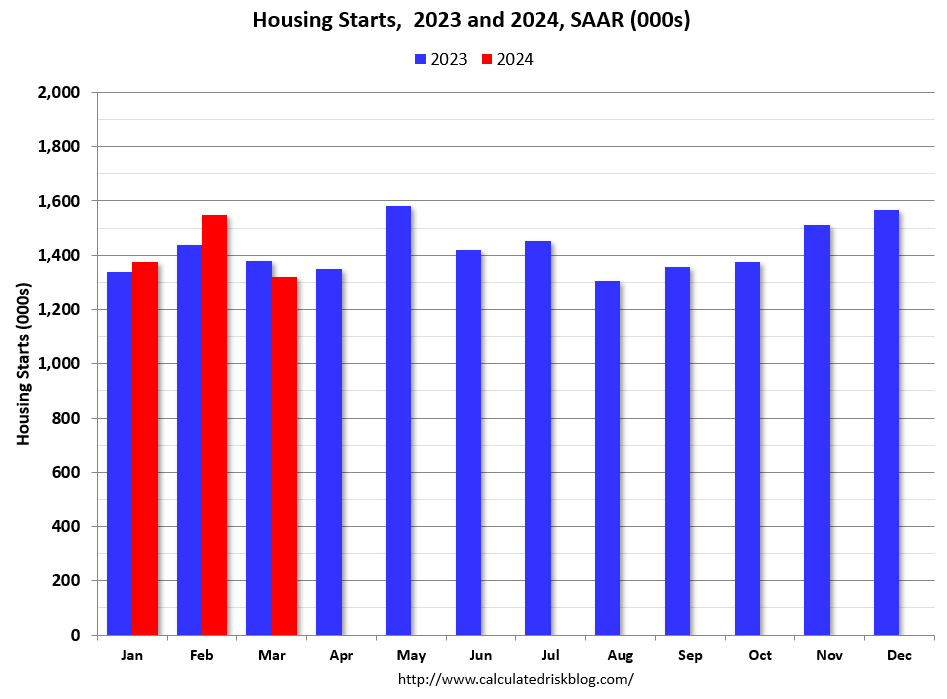

Total housing starts in March were well below expectations, however,starts in January and February were revised up.

The third graph shows the month-to-month comparison for total starts between 2023 (blue) and 2024 (red).

Total starts were down 4.3% in March compared to March 2023.

Starts were down year-over-year (YoY) in March following 4 consecutive months with starts up YoY. The YoY decline is due to the sharp decrease in multi-family starts.

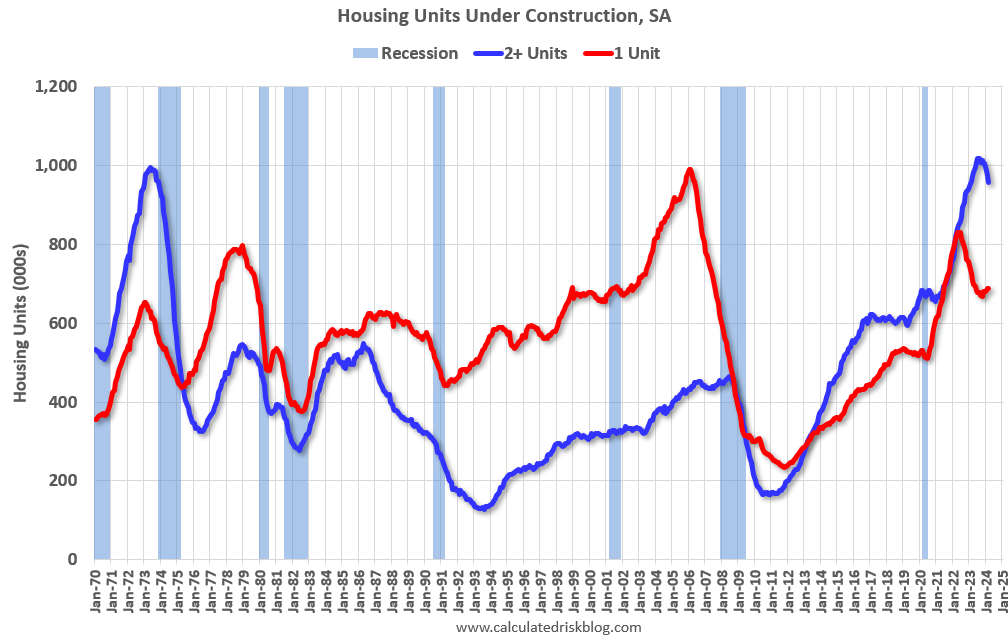

Multi-Family Housing Units Under Construction has Peaked

The fourth graph shows housing starts under construction, Seasonally Adjusted (SA).

Red is single family units. Currently there are 689 thousand single family units (red) under construction (SA). This was up in March compared to February, and 142 thousand below the pandemic peak in May 2022. Single family units under construction peaked in 2022 since supply chain constraints have eased.

Blue is for 2+ units. Currently there are 957 thousand multi-family units under construction. This is 61 thousand below the record set in July 2023 of 1,018 thousand. For multi-family, construction delays have been a significant factor, but multi-family units under construction have peaked and will likely decline significantly in 2024.

Combined, there are 1.646 million units under construction, 64 thousand below the all-time record of 1.710 million set in October 2022.

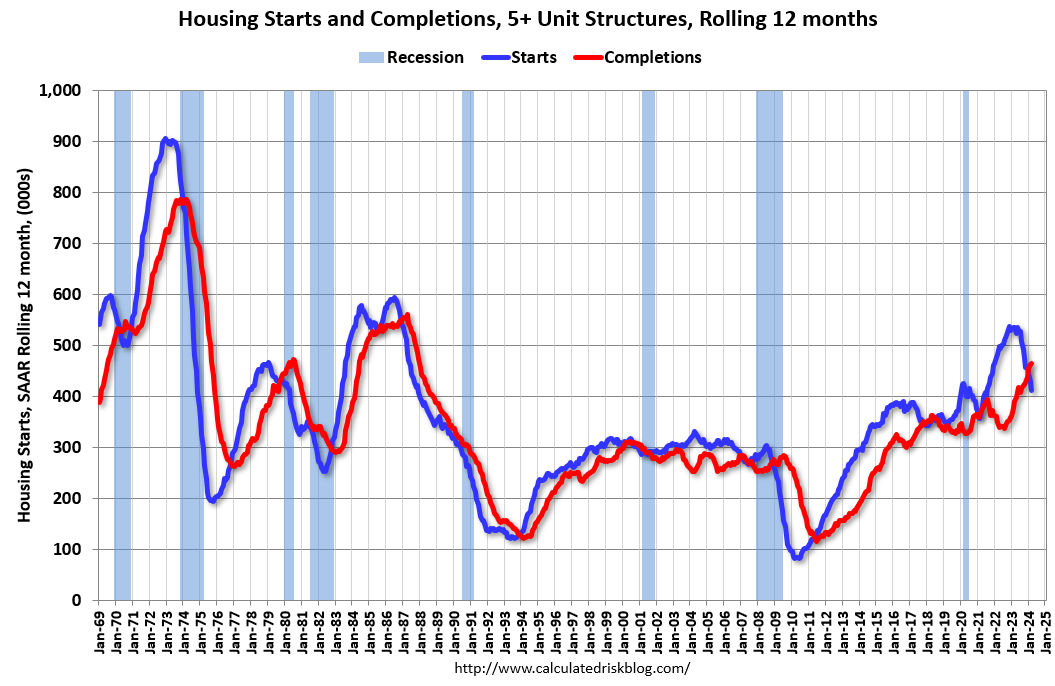

Comparing Starts and Completions

Below is a graph comparing multi-family starts and completions. Since it usually takes over a year on average to complete a multi-family project, there is a lag between multi-family starts and completions. Completions are important because that is new supply added to the market and starts are important because that is future new supply (units under construction is also important for employment).

These graphs use a 12-month rolling total for NSA starts and completions.

The blue line is for multifamily starts and the red line is for multifamily completions. Builders are now completing more multifamily housing units than they are starting on a 12-month basis. Multifamily starts will likely decline further on a rolling 12-month basis, and completions will increase over the next year.

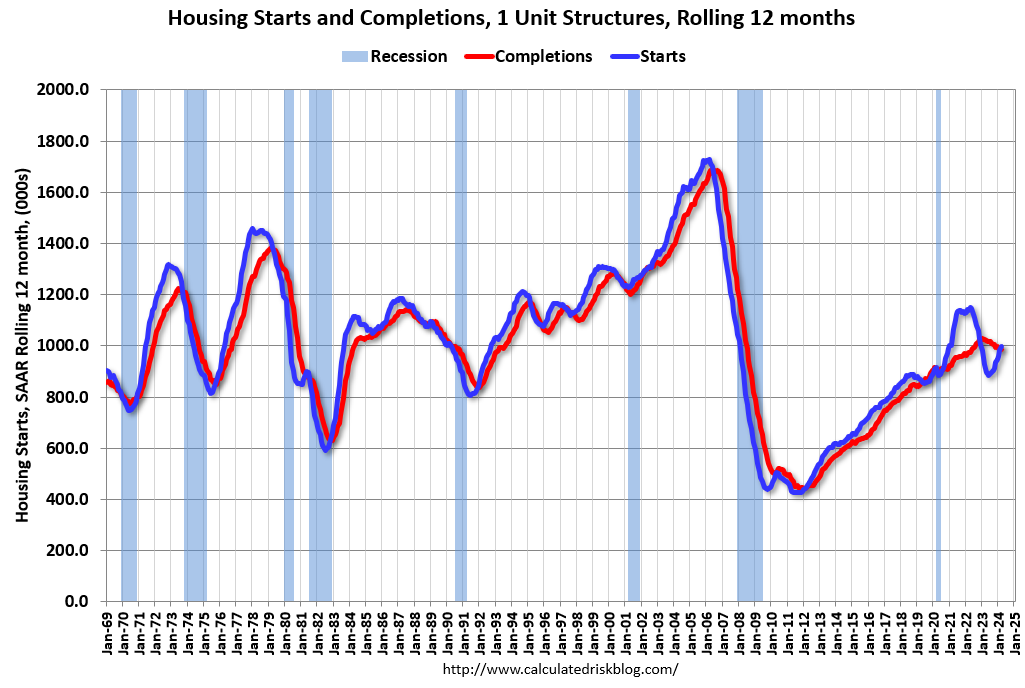

The last graph shows single family starts and completions. It usually only takes about 6 months between starting a single-family home and completion – so the lines are much closer than for multi-family. The blue line is for single family starts and the red line is for single family completions.

Builders are now starting slightly more single-family homes than they are completing on a 12-month basis.

Conclusions

Total housing starts in March were well below expectations, however, starts in January and February were revised up.

The weakness in 2022 and early 2023 was in single family starts. However, single family starts have now picked up year-over-year, helped by limited existing home inventory. The bottom for single family starts was in November 2022 and single-family starts were up 22% year-over-year in March.

The expected weakness in multi-family starts began last summer, and we should see ongoing weakness in the sector based on less household formation, flat asking rents, rising vacancies, and tighter lending. We saw this coming in the National Multifamily Housing Council’s (NMHC’s) Quarterly Survey of Apartment Market Conditions and in the Architectural Billings Index that showed a decline in multi-family design for the 19th consecutive month in February.